MarioGuti/iStock via Getty Images

Introduction

Expanding your investment portfolio to include Canadian stocks can offer exciting new opportunities for growth and income. I’ve received numerous requests to delve into this market and, after recently increasing my position in Canadian Pacific Railway (CP) and putting several other Canadian stocks on my watchlist, I understand the appeal.

In this article, I will present my top picks for Canadian dividend stocks. These companies have been selected based on their attractive yields, consistent dividend growth, strong business models, and potential for delivering satisfying long-term returns.

So, without any further ado, let’s take a closer look at the Canadian market and discover the best investment opportunities this country has to offer!

Reasons To Go Canadian

There are some compelling reasons to invest money in Canada, even if you’re not Canadian.

-

Diversification: Investing in Canadian dividend stocks can provide diversification for investors who primarily hold U.S. stocks.

Canada isn’t necessarily a must-own nation for diversification. The MSCI World Index has 3.5% Canada exposure. This is in line with France (3.5%) and slightly below the UK (4.0%).

MSCI Inc.

However, there are good reasons to invest more than 4% in Canada. I currently have close to 5% exposure, and I see a high likelihood of boosting that number in the future.

- Financial stability: Many Canadian companies have a history of financial stability and have been consistently paying dividends for many years, making them an attractive option for income-seeking investors.

-

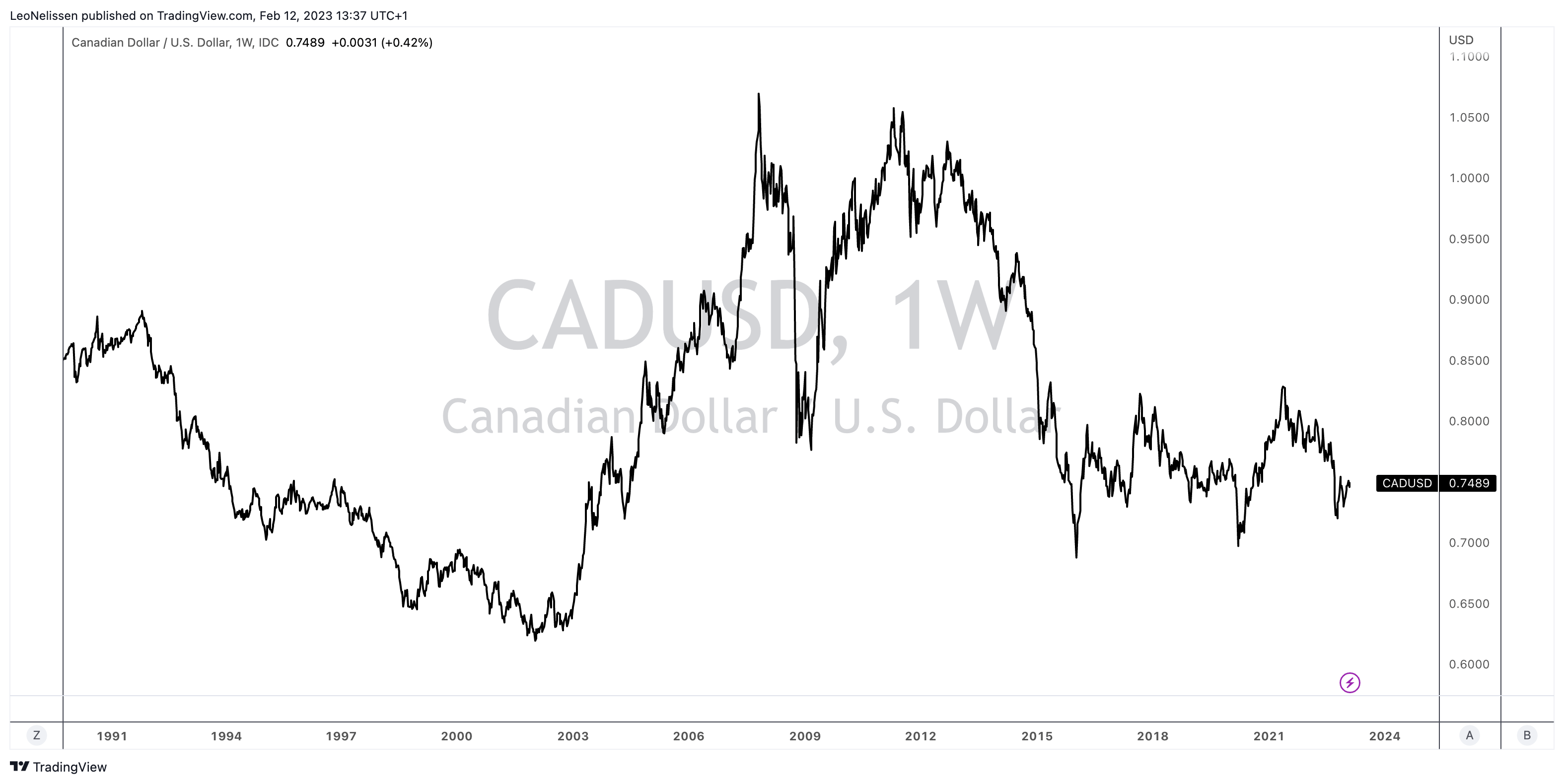

Strong currency: The Canadian dollar has historically been a strong currency, which can help protect against currency risk for foreign investors.

