Pgiam/iStock via Getty Images

The primary focus of this article is Calix, Inc. (NYSE:CALX).

Investment Theme

Actions of institutional investment organizations in managing their multi-billion-dollar stock portfolios require the negotiating help, and often temporary liquid capital assist, of Market-Makers [MMs] in the prompt, low-disturbance round-up of desired shares of identified promising companies.

MM risk-avoidance requirements continually drive derivative market prices, revealing in the limited-life legal contracts traded there the price-range extremes regarded likely by the well-informed sellers and buyers of the related risk protections. They are informed by over 100,000 world-wide wide-eyed and –eared MM employees on a 24x7x365 watch for change in competitive circumstances, which get immediately communicated to the home-based trading desks.

Following an unchanging risk-minimizing portfolio management discipline, records can be kept of how insightful the maintained intelligences flow has been on each of thousands of subject stocks over decades of daily observations.

Description of our company of interest

“Calix, Inc., together with its subsidiaries, provides cloud and software platforms, and systems and services in the United States, rest of Americas, Europe, the Middle East, Africa, and the Asia Pacific. The company’s cloud and software platforms, and systems and services enable broadband service providers (BSPs) to provide a range of services to anticipate and target new revenue-generating services and applications through mobile application. It offers its products through its direct sales force and resellers. Calix, Inc. was incorporated in 1999 and is headquartered in San Jose, California.”

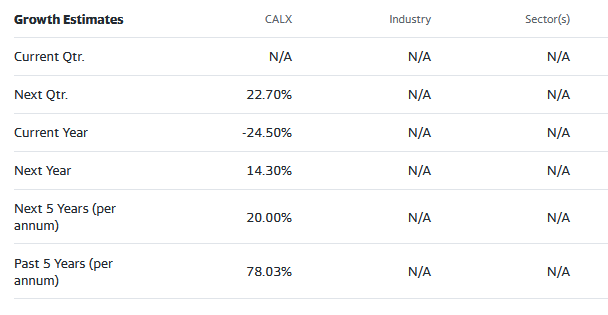

Source: Yahoo Finance

Yahoo Finance

These estimates come from less-intense general “street analyst” estimates made across hundreds or more subject companies, usually without specific things of value resting on the estimates offered.

What Are the Present Opportunities?

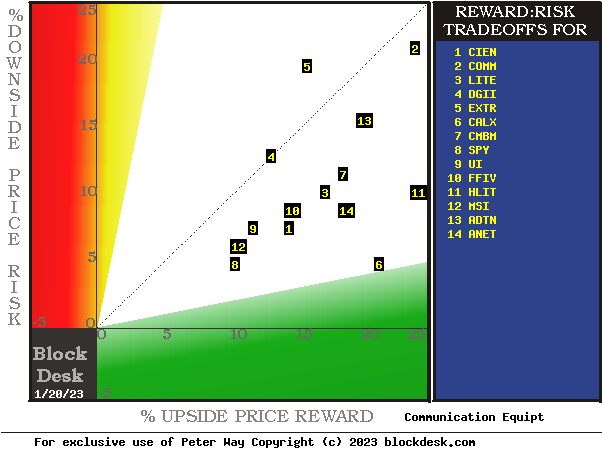

Figure 1 compares the prices and price-range extremes likely of Information Technology-provider stocks at this point in time, now that the Covid-19 pandemic has become relaxed as to voluntary home quarantining.

Figure 1

blockdesk.com

(used with permission)

The tradeoffs here are between near-term upside price gains (green horizontal scale) seen worth protecting against by Market-makers with short positions in each of the ETFs, and the prior actual price draw-downs experienced during holdings of those ETFs (red vertical scale). Both scales are of percent change from zero to 25%. Desirable locations are down and to the right.

The intersection of those coordinates by the numbered positions are identified by the stock symbols in the blue field to the right. The ‘market-average” notion SPDR S&P 500 Index ETF (SPY) at location [8] provides a sense of trade-off norms. CALX at [6] is our principal focus.

The dotted diagonal line marks the points of equal upside price change forecasts derived from Market-Maker [MM] hedging actions, and the actual worst-case price drawdowns from positions that could have been taken following prior MM forecasts like today’s.

This map is a good starting point, but it may only cover part of the investment characteristics that often should influence an investor’s choice of where to put his/her capital to work. Other considerations are indicated in Figure 2.

