Darren415

This article was first released to Systematic Income subscribers and free trials on Feb. 7.

In this article we discuss the latest quarterly results from the business development company (“BDC”) Capital Southwest (NASDAQ:CSWC). The company delivered a 1.5% total NAV return over the quarter and hiked the base dividend by 2% while re-declaring its supplemental dividend. CSWC trades at a 11.9% total dividend yield.

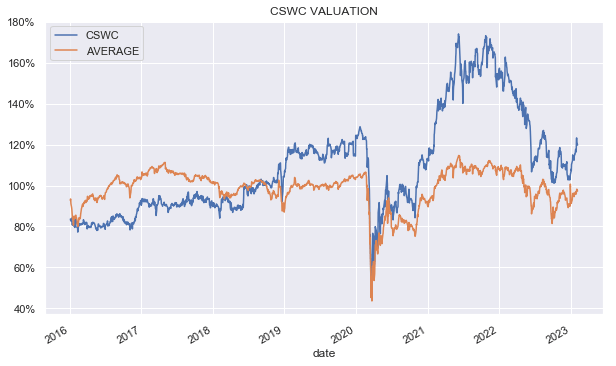

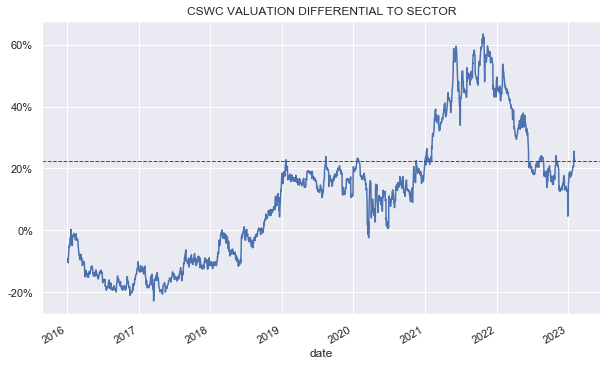

Our previous bullish article on the stock was published in mid-October, when the stock’s valuation had deflated to a much more reasonable level of 103%, or 16% above the sector average. As of this writing, it’s trading at a valuation of 120%, or 23% above the sector average. This sharp recovery leaves less of a margin of safety and keeps us on the sidelines at the moment.

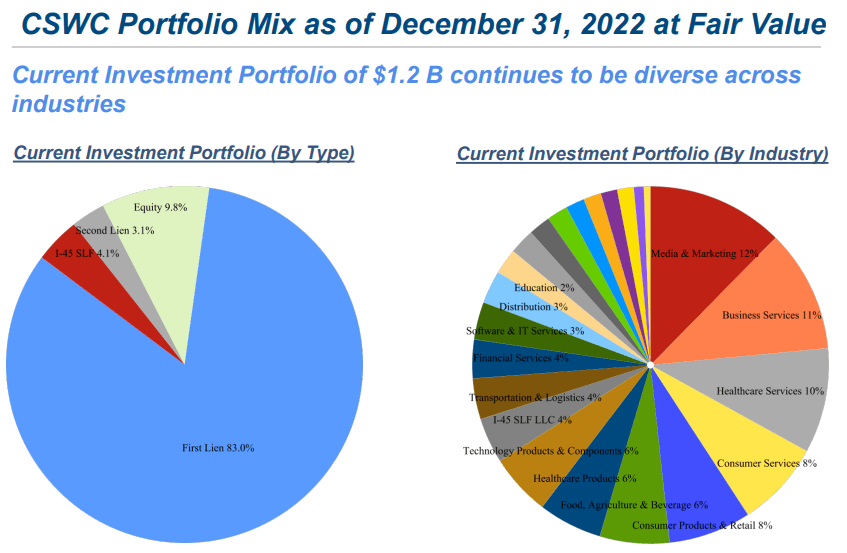

The company has a focus on first-lien loans – at around 10% above the sector average with sub-sector overweights in Media, Marketing & Entertainment as well as Business Services, as the following chart shows. Its allocations target primarily the lower middle-market segment.

