VOLKOVA ANASTASIA/iStock via Getty Images

Introduction

We have been a little remiss in covering some of the Canadian OFS companies up to now. Part of the reason is they get so little coverage on this platform it’s sometimes hard to remember they are out there. A poor excuse as a lot of folks follow these companies. This one had slipped my mind until one of the members of the Daily Drilling Report asked for information on Canadian OFS companies, and I was moved to act. Calfrac Well Services, (OTCPK:CFWFF) is just such a company that might present an opportunity in the coming months.

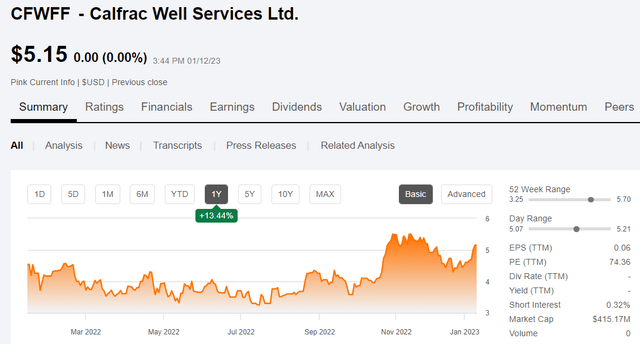

(Seeking Alpha)

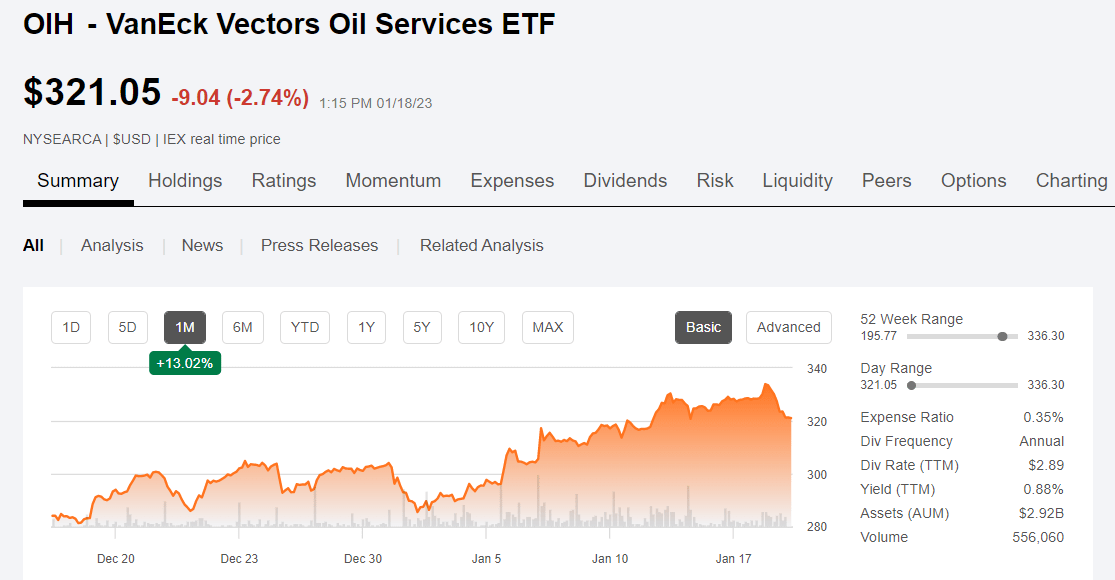

It’s had a 20% run recently, so we’re a little late to the game. This is consistent with the action of OFS tracking ETFs, such as the VanEck Vectors Oil Services ETF, (OIH). We think the general market is realizing that capex is returning to this sector, along with pricing power for their services, making these moves sustainable.

VanEck OFS-ETF (OIH) (Seeking Alpha)

Let’s have a closer look and see what the future might hold for them. Calfrac will report in early February, if history is any guide. The questions before us are (1) is there a reason to invest at all, and (2) is there a reason to dive in before earnings. Some of their customers have reported downtime or underlift for the fourth quarter, so it’s a fair assumption that service revenues will be off a hair as well. That potential was actually noted in the Q-3 call.

That might push us toward a seagull-like posture and sit on the fence until after earnings, but let’s look at the info and you can decide for yourselves.