This is the CAD/USD currency pair (it follows commodity cycles, due to Canada’s commodity exposure):

TradingView (CAD/USD)

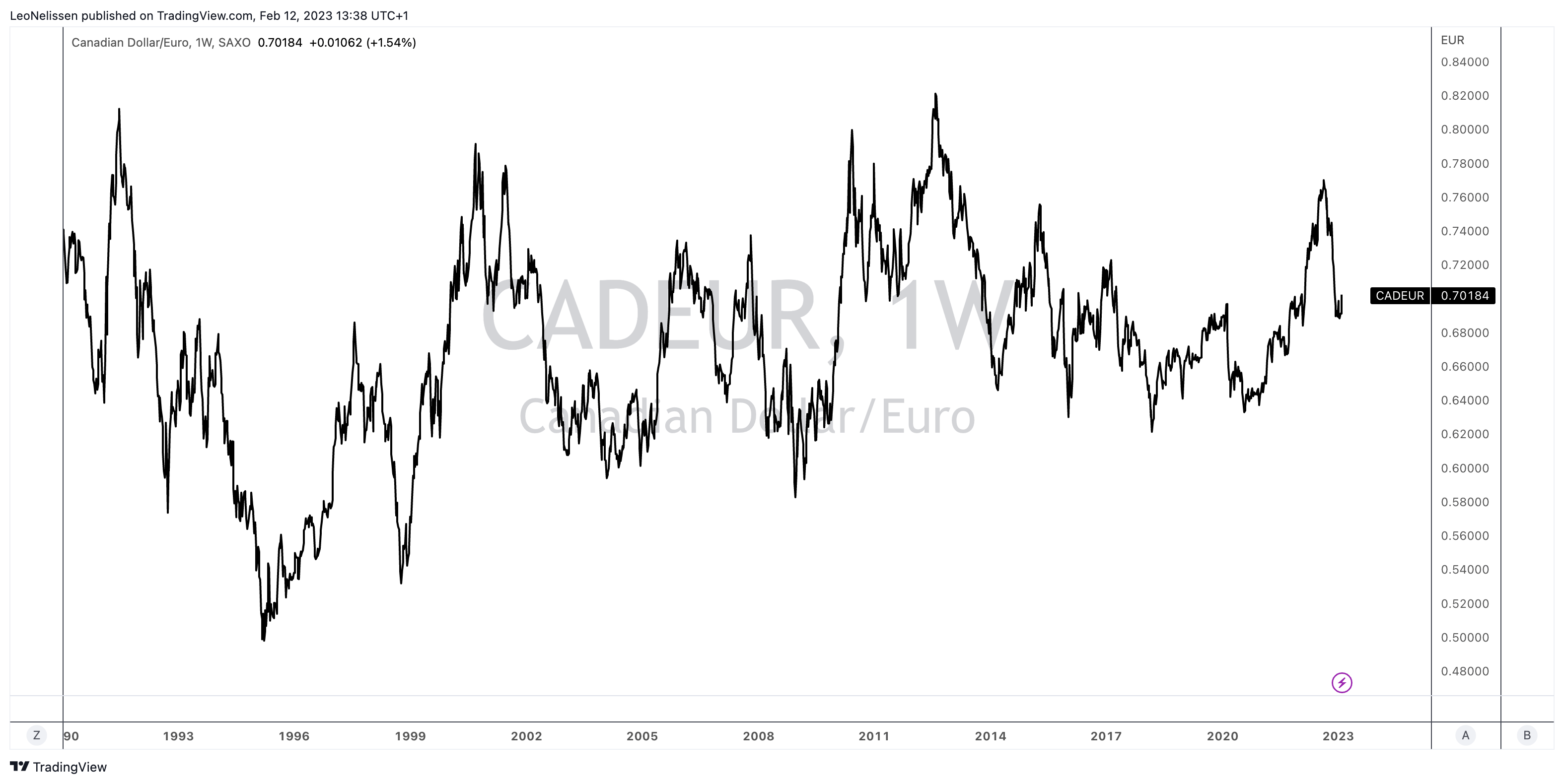

This is the CAD/EUR currency pair (it’s even less volatile):

TradingView (CAD/EUR)

-

Attractive yields: Canadian dividend stocks have generally offered attractive yields compared to other countries.

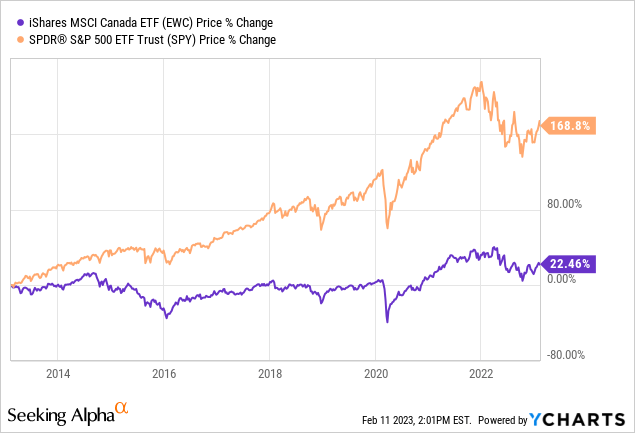

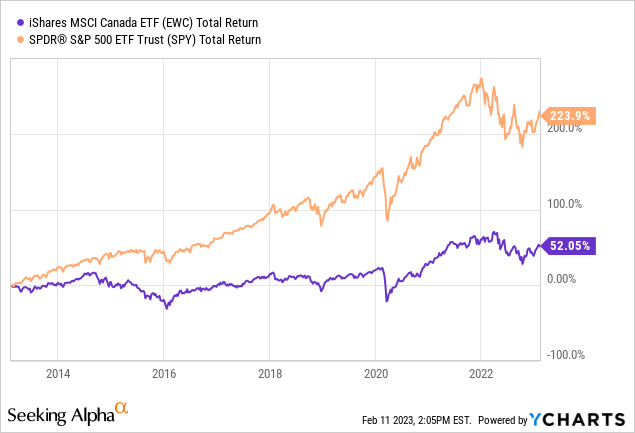

In light of the three bullet points above, Canadian stocks have generated 22.5% in capital gains over the past ten years. In this case, I’m using the iShares MSCI Canada ETF (EWC) as a benchmark. In other words, you’re looking at capital gains only. Moreover, this ETF is in US dollars.

