Bloomberg/Bloomberg via Getty Images

Introduction

All financial data are reported in CAD

One of the things I learned from Warren Buffett last year was to understand how he came to realize that railroads – and capital-intensive businesses more in general – can be rewarding investments. Afterwards, I started assessing the five major North American Class 1 railroads according to the criteria Buffett showed to follow.

In this article, we are going to go over the newly released Canadian National (NYSE:CNI) Q4 earnings report to understand if the company performed according to expectations and to see what we can expect from the future.

Summary of previous coverage

I still suggest reading my initial article: Learning From Buffett And Berkshire About Investing In Railroads: The BNSF Case Study. Here I share what I learned and how I research railroads. In summary, there are four intertwining sides to be considered: earning power, interest coverage, fuel-efficiency, use of capital (rate of return).

After this article, I published the whole series. You can find it at the bottom of this article.

The result of this research was as follows: Canadian National, Union Pacific (UNP), and CSX (CSX) seemed to be the best three picks in the order I just wrote.

Regarding Canadian National, I came to appreciate its three-coastal network and its exclusive partnership with Union Pacific and Norfolk Southern (NSC) in Equipment Management Pool (EMP) program, an interline service that enables shippers to use more networks, providing seamless access to most of the major cities across the whole North-American continent, from Canada to Mexico.

Canadian National has also shown to be very cost-conscious, especially about fuel costs. This is why it was a pioneer in Precision Scheduled Railroading (PSR), which has let to better network efficiency, even though with some disputes with workers that asked for wage increases and better schedules.

Canadian National is also exposed to petroleum, chemicals, grains, and fertilizers. Since, 2022 Canadian harvest was particularly rich, the company is clearly set to benefit greatly from this, thanks to its new 500 grain hoppers bought in 2022.

We also saw its pre-tax earnings/interest ratio going up from 10.37 at the end of 2021 to 13.38 for the TTM at the end of 3Q 2022. This is a big earning power increase.

As per efficiency, Canadian National’s operating ratio is once again below 60%, coming in as low as 57% in Q3.

Quite impressively, while fuel costs increased, Canadian National managed once again to optimize its fuel consumption, with 0.838 US gallons of fuel consumed per 1,000 GTMs. Most of its peers are in the range between 0.96 and 1.11.

The company is also increasing its ROIC and it guided for a target of 15% at the end of 2022.

Regarding its use of capital, Canadian National has proven to investors it can keep is capex under 17% of total revenues, enough to enhance safety and integrity of track infrastructure while developing new facilities such as Canada’s hub for petrochemical production and refining in Alberta.

With the excess cash, Canadian National spent $3.5 billion to repurchase 23 million shares. At the same time, it increased its dividend increase by 19% while keeping its payout ratio at 37%.

Q4 and FY22 Results

I think the recently reported results were somewhat expected.

Revenues for the quarter were up 21% YoY to $4.54 billion, thanks to bulk segments leading the charge with strong growth.

On the other side, the railroad is seeing some weakness in forest products and intermodal. These segments generated higher revenues YoY, but the number of carloads decreased YoY by 1% for forest products and 7% for intermodal. Petroleum and chemicals are also showing some weakness, with revenues up only 5% and carloads barely up 1% YoY.

Let’s quickly look at a few other reported data before making some considerations.

- Operating income increased 22% YoY to $1.91 billion.

- Diluted EPS increased 24 to $2.10.

- Operating ratio (operating expenses as a % of revenues) improved by 0.4 percentage points, ending up at 57.9%.

This quarter closed a very strong 2022 for the company, where revenues went up 18% YoY to $17.1 billion, with an operating income of $6.84 billion (+22%). This led to an operating ratio of 60%, a 1.2 points improvement YoY. Diluted EPS of $7.44 (+8%, +25% if adjusted).

Most importantly, free cash flow increased 29% to $4.26 billion, better than what the company expected.

Last, but not least, return on invested capital reached 15.8%, above the company’s guidance of 15%.

Understanding the report

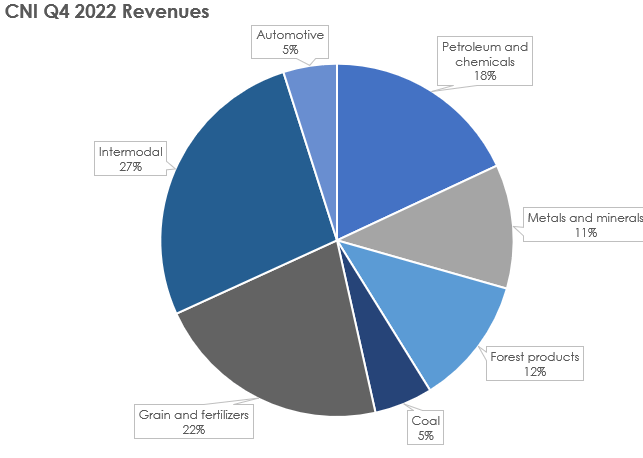

Let’s take a look at the new revenues mix.

Author, with data from CNI Q4 Earnings Report

Compared to what we saw a few months ago, grain and fertilizers have increased its weight, while intermodal decreased from 31% to 27%.

Canadian grain was strong thanks to the huge harvest. However, as the Mississippi River water levels were low in the fall, U.S. grain train shipments beat the 2006 record as the supply chain had to shift to railroad.

Coal demand set a record in 2022 with over 30 million tons shipped for the full year. No wonder automotive volumes were strong in the quarter: inventory replenishment is continuing across the industry.

Weakness appears through a softening in international intermodal as volumes diminished due to inventory overstocking.