CSWC

Quarter Update

Net income over the quarter rose by 11%. CSWC reports headline net income on a pre-tax basis, which is a little unusual in the sector. On a post-tax basis, the numbers were even more impressive, with a 20% quarterly jump. In the rest of the article, we will use post-tax figures as we do for other BDCs.

Systematic Income BDC Tool

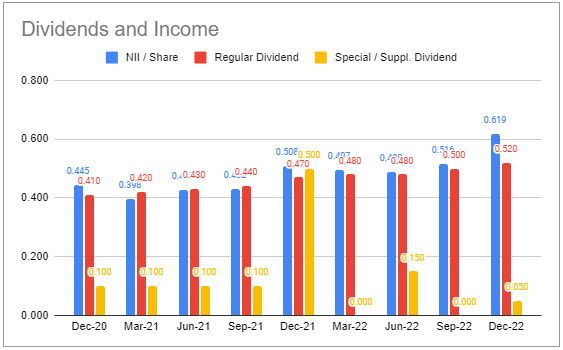

Base dividend coverage rose to a strong 119% while total dividend coverage (CSWC paid out a $0.05 supplemental in addition to a $0.52 base dividend last quarter) came in at 109%.

Given rising net income trends and already high coverage, the company hiked the base dividend by a penny to $0.53 while redeclaring the $0.05 supplemental. Even on a pre-tax basis this looks a bit stingy, as coverage with the new dividend is 107% without taking into account a rising net income trajectory over the coming quarter.

CSWC seems to be leaving room for further hikes over the rest of the year, as the Fed has already slowed down its pace of hikes, creating less of a tailwind for net income. The explicit strategy of the company is to be able to keep the dividend flat even if the Fed takes its policy rate down meaningfully.

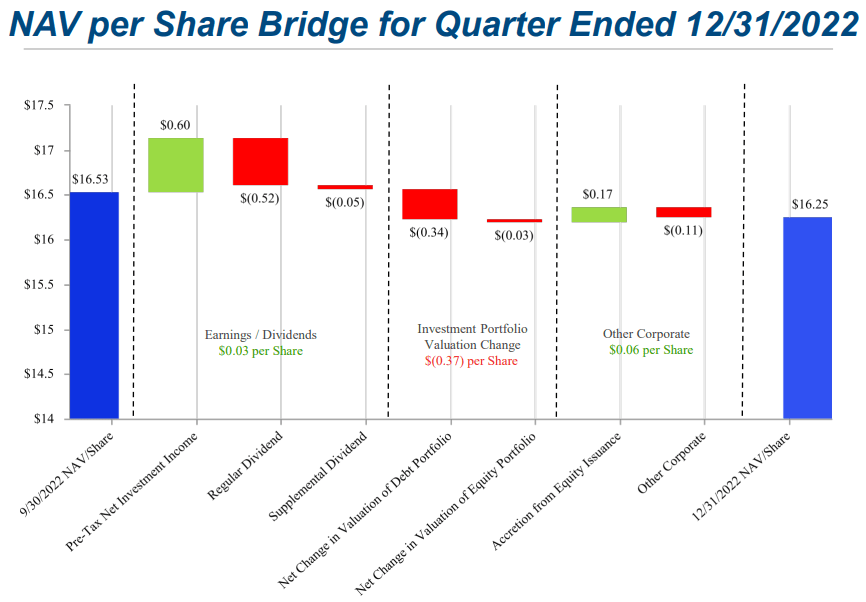

The NAV fell 1.7%, primarily as a result of the fall in the mark-to-market of the portfolio. The company raised $104m of new equity both through its at-the-market program as well as an underwritten offering, at a 9% premium to NAV, which drove a 1% return tailwind.