22.5% in capital gains is terrible. It underperforms the S&P 500 by more than 140 points.

However, in light of what we just discussed, there’s still a good reason to invest in Canada: a decent yield.

Over the past ten years, the total return is 52%. That’s still poor, yet much better than the 22.5% return without dividends.

One of the reasons why Canada performed so poorly in the past ten years is that the biggest period was beneficial to low-inflation stocks like tech and growth stocks. This benefited the US more than any other country on Earth.

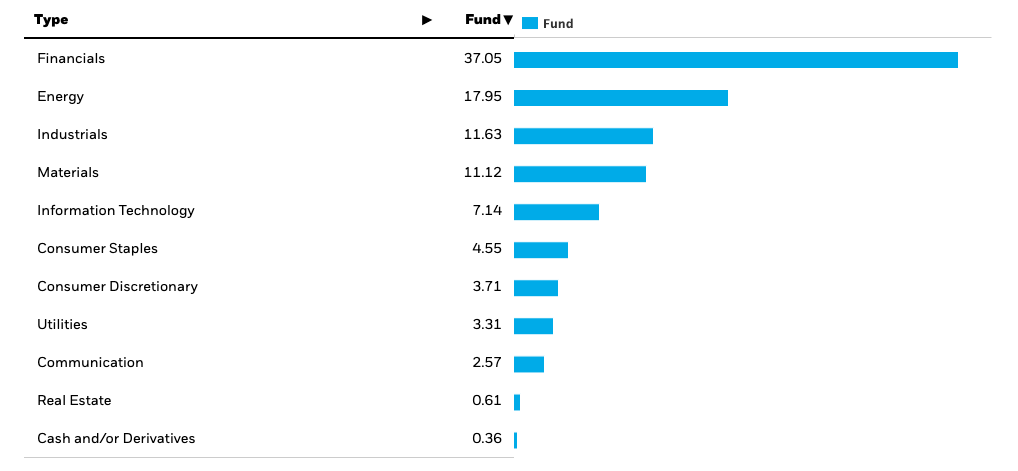

Canada is different. Using the EWC ETF as a benchmark again, we see that the ETF is dominated by large banks and commodity-related investments.

iShares

Hence, since the pandemic, Canadian stocks are finally outperforming again, thanks to higher inflation, higher rates, and a strong bull market in commodities.

-

Stable political and economic environment: Canada has a stable political and economic environment, which can provide some protection against market volatility.

While I am not a fan of the current government in Canada, there is no denying that Canada has a stable government, offering companies an environment that allows them to pursue long-term goals. This is different in a lot of emerging markets where political risks are just too high.

-

Tax benefits: In some cases, dividends from Canadian companies may be taxed at a lower rate than other types of investment income, making them an attractive option for tax-conscious investors.

Needless to say, the tax situation is dependent on your own situation. Personally, as an EU-based investor, I pay 15% on Canadian dividends, which is in line with the tax rate in my country. In most cases, Canadian withholding taxes are waived by i.e., the IRS. But please check your personal situation before making investment decisions.

About My Picks

With a focus on decent yields, sustainable and increasing dividends, and market-matching total returns, I carefully selected my Canadian stocks for this article. I consciously decided not to include Canadian banks in my portfolio, as I believe that there is ample opportunity for quality banking exposure within the country, and I am wary of the weakened housing market and high levels of leverage in the system.

To achieve higher yields, I chose to exclude Canadian Pacific, even though it is one of my favorite stocks, as its yield falls below 1.0%. If you’re interested in my thoughts on Canadian Pacific, I invite you to read one of the many articles I’ve written on the company (like this one).

All of the stocks I’ve selected are listed on the New York Stock Exchange, giving investors a more accessible avenue for investment. However, it’s important to note that dividends received in USD may be impacted by currency fluctuations, with a stronger CAD/USD supporting the value of dividends, and a weaker CAD/USD having the opposite effect.

In my opinion, as long as the dividend continues to grow consistently, the impact of currency fluctuations can be overlooked.

So, let’s start with stock number one.