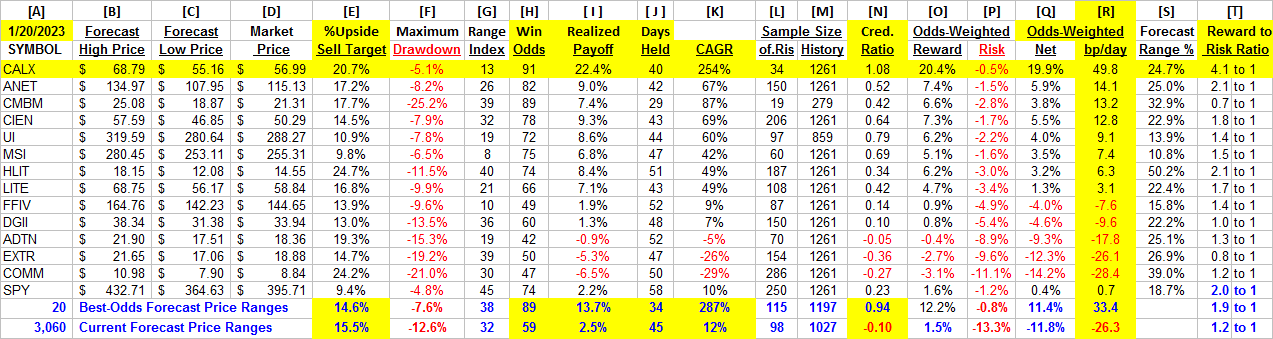

Figure 2

blockdesk.com

The likely price range forecast for our subject of the moment, CALX, is in columns [B] and [C] with its current price in [D]. [E] tells the upside size of a price move [B] from [D]. The Range Index [G] measures the downside proportion of the whole [C] to [B] range lying between [D] and [C]. That proportion is reported in [G] as a % may be looked at as a potential forecast-risk “cost” of owning or being “long” the subject.

We use the Range Index as a perceived Reward~Risk gauge of coming near price extremes to assemble a sample of prior expectations among institutional investors and their professional agents, the Market-Makers. With a statistically-significant number of prior expectations a comparison of the subject investment candidate of the moment can be made to itself, historically, and used as a normalized projection of how often such prior projections became profitable outcomes in the sample [L] from the available 1261 forecast days [M] of the past 5 years.

In addition to the “Win odds” of [H] we can know the average size [ I ] of the net win and loss payoff outcomes of all [L] forecasts and use it in comparison to the comparison of the current [E] upside potential maximum likely price gain prospect [E]. That [E] vs. [ I ] ratio we regard as the “Credible ratio” shown in [N]. Because [ I ] usually includes some loss experiences [N] typically is less than 1.0, but anything less than .66 is not encouraging.

A more universal “figure of merit” [fom] is obtained by win~loss odds weighting of [ I ] and [F] in [O] and [P] to get a net risk-adjusted reward [Q]. Recognizing the power of time in compounding, [Q] is adjusted by [J] to get the fom [R]. It is the potential “basis points per day” of return on investment from the current forecast.

Here that number for CALX is 49.8, which calculates to a CAGR of +254%. Compared to the current MM community expectations for the S&P 500 index ETF (SPY) at +0.7 of +10% CAGR that is pretty good. And compared to the 3,060+forecast population outlook for less than 1 bp/day it is way above average.

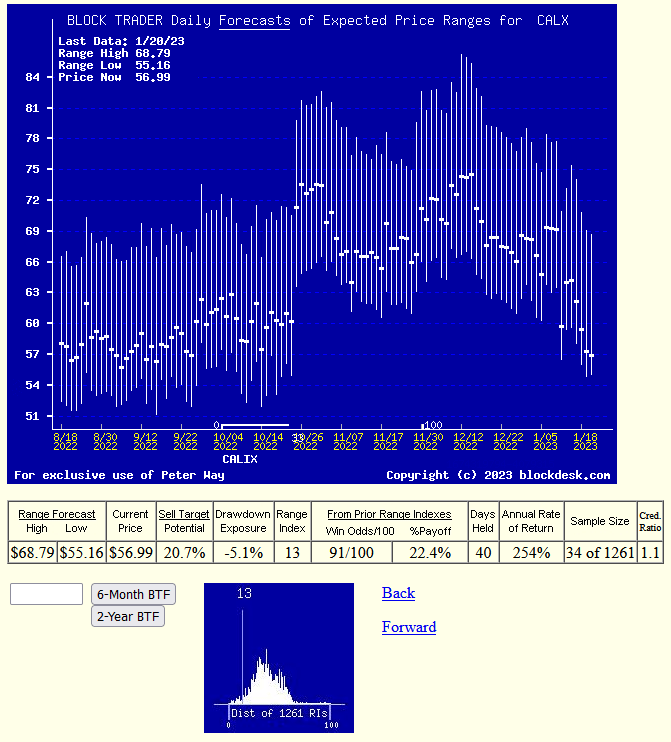

Recent trend of MM Price Range forecasts for CALX

Figure 3 provides picture and analysis data of the past 6 months trend of MM daily price range forecasts. The vertical lines are forecasts, NOT “technical analysis” of past market actions. Each day’s range forecast is split into upside and downside prospects from the close price of the day of the forecast. This has not been an encouraging period for CALX and its industry group.

Figure 3

blockdesk.com

(used with permission)

But now the CALX Range Index of 13, with a Reward-to-Risk ratio of 4.1 to 1 is very attractive compared to anything else in Figure 2’s column T. And its prior 5 year experience of 31 profitable position forecasts out of 34, with a net profitability of all 34 at +22.4% in 40 market days suggests a better-than +200% CAGR

Conclusion

We believe that Calix, Inc., better than other cloud care stocks, will blossom well in the next 8+ weeks. Then earlier opportunity experiences will likely be revisited, rewarding a buy-here, sell-later decision.

Be the first to comment