CSWC

Income Dynamics

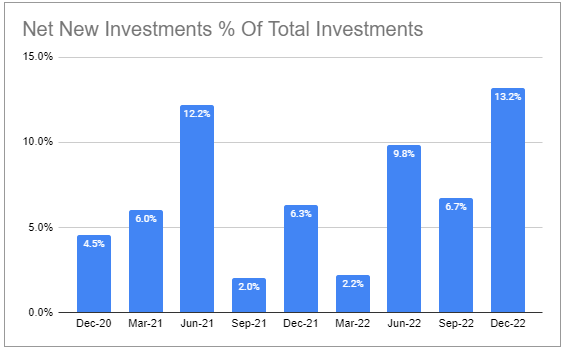

Net new investments continued to power ahead. Normally, this would be a tailwind for net income. However, in the case of CSWC this was entirely driven by its equity issuance, and this is actually dilutive to income.

Systematic Income BDC Tool

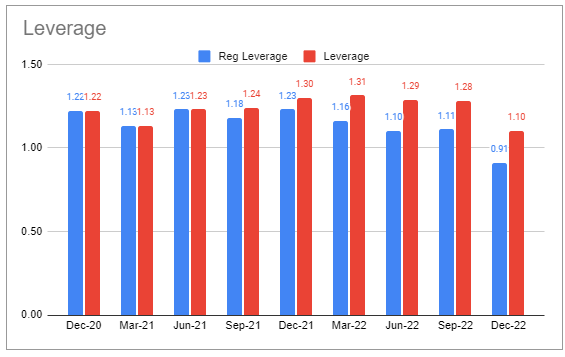

Because outstanding debt rose only marginally, leverage fell to 1.1x, which is near the bottom of its 1.1-1.3x target. Management has guided that they want to run leverage at the lower end of the target range in case the economy enters a recession.

Systematic Income BDC Tool

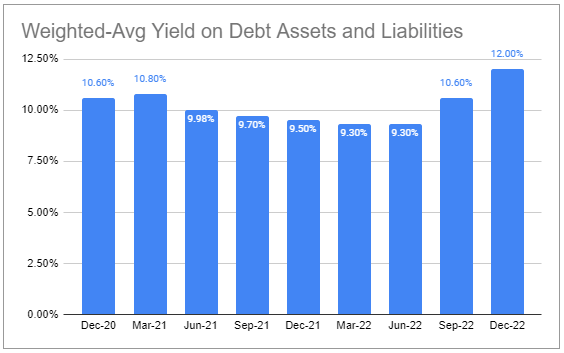

Weighted-average yield on debt assets jumped by 1.4% to 12%, as the rise in short-term rates accelerated over Q3 of last year.

Systematic Income BDC Tool

The company has indicated that the base rate index (i.e., Libor / SOFR) used to calculate interest on most of the loans in the portfolio reset 1% higher in January from its October level. This significant increase quarter-over-quarter will provide another immediate step-up in portfolio income in the March quarter. This means we can expect another mid-to-high single-digit jump in net income next quarter, all else equal.