Enbridge Inc. (ENB) – Oil & Gas Midstream – 6.6% Yield

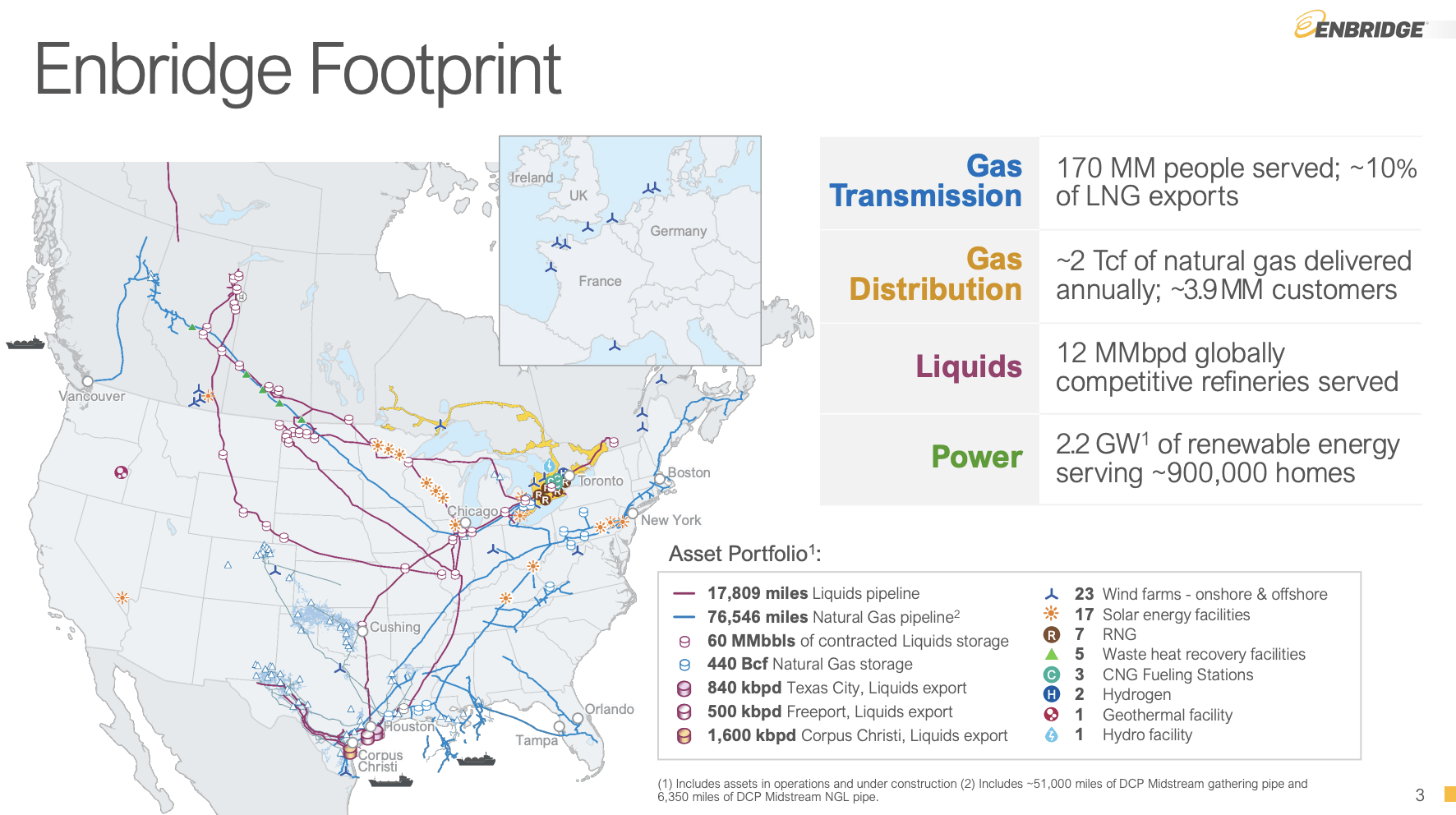

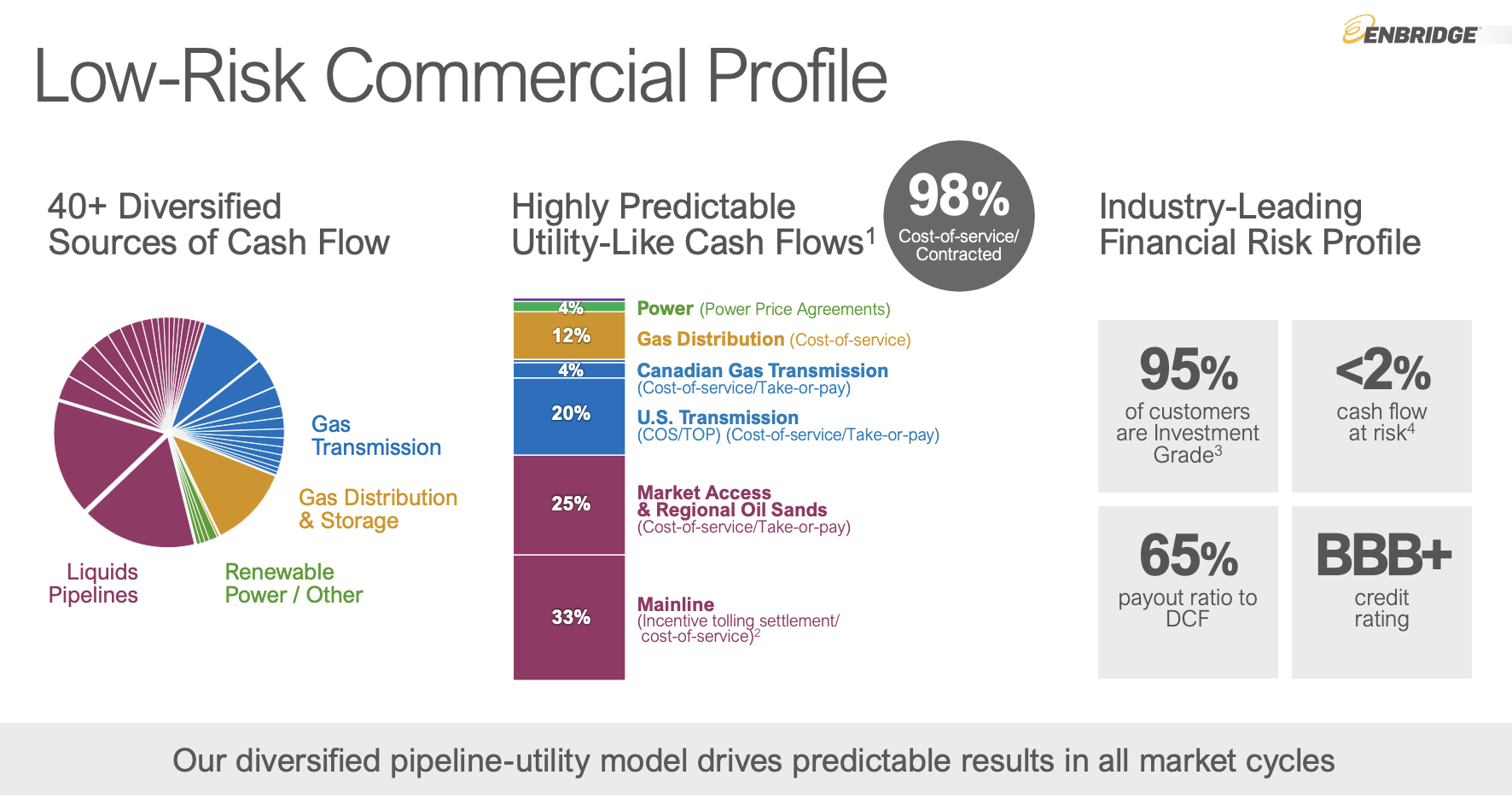

Enbridge Inc. is a Canadian-based midstream company that operates a vast network of pipelines connecting major energy hubs in both Canada and the United States. With a market cap of $80 billion, close to 18,000 miles of liquids pipeline, and 76,500 miles of natural gas pipeline, Enbridge is one of North America’s leading pipeline operators.

Enbridge Inc.

The majority of the company’s revenue comes from pipelines for liquids and gas transmission, which are protected by investment-grade balance sheets of its customers (95% of which have investment-grade balance sheets), and by Enbridge’s own BBB+ balance sheet.

Enbridge Inc.

Enbridge has growth opportunities through organic internal growth and external growth opportunities, including the LNG export market. The company expects North American LNG shipments to triple to more than 30 Bcf by 2040 and expects to have a 30% export share in the market.

Related to that, Enbridge also owns 30% of the Woodfibre LNG project and serves four plants on the Gulf Coast, with two more LNG facilities pending FID. The Woodfibre LNG project, which is expected to be online in 2027, is underpinned by two long-term offtake agreements with BP Gas Marketing Limited for 15 years, representing 70% of its capacity.

