Zerbor

Article Thesis

Capital Southwest (NASDAQ:CSWC) is a fundamentally strong business development company that has seen its shares come under significant pressure in 2022. At current prices, the company offers a compelling dividend yield of 12% that is reasonably covered. For income investors seeking a high-yield vehicle, Capital Southwest looks like a good investment at the currently very undemanding valuation.

Capital Southwest’s Recent Performance

The company reported its most recent quarterly results, for its fiscal second quarter of 2023, in October. The company grossed revenue, or total investment income, of $27 million during the quarter. That was up by more than 30% year over year, although investors should note that company-wide growth does not fully flow through to investors — since Capital Southwest issues new shares regularly, some of the underlying business growth is eaten up by dilution. That’s not necessarily a problem, however, as long as this share issuance is accretive to some degree. Since Capital Southwest also grew its net investment income on a per-share basis, although at a slower rate relative to the company-wide growth, the last year has been successful for the company.

Net investment income per share rose from $0.43 per share to $0.52 per share year over year, which pencils out to around 20% — which is still very compelling, although not quite as strong as the company-wide NII growth rate.

During the quarter, the company originated close to $90 million of new loans. The weighted yield on those debt investments is 10.6%, which is quite strong and which reflects that interest rates have been rising over the last year. CSWC benefits from that as it can also demand higher rates from the companies it makes loans to. Capital Southwest operates with a lower-risk approach, primarily making first-lien loans. More than 80% of its portfolio consists of such first-lien loans, and among the loans the company made during its fiscal second quarter, most were first-lien loans as well. One of its portfolio companies, DBA Giving Home Health Care, a healthcare services company, got a combination of a first-lien loan and a second-lien loan with warrants. Capital Southwest also funded $0.8 million of equity investments during the quarter, but that is almost negligible versus the loan investments it made during the period. Overall, that fits with management’s past strategy of primarily investing in low-risk debt investments, relative to riskier equity investments.

The company also exited three investments during the period, which brought its weighted average IRR since 2015 to 14.7%, which is quite attractive and which explains why Capital Southwest has been a solid total return investment in the past.

Low Risks And Solid Operational Progress

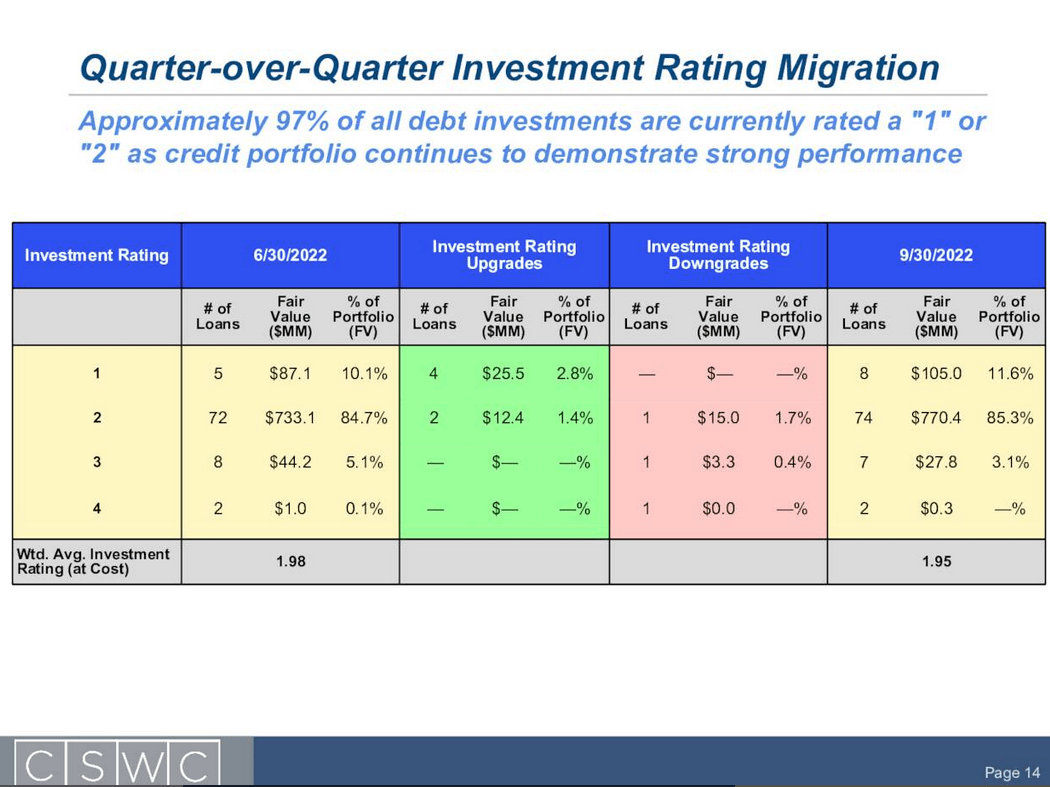

Looking at the risk ratings of the companies Capital Southwest is exposed to, we see the following changes over the most recent period:

