Sergei Dubrovskii/E+ via Getty Images

Investment Thesis

Canadian Natural Resources (NYSE:CNQ) is the largest crude oil producer in Canada.

In the analysis that follows, I discuss the dynamics that will lead to a strong oil market in 2023.

Also, how a strong oil market will mean that CNQ’s dividend will increase. Thus, I lay out why CNQ’s dividend will reach a +5% yield from current prices before we know it.

Why Canadian Natural Resources?

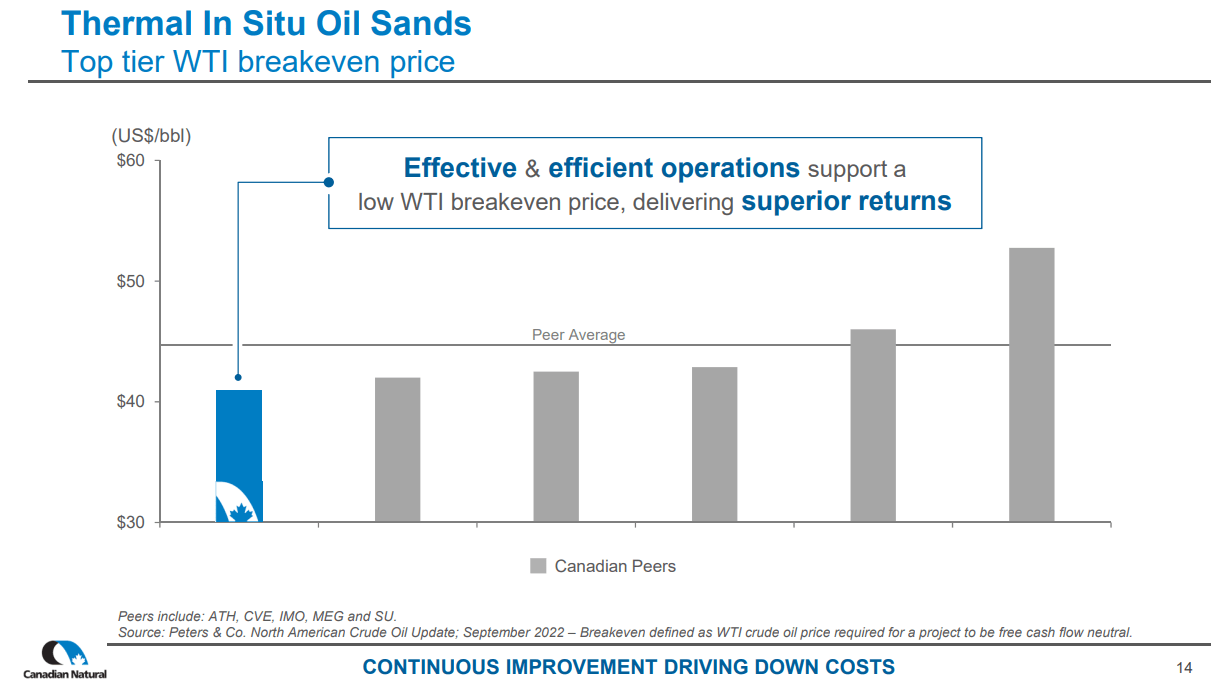

In the first instance, CNQ has a low breakeven price of close to $40 WTI. That means that even if WTI were to remain low in 2023, CNQ would likely be profitable.

CNQ January presentation

Put another way, if for whatever reason, WTI was to fall in 2023, many other companies would be unprofitable and cut back on production, before CNQ.

That margin of safety, in and of itself, should carry a premium in CNQ’s valuation.

Secondly, I strongly believe that the oil market isn’t acting rationally. The reason why oil prices have come down is that there’s an overwhelming fear that with a global recession potentially on the cards, oil consumption will fall.

However, I don’t buy this argument on three counts.

Reasons For High Oil Prices In 2023

Here are three reasons why oil will be strong in 2023.

China is starting to reopen. After nearly 3 years of being closed, we can expect its economy to start and stop. It will not be a smooth start. The same as it wasn’t a smooth reopening in the US and many counties in Europe.

But directionally, China is reopening and this will lead to a surge in oil consumption.

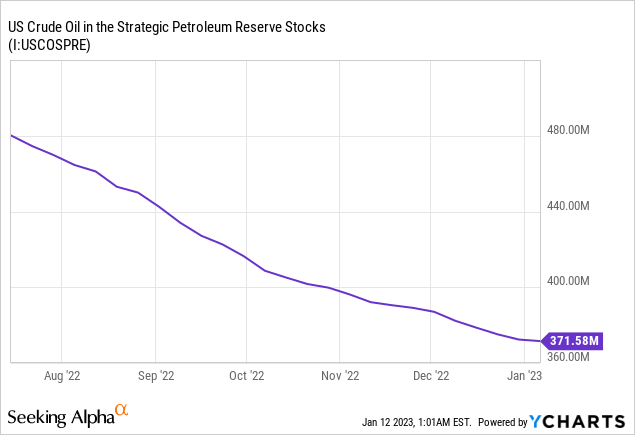

Next, we’ll discuss the Strategic Petroleum Reserve.

What you see above, is that throughout 2022 there was a large inflow of oil into the market from the SPR.

However, this release has mostly stopped. That means that a sudden shock to the tight oil market in the form of excess supply is not likely to be in place in 2023.