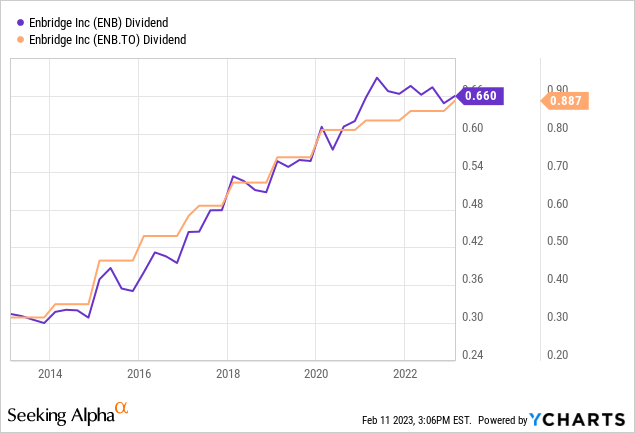

Despite the high costs of building and maintaining pipelines, storage, and related facilities, the company has reduced its capital expenditures and is now generating strong free cash flow, with an implied free cash flow yield of 7.5%. This supports Enbridge’s 6.5% dividend yield, which has grown by 7.4% per year over the past five years. The company’s 126% payout ratio may indicate the need for a dividend cut, but the company generates more free cash flow than net income, ensuring the safety of its dividend. This is because net income is impacted by billions in depreciation and other non-cash items. This makes it look like the company cannot service its dividends.

Enbridge is trading at a fair valuation of 12.4x forward EBITDA, with a current stock price of $40.60 and an average target of $43.90. With its strong LNG footprint, high dividend yield, and expected annual discounted cash flow growth of 5% to 7% through 2024, Enbridge is an attractive high-yield dividend stock for long-term investors.

After covering the stock in an LNG-focused article this month, I have put the stock on my high-yield watchlist.