CSWC presentation

While just 10% of the company’s investments had the highest credit rating at the end of the previous quarter, that ratio rose to 12% as of the end of the most recent quarter. At the same time, the exposure to companies with a “2” rating rose as well. Meanwhile, exposure to the lower rating categories “3” and “4” declined from 5% to just 3%. Overall, this indicates that credit quality improved and that Capital Southwest’s already low-risk portfolio became even less risky during the last couple of months. In a rising rates environment where many worry about a potential recession or economic downturn, that’s far from a given, and thus a noteworthy positive item that suggests that Capital Southwest’s underwriting is strong.

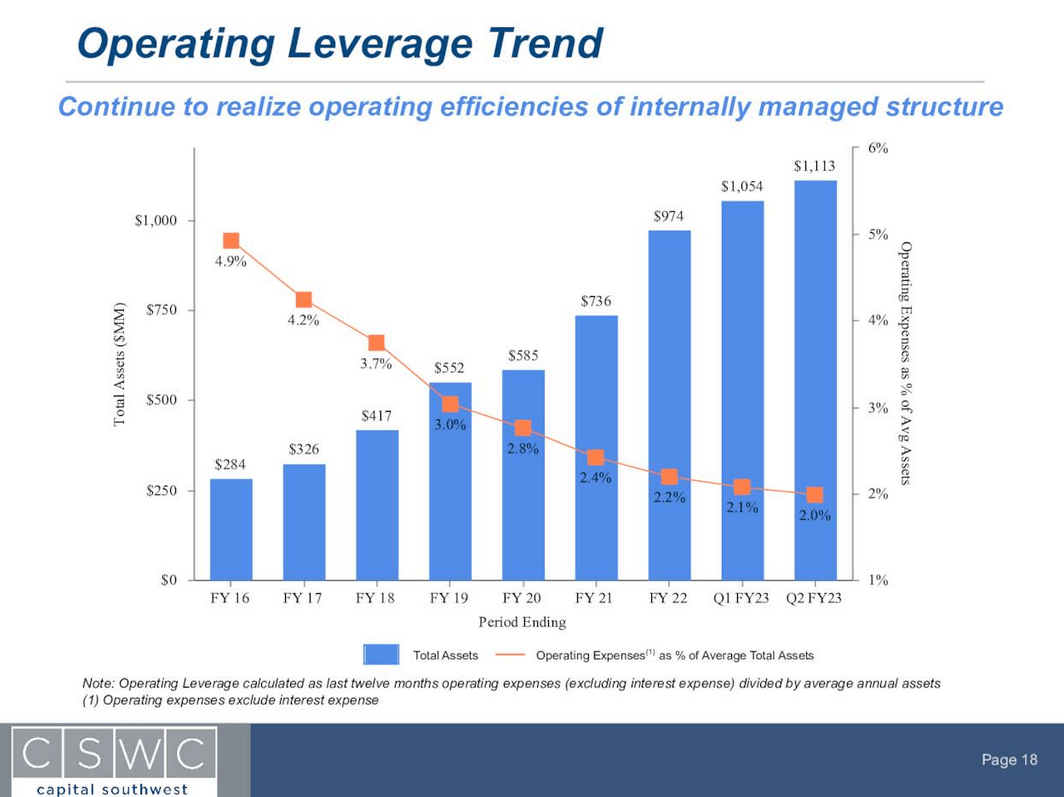

Capital Southwest is also making progress when it comes to improving its efficiency over time. Since operating expenses for business development companies can heavily impact profitability, progress on that front can be highly value-creating for shareholders.