Finally, I don’t believe that demand for oil will fall as much as feared. Recall, the vast majority of oil is used in transportation. With air travel expected to be strong in 2023 as businesses and households resume traveling, as disruption eases, together with supply disruptions starting to ease too, this will lead to increased shipping and freighting. Consequently, altogether, I don’t believe we’ll see a substantial fall in oil demand.

Accordingly, given this stable backdrop to oil prices, allow me to now discuss CNQ’s dividend.

At Least A +5% Dividend Yield

CNQ January presentation

For 2022, CNQ had one CAD$1.50 special dividend per common share. If we assume that this special dividend doesn’t repeat, CNQ’s annualized dividend will reach CAD$3.40.

This translates into a dividend yield of 4.5%.

That being said, I believe that CNQ has room to further increase its declared dividend. Particularly if the oil market in 2023 ends up being stronger than it’s currently priced at.

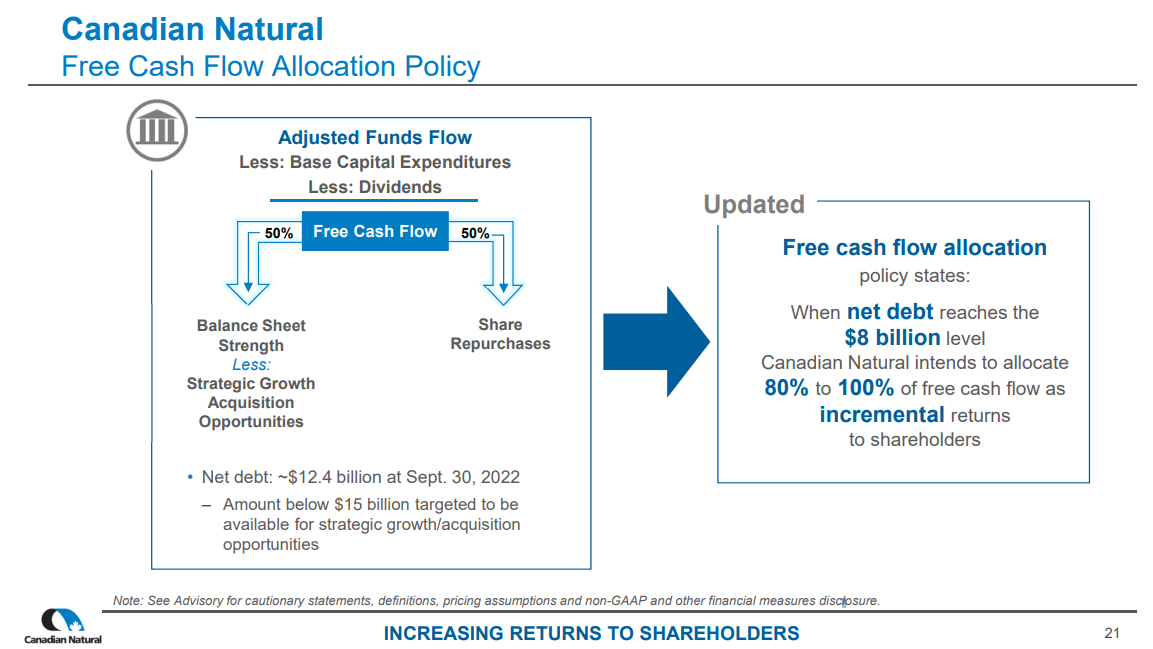

What’s more, consider CNQ’s newly updated dividend policy.

CNQ January presentation

On the left, we see CNQ’s capital allocation priority up until Q3 2022.

CNQ was committing to return 50% of its free cash flow to shareholders, after paying out its dividend and deploying excess free cash flow to its balance sheet.

Now, its newly updated capital allocation policy states that when its net debt falls to CAD$8 billion, CNQ will return 80% to 100% of its free cash flow to shareholders.

We know that CNQ’s balance sheet will have exited 2022 with approximately $10 billion of net debt.

We also know that CNQ makes very approximately CAD$2 billion of free cash flow per quarter at current WTI prices.

That means that before the summer, CNQ will be in a position to further increase its dividend.

What’s more, given that CNQ continues to repurchase shares, that will mean that the same corporate dividend payout will be higher per share.

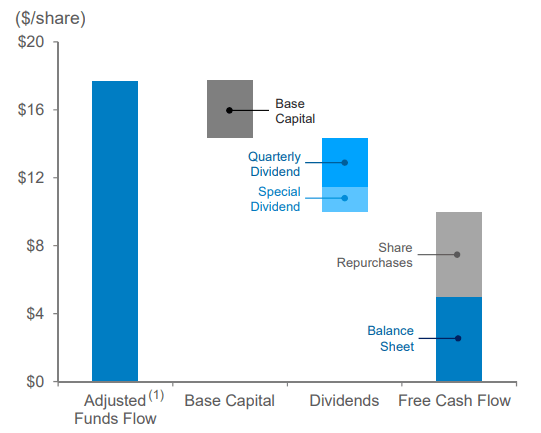

CNQ January presentation

As you can see above, CNQ has been buying back and returning capital to shareholders via buybacks. That means that before the summer, CNQ’s dividend per share could be annualizing CAD$4.00 on a sustainable base dividend.

The Bottom Line

Canadian Natural Resources is a large, stable, crude oil producer, with a rewarding dividend, that I believe in the coming months could reach a +5% yield from current prices.

Be the first to comment