Canadian National Railway (CNI) – Railroads – 2.0% Yield

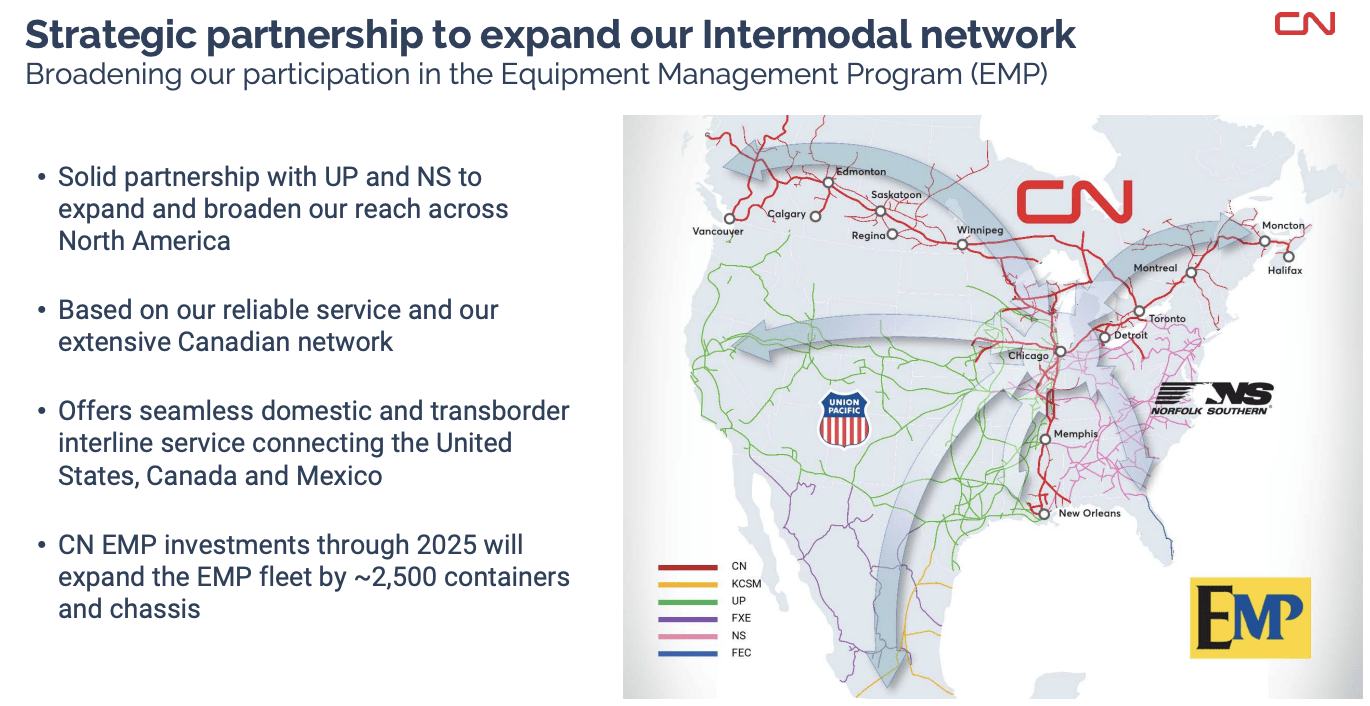

Canadian National is a leading transportation and logistics company that operates one of the largest rail networks in North America. With a market cap of $79 billion, CN is considered one of the largest and most diversified railway companies in the world. The company’s rail network spans across Canada and the United States, connecting key economic centers and allowing for efficient import and export operations. In addition to its vast network, CN also offers a range of complementary services, including intermodal and logistics solutions.

Canadian National

In recent years, CN has made significant investments in its infrastructure and technology, which has allowed the company to increase its operational efficiency and expand its partnerships with American peers. The company’s strong financials, growing dividend, and commitment to sustainability make it a compelling investment option for those looking to tap into the Canadian and North American economies.

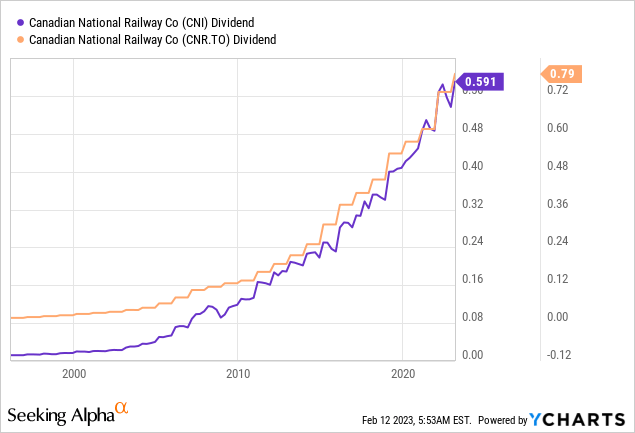

While its 2.0% yield certainly isn’t overly exciting, it comes with steady dividend growth. The company has 27 consecutive years of dividend increases, which includes the Great Financial Crisis.

These are the latest dividend growth rates:

- 10Y CAGR: 11.7%

- 5Y CAGR: 12.1%

- 3Y CAGR: 11.6%

The most recent hike was announced on January 24, when the company hiked by 7.8% to C$0.79 per share per quarter.

In general, the company accelerates dividend growth whenever economic growth is rebounding. It lowers dividend growth whenever it is faced with headwinds. However, it does not feel the urge to cut its dividend when economic growth goes south, thanks to a 40% payout ratio. The cash flow payout ratio is just 28%, which is good news for future dividend growth, especially if we incorporate that economic growth will eventually rebound again.

The company also engages in buybacks.

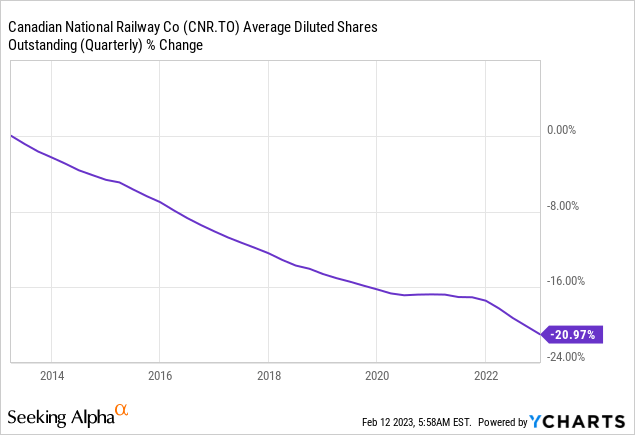

Over the past ten years, the company has bought back 21% of its shares outstanding.

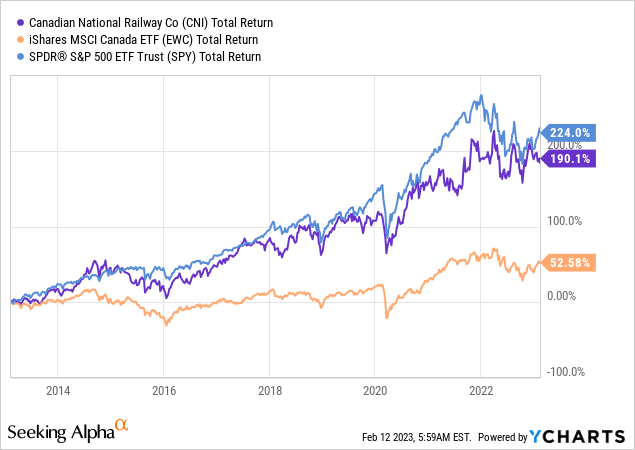

Despite underperforming compared to the S&P 500, Canadian National has demonstrated strong growth and is working to improve its operational efficiencies. I am optimistic that this will drive future outperformance. Additionally, I believe that the explosive growth of stocks over the past 12 years, which greatly benefited the S&P 500, may be difficult to replicate. Instead, I believe that value stocks will continue to be the optimal investment choice.

