piranka

Published on the Value Lab 1/15/22

Cambium Networks (NASDAQ:CMBM) is a network infrastructure services and products provider that builds solutions mainly for ISPs, but also enterprises and governments, in order to establish their networks according to their needs. The ISPs they focus on are in the American mid-market, and therefore while 5G is an important tailwind for them, it only comes into effect now that a large portion of the US population is beginning to get covered by 5G connectivity. They are going to see further tailwinds, and with a strong performance already from enterprise, Cambium is a solid business. However, it comes at too steep a price.

What Does Cambium Do?

Cambium provides point to multipoint solutions, but also point to point solutions, that connect what are often telco infrastructures that reach devices wirelessly to the internet backbone, and defines the functionality of the infrastructure and how it reaches out to devices wirelessly. The connectivity back to the backbone, which also uses spectrum, is called backhaul. Their clients are primarily ISPs who need their solutions for their infrastructure, like small intracity radio towers, to work properly. Cambium competes on being able to provide the best solutions in terms of connectivity at the lowest possible cost of ownership. They also have an enterprise solution which includes services for Wi-Fi solutions, switching and software subscriptions associated with a connectivity suite for enterprises. Things like video surveillance connectivity and other network management tools and software end up in the enterprise bucket too. They also sell to the government and for defense purposes, and those solutions are primarily point to point solutions.

Q3 Notes

Defense orders were the largest they’d ever been recently, and enterprise performed supremely well and grew in the mix, expanding gross margins.

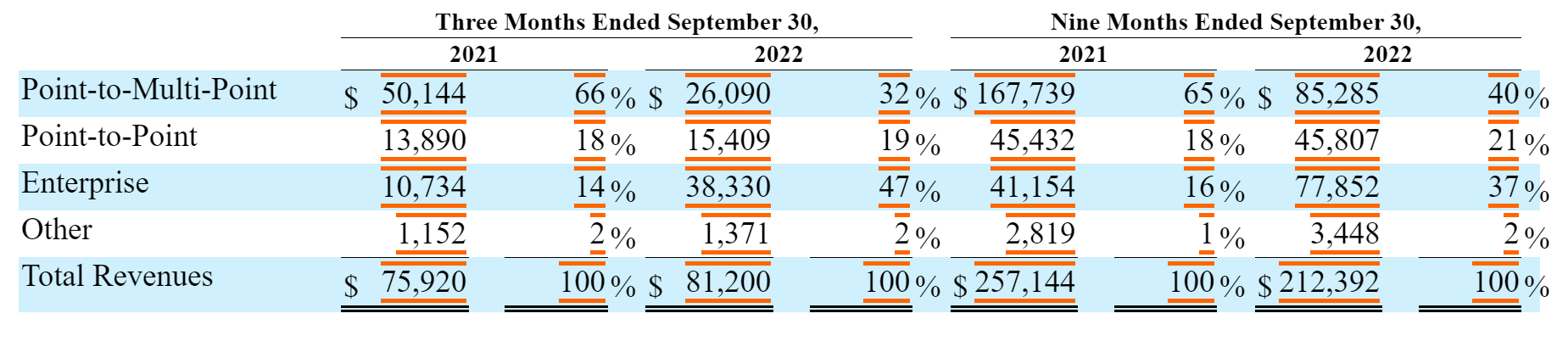

Segments (SEC.gov)

Their segments are as shown above. PTP is supported by defense demand, and PMP is in a pretty substantial decline YoY, shrinking almost 50%. Enterprise is rocketing by almost 4x YoY.

The dynamics are essentially a fall-off in investment in 4G-appropriate legacy products within PMP, with no pickup yet from the suite of 5G products that Cambium does have on offer. Therefore, PMP as a category is falling precipitously as mid-tier markets have yet to invest in 5G, but management expects this will start very soon, probably in the next quarter.

Enterprise is less complex systems provided to enterprises such as Wi-Fi switching and routing. The 4xing of this revenue did quite a lot to grow gross margins 3.5% up to 51.3% thanks to mix effects.

While growth from next-generation PMP products will help keep revenue momentum, which was up 7% this quarter YoY, gross margins will probably suffer. Not only are PMP products lower margin, but they are new and therefore will be limited in their scale and learning economies to start. However, long-term targets around 52% are believed to still be obtainable by management, especially as price action to raise product prices by about 5% is underway.

Bottom Line

Because of the need for substantially more telco infrastructure to provide 5G compared to 4G due to the shorter wavelengths, there is quite a lot of scope for growth of demand in the mid-market, which has only started to make a meaningful investment. Moreover, EMEA is a major market for Cambium, and one that is much earlier on in their general transition into 5G, accounting for more than a third of revenue. The 26x PE multiple is consistent with the quantum of growth that can be expected in its segments of the market. On the other hand, the multiple offers quite a little yield even at the terminus of where growth goes. It will need 3 years of high levels of compounded growth to bring the multiple at today’s price to be a compelling multiple. While markets are rallying, we think there are better opportunities. With conflict over the coming debt ceiling, and a risk of technical default by the US government on bonds in the event a new ceiling doesn’t get approved, funds that support investment in more suburban telco infrastructure may decline, as this is a somewhat subsidized market. You’d want a lower multiple, but not so much lower, to pull the trigger here. A 15% larger margin of safety would make it attractive.

Be the first to comment