The company also reported that lumber and panels decreased following additional mill curtailments in British Columbia due to low commodity prices, high stumpage fees in BC and lower housing demand due to rising interest rates.

Now, what I would like to point out is this: railroads are exposed to different segments that follow different macro-trends and economic cycles. This creates a well-balanced exposure that mitigates downside risks of one particular segment. This year, for example, the strong harvest is making up for a slowing intermodal segment. True, most of these segments are related to commodities, but these commodities are linked to different needs and industries.

Earning power

Let’s dig deeper into the numbers and let’s see what has happened to the most important metric according to Buffett: earning power. That is, the power a capital intensive business has to cover its interest expenses. It is calculated as pre-tax earnings over interest expense. At the end of 2022, Canadian National scores a 12.34 which is much higher compared to the 10.37 it had at the end of 2021. The company keeps on leading the industry, confirming its conservative management of capital.

Efficiency

I think here we have to listen to a few things that were said during the last earnings call. The company, in fact, is undertaking a turnaround project to improve the way it runs its network. Edmond Harris, Canadian National EVP and COO, explained how the company focused on increasing train speed:

Railroading needs to remain simple. Velocity creates capacity, the faster we are, the more we can handle.

Car velocity averaged 207 miles per day in the fourth quarter, up 10% from last year, while origin train performance averaged 85% in quarter 4, also up 10% from last year.

So far this month alone, car velocity is hovering near 220 car miles per day, similar to the numbers that this company saw last summer. Now winter is far from over, but compared to last year, we are in a much better position to start the year, and it means we should be in a better position to come out of winter into the spring.

The mechanical team is bolstering in modernizing our fleet of locomotives with camera technology and energy management systems, which will help us be more efficient with fuel and safer.

At the same time, Canadian National kept under control train length, reducing it when needed, and fuel costs. In Q4 Fuel efficiency improved once again by 1% to 0.886 US gallons per 1,000 GTMs. For the whole year, it actually improved by 2% to 0.867 US gallons per 1,000 GTMs.

I think it is also worth reading what Ghislain Houle, CFO of the company, said to explain the trajectory Canadian National means to go to become even more efficient:

the next path on this, the next step is really to sell into the capacity that we’ve unveiled as we’ve kind of advanced the scheduled plan then. So we can now see where we’ve got train capacity in corridors and where we have capacity on trains that aren’t running yet to maximum length.

I think these words do tell Canadian National still has room to improve further, leading to even better margins and results. Coupled with a best-in-class operating margin under 60% and a conservative balance sheet, the company seems to me quite strong and ready to withstand any economic turmoil while being able to profit from the following rebound.

There is one last aspect I want to point out before moving on: in 2023 I would like to monitor how the EMP program signed with Union Pacific and Norfolk Southern will lead to new gains and better results. At the end of Q4 the company reported it was fully integrated with its two partners, averaging $1 million per week in this new interline domestic intermodal business.

Use of capital

Canadian National topped estimates by reaching a ROIC of almost 16%, as we have already seen. This is, once again, a metric where the company is an industry leader.

Canadian National confirmed its conservative policy by raising its dividend by 7.8%, a good increase that doesn’t endangered the balance sheet nor commits the company to a perilous payout ratio that could risk to not be sustainable in case of a big recession. Canadian National also announced a new $4 billion buyback plan where the company can repurchase, for cancellation, up to 32 million shares over 12 months, representing 4.8% of its currently outstanding stock.

As far as capex goes, there are no particular news and we can assume the company is sticking to its target of keeping capex under 17% of revenues.

Outlook

Now, I think it may be interesting for investors to know a few things about the economic outlook the company reported. In fact, it offers useful insights on different industries where many of us may be already invested or are planning to be invested in. Let me hand the word over to Canadian National’s management team:

The weakness that we began seeing in the fourth quarter is expected to persist through at least the first half of 2023. The international intermodal will have multiple blank sailings as the North American inventories rebalance.

Lumber will be slow to recover due to market oversupply and high interest rates dampening demand. Chemical and petroleum production is directly tied to the economy, so we expect demand to be soft in the first half of 2023. Automobiles are still in a tight supply situation, but this is changing with higher interest rates as well as part shortages.

This is why the company guided for low single-digit EPS growth for 2023. Some analysts were concerned as they rightly thought this year EPS growth could be fueled only by share buybacks. However, if I am understanding correctly how Canadian National operates, its first guidance is usually quite prudent and, as we have seen many times, it often revises it upwards in most economic conditions. I wouldn’t be surprised if, in case of a mild recession, the company ended up with a 7% EPS growth at the end of 2023.

Conclusion

Overall, I stick to my buy rating and I actually believe there could be the chance to pick up some shares at a discount given recent volatility. In my previous articles (look at the bottom of this article) I explained why the company is trading around fair value in case of a mild recession scenario. Buying at fair value is already an opportunity. For sure, if the stock falls below $100 we enter into a very interesting buying opportunity. In fact, the company seems to be able to compound at a reasonable rate of return that justifies the current price. Clearly, we are talking about a long-term investment. In fact, over the short term it might actually drop a little further. I bet many are waiting to pick it up below $100. As for me, I am behaving like this: today I bought my first little chunk while keeping some cash aside to dollar cost average into the stock during the upcoming months.

The series

For those interested in reading the previous episodes, here are the links:

- Looking At Railroads As Mr. Buffett Does: Canadian National Railway

- Looking At Railroads As Mr. Buffett Does: Canadian Pacific

- Looking At Railroads As Mr. Buffett Does: Norfolk Southern

- Looking At Railroads As Mr. Buffett Does: CSX Corporation

- Looking At Railroads As Mr. Buffett Does: Union Pacific

Follow-up articles of this series can be read here:

Be the first to comment