With that said, so far, we have covered energy and industrial stocks. Now, let me introduce a stock you may not be familiar with – unless you’re Canadian, of course.

Fortis Inc. (FTS) – Utilities – 4.1% Yield

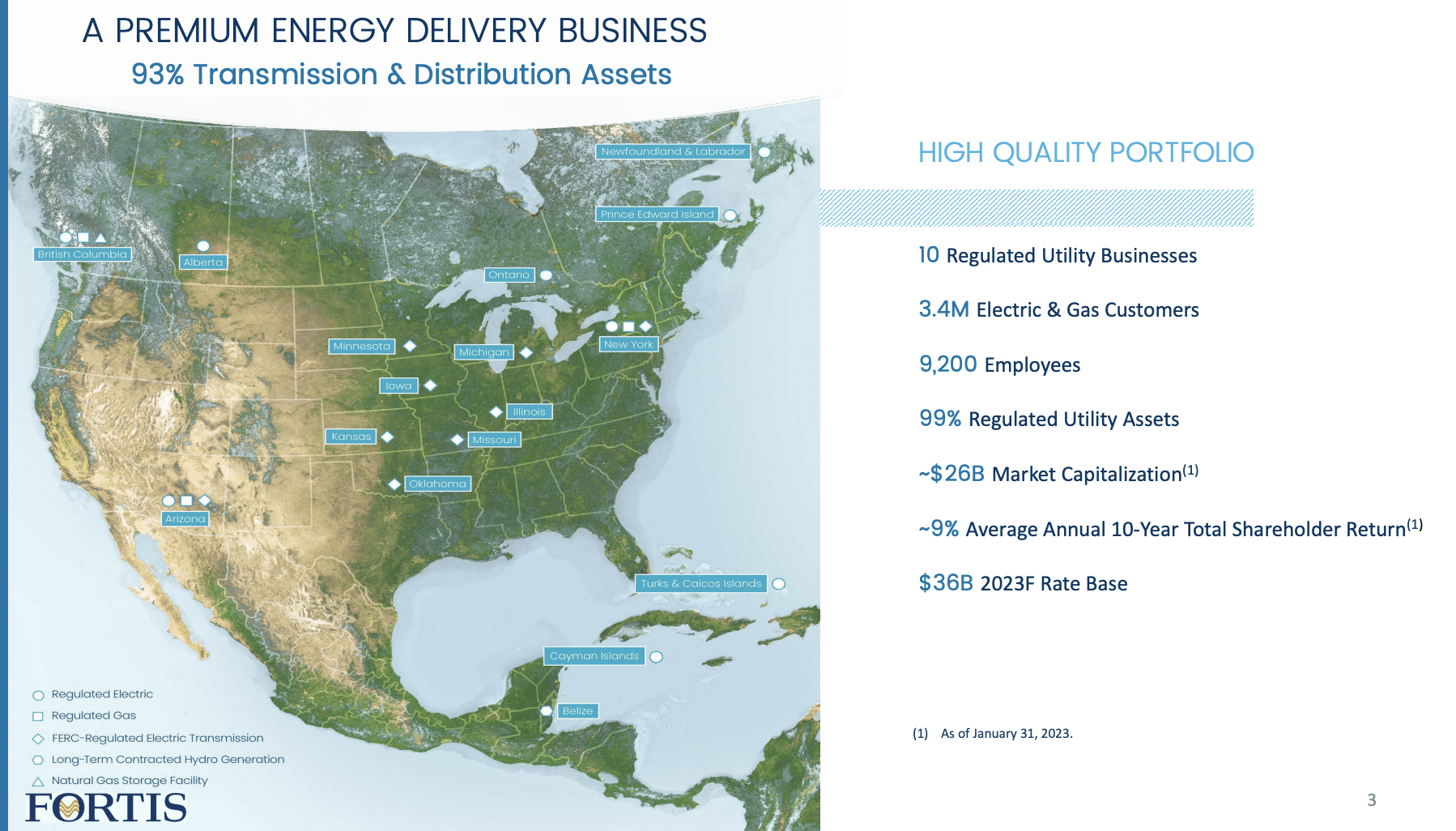

While I was aware of most Canadian stocks before writing this article, I did not have Fortis on my radar. Located in St. John’s, Newfoundland, Fortis is a Canadian utility company that provides electricity and natural gas services to customers in Canada, the United States, and the Caribbean. It operates through its subsidiaries, including electric utilities, gas distribution companies, and non-regulated energy businesses. With a history dating back over a century, Fortis has established itself as a leader in the energy industry, serving over three million customers and delivering reliable and affordable energy solutions. The company is committed to investing in sustainable infrastructure and promoting energy efficiency, making it a valuable player in the transition to a low-carbon future.

Fortis Inc.

Additionally, Fortis has a strong track record of financial stability and consistent dividend growth, making it an attractive option for income-seeking investors.