CSWC presentation

Thanks to operating leverage — which means that operating expenses are distributed over a wider gross profit base as a company grows — the company has managed to more than half its operating expenses (on a relative basis) since fiscal 2016. As of the end of the most recent quarter, which saw an improvement on a sequential basis and on a year-over-year basis, Capital Southwest’s operating expenses are equal to just 2% of its average total assets. Since Capital Southwest generates an average yield of 10.6% across its portfolio, less than one-fifth of the company’s gross interest income is spent on operating expenses. Capital Southwest has proven to be ambitious when it comes to lower relative operating expenses over time, which is good news for investors — management is focused on doing what’s good for shareholders, whereas there is no hint of management trying to enrich itself at the cost of investors. With insiders owning more than 6% of the company, which is equal to around $30 million, it’s no wonder that executives are interested in creating value for shareholders, as that also benefits them directly.

Looking at CSWC’s balance sheet, we again see that there are not a lot of risks to worry about. The company has significant unused debt capacity, and there are no near-term maturities. The two credit facilities have $180 million of unused capacity as of the end of the second quarter, giving Capital Southwest considerable leeway should the company require additional cash. The nearest debt maturity is in January 2026, or three years from now. Management has been proven wise in pushing out debt maturities by locking in lowish interest rates over the last couple of years. Since no debt has to be refinanced in the near term, rising interest rates should be a tailwind for Capital Southwest in the foreseeable future (as CSWC can demand higher rates from portfolio companies). Especially CSWC’s 3.4%-yielding notes due in late 2026 look attractive in the current inflation and interest rate environment from the company’s perspective. Debt to equity stood at 1.11 at the end of the most recent quarter, down from 1.23 one year earlier — which, again, suggests that CSWC is becoming a lower-risk investment over time, which makes the recent share price swoon even more surprising.

A Compelling Yield At A Reasonable Price

This share price decline — CSWC is down more than 30% over the last twelve months — has made Capital Southwest’s dividend yield soar to a very attractive level of 12.2%, even before accounting for supplemental dividends that push up the yield to an even higher level.

Business development companies aren’t growth vehicles, thus the majority of total returns can be expected to stem from dividend payments. But with a starting yield this high, not a lot of growth is needed. In fact, I’d say that no underlying growth is needed at all — even if the company were to just pay the current dividend forever, without increasing it or offering any share price gains, the outcome would be favorable for income investors and total return seekers alike.

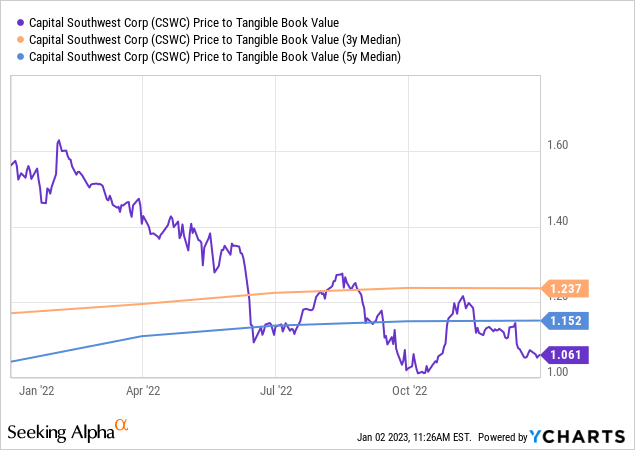

Some share price upside can be expected, over time, however. Not only has Capital Southwest grown its net asset value per share over time, but the stock could also benefit from multiple expansion tailwinds going forward, as shares are currently trading at a below-average valuation.

Today, the stock is valued at 1.06x tangible book value. The median tangible book value multiple over the last three to five years is in the 1.2x range. We can thus say that shares are currently underpriced by around 15% versus where Capital Southwest used to trade in recent years.

Of course, there is no guarantee that Capital Southwest’s tangible book value multiple will expand to the 1.15x to 1.25x range it was in in the past. It is possible that CSWC forever trades at a lower book value multiple in the future, or the book value multiple might even compress further. But historic patterns suggest that CSWC is likely undervalued right now, not overvalued. Some upside potential over the near to medium term would thus be far from surprising, I believe.

Takeaway

Capital Southwest is a quality BDC that invests in low-risk first-lien loans primarily. Risks across its portfolio are low, and credit quality is high. The balance sheet is looking healthy as well, and profits are climbing.

And yet, CSWC has dropped considerably over the last year, which has made its dividend yield soar deep into the double-digits. With shares offering a 12% yield while trading at an inexpensive valuation, Capital Southwest looks interesting for income investors at current prices.

Be the first to comment