Systematic Income BDC Tool

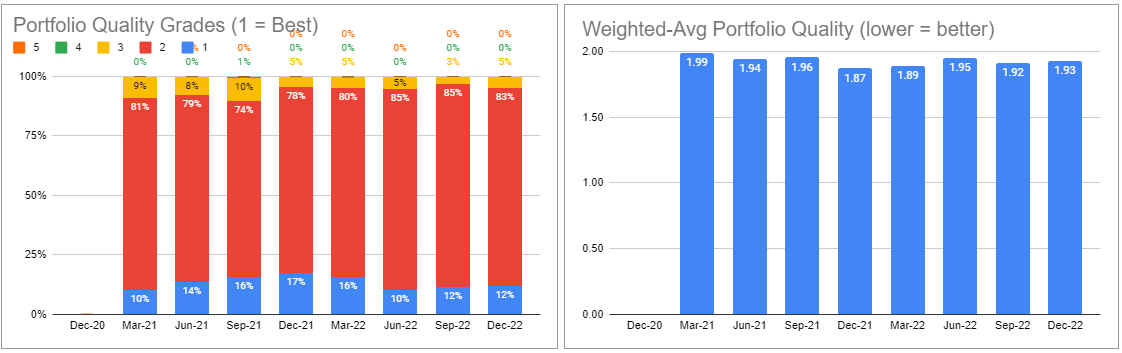

Portfolio Quality

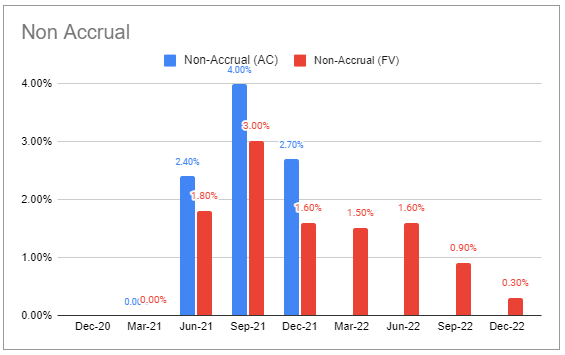

Non-accruals were very low at just 0.3% on a fair-value basis.

Systematic Income BDC Tool

Portfolio quality, as guided by internal ratings, was little changed.

Systematic Income BDC Tool

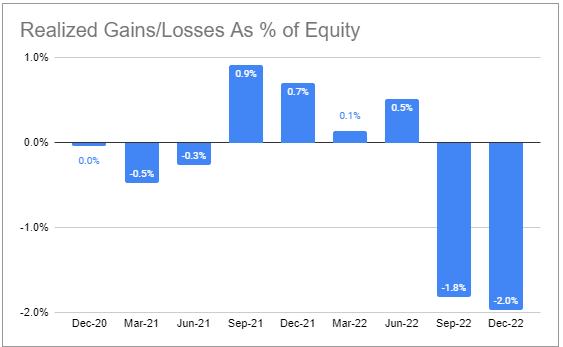

One thing to watch is the pace of net realized losses, which was elevated for the second quarter in a row.

Systematic Income BDC Tool

Management guided that loan-to-value levels on new deals continue to fall, which improves overall portfolio quality. Weighted-average company leverage also fell to 3.9x from 4.1x, which is good to see.

Return And Valuation Profile

Capital Southwest has delivered sector-beating returns in total NAV terms, with particularly strong returns over the last 3 years of 14.1% CAGR, or 3% above the sector average level. A key factor that has supported Capital Southwest’s strong returns is its relatively low operating costs, which is largely a function of its internal management structure.

Systematic Income BDC Tool

The second unusual source of returns is its continued level of equity issuance at a premium to NAV, however, this tailwind is strictly conditional on its valuation remaining high.

Given its strong historic return, it’s no surprise, therefore, that Capital Southwest stock continues to trade at a hefty valuation premium versus the sector, as the following chart shows.

Systematic Income

Its current 23% excess valuation over the sector average is far from the peak of 60% it achieved in late 2021.

Systematic Income

Factors Of Differentiation

There are a few points of differentiation that Capital Southwest offers relative to the sector which may be useful for investors building a diversified BDC portfolio.

The company is focused primarily on the lower middle market segment, which can be a good counterpart to other popular BDCs that focus on the upper middle-market space, such as Ares Capital (ARCC) or Oaktree Specialty Lending (OCSL).

CSWC has a larger than average secured loan focus, with a larger allocation to first-lien loans than the average BDC.

Finally, as highlighted above, it has an unusual and high, though conditional, additional source of returns via its above-NAV equity offerings.

Takeaways

Capital Southwest continues to perform well, generating a respectable 1.5% total NAV return over the previous quarter and raising its base dividend once again. It is very likely to further grow its income next quarter given the baked-in net income rise in its portfolio, which should result in another dividend hike.

Overall, Capital Southwest portfolio quality remains good, however, investors should watch its net realized losses, as these have increased lately. Separately, the company has generated an amazing 5.6% in total NAV return just from accretive share issuance over the past 4 quarters. This dynamic creates a kind of positive feedback loop where above-NAV share issuance drives strong returns which, in turn, cause the stock to continue to trade above the NAV. The risk is that if this feedback loop is broken, Capital Southwest will likely become an average performer (which it is if we strip out the total return contribution from share issuance), causing its valuation to fall, removing an important return support.

Be the first to comment