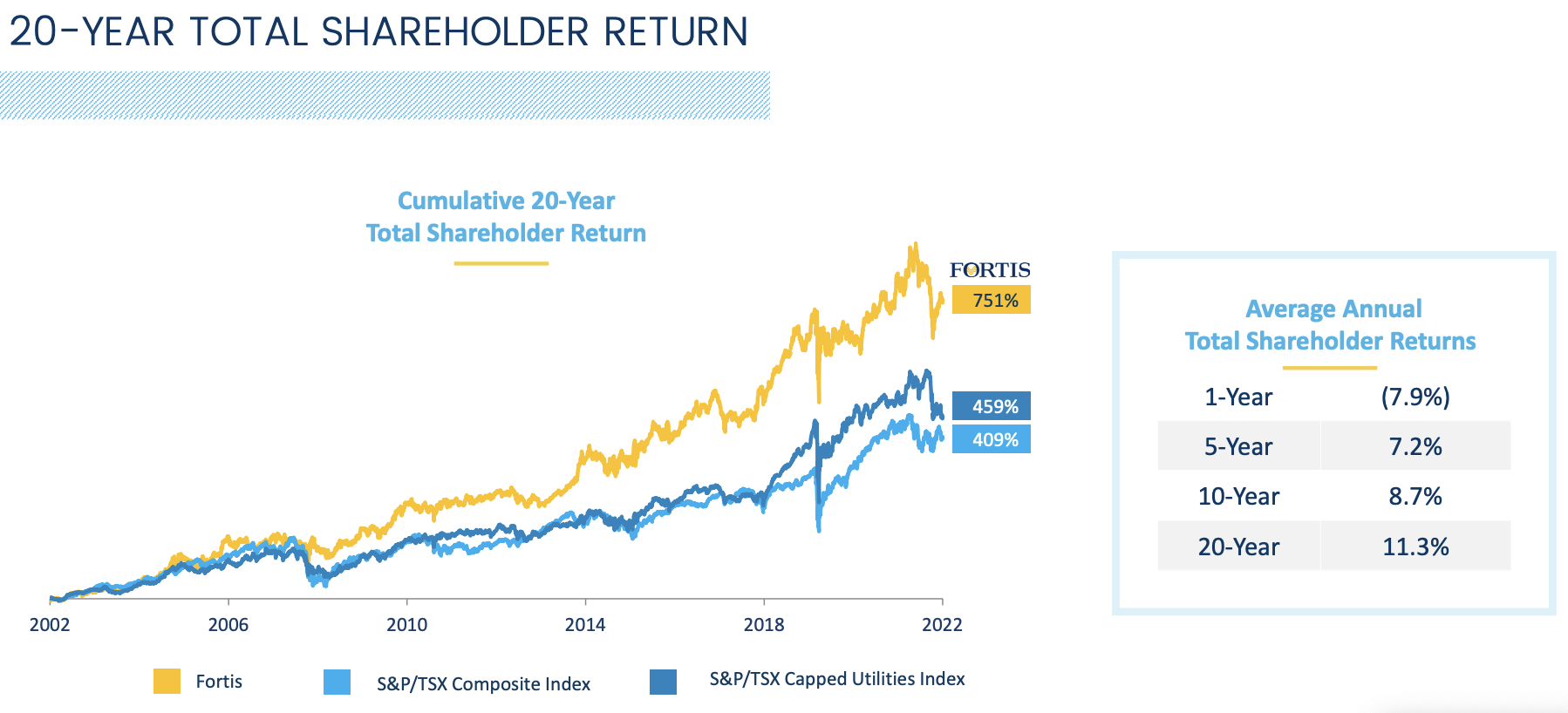

Over the past ten years, the company has returned 8.7% per year. Over the past 20 years, that number is 11.3%, beating the S&P/TSX composite and utilities index.

Fortis Inc.

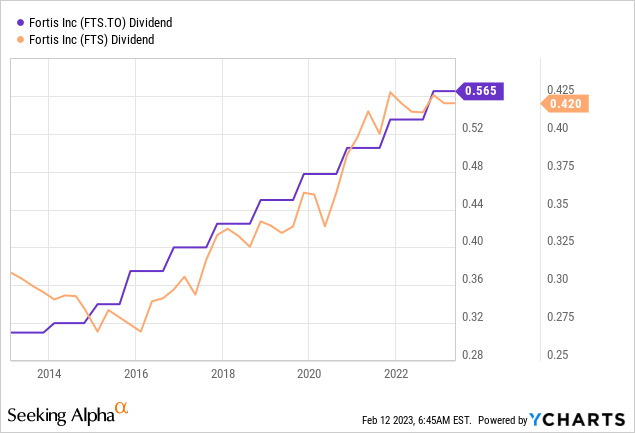

The company has hiked its dividend for 49 consecutive years, making it a dividend king after the next hike.

The company currently yields 4.1%, which is a more than decent yield.

These are the latest dividend growth rates:

- 10Y CAGR: 3.5%

- 5Y CAGR: 6.0%

- 3Y CAGR: 6.8%

The company is guiding to 4% to 6% in annual dividend growth through 2027.

[…] we increased our dividends paid per common share to $2.17 in 2022, up approximately 6% from 2021, marking 49 consecutive years of dividend increases. Looking ahead, we remain committed to building on our track record through the execution of our organic growth strategy that supports our 4% to 6% (PH) dividend growth guidance through 2027. – Fortis

The company has a BBB-rated balance sheet by Moody’s. S&P Global and Morningstar give the company an A- and A (low) rating, respectively. Last year, the company was able to raise C$3 billion in debt at an average rate of 3.9% with durations between 5-30 years.

The company has roughly $1.9 billion in debt due this year. The first major tranche of maturities will hit in 2026 when close to $2.5 billion in debt is due.

Takeaway

In this article, I highlighted three of my favorite Canadian stocks, showcasing their potential for income-seeking investors. Canada boasts a plethora of companies that provide high dividend yields, consistent dividend growth, strong balance sheets, and stable business models.

For energy-focused investors, Enbridge is a solid option to consider. Despite my focus on dividend growth over high yields, I believe that Enbridge aligns well with my investment strategy and I have placed the company on my watchlist.

Canadian National is another company worth considering, although I personally do not plan to invest in it as I already own three railroads.

For conservative investors seeking high yields in less cyclical industries, Fortis may be a good fit. The company offers a competitive yield compared to its American peers and boasts a strong growth profile for consistent dividend growth.

I’d love to hear your thoughts on this article. Are you interested in seeing more country-specific stock picks? Do you have a preference for Canadian exposure in your portfolio? Let us know in the comments.

Be the first to comment