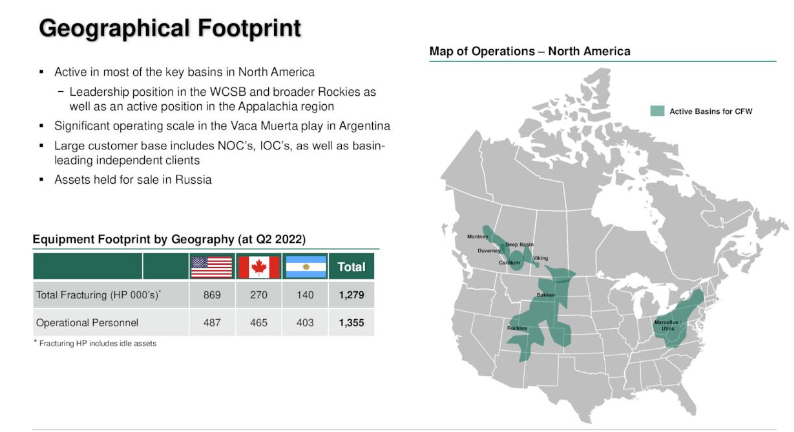

Calfrac’s footprint

The company is a minor player in the U.S. market with about two thirds of its available horsepower in the Bakken, Niobrara (Colorado), and the Marcellus. Most of the rest is in Canadian frac country and for some strange reason at least one spread down in Argentina in the Vaca Muerta play. They do note that margins in Argentina are approaching those in the U.S. Still!

They’re looking at solid business going forward in 2023, and the Baker Hughes rig count supports that notion with rig counts across relevant petroleum basins in Canada and the U.S. at high levels. As of Q-3 Calfrac had reactivated a 10th U.S. fleet, and runs four in Canada for a current company total of 15. In addition to fracking, the company provides coiled tubing and cementing services. As I’ve discussed previously, these businesses are complementary and promote higher EBITDA per job. In fact they go together so well, you will be hard pressed to find a fracking company not providing these ancillary services.

Calfrac

Calfrac has an additional 4-5 spreads that could be called up if business conditions warrant. This is a good possibility as after plateauing in the 280’s for most of 2022, in Q-4, the frac spread count touched 300 before winter set in. If we do pick up another 70-80 rigs this year as some drillers have suggested we might, additional fracking equipment will be needed.

Calfrac is the leader in the Canadian market and has a strong position in the two core Niobrara and Bakken plays.

The thesis for Calfrac

The company’s geographical footprint contributes to higher revenue and EBITDA as a percentage of revenue. In particular their strength in Canada is bullish for the company. As we have discussed many times, with shale reservoirs, there’s no production without fracking. To a degree production is driven by the number of wells, the length of the interval, and the amount of sand jammed into the fractures. Ergo, if the goal is to increase production you will drill and frack more, or you will not be successful. This underpins the thesis for Calfrac.

Calfrac

Pumping equipment is typically charged on a daily rate and hourly pumping charge basis. There also are incentives for pumping hazardous materials like acids or oxidizers and in some cases solvents. The hourly charge is the key driver of profits as it represents “up” time. Pumping companies don’t usually release this metric, but I take the number that Calfrac has included in the slide below 20-24 hours as a revenue driver, and bullish stat for the company.

Calfrac

A catalyst for Calfrac

As is noted on their Q-3 filing the company has as many as five fleets- +/- 270K HHP, available for reactivation. These are being upgraded to Tier IV DGB status as they are reactivated, which will promote higher rental rates. It does seem that Calfrac along with many other companies is being very methodical about this process. Patrick Powell, CEO, comments about the possibility of reactivation:

As a market leader, we expect to build upon the momentum through next year as customers pursue Calfrac to execute their completion schedules. We will continue to evaluate equipment expansion options and we’ll activate additional fleets if and when it makes sense for Calfrac.

The company is blessed with a pricing structure and revenue stream that permits upgrading stacked equipment to Tier IV DGB status. It only makes sense to invest the ~$4.5 mm per spread necessary to do this as business demands dictate.

Fracking equipment is in tight supply, and having Tier II pumps available for upgrade is bullish for the stock over the course of the year.

Additionally, pumping companies have told us they intend to pursue additional rate increases as more rigs hit the market. More rigs mean more holes in the ground needing to be fracked. This is bullish for the stock. Calfrac’s CEO Patrick Powell commented on the expectations for continuing to be able to push pricing as new equipment is reactivated:

By investing in projects with the highest expected yield, we will safely exceed our customer’s expectations and continue to generate increased financial performance to produce sustainable returns for our shareholders

Q-3, 2022

Calfrac’s revenue from continuing operations during the third quarter of 2022 was $438.3 million, or 67% higher than the same period in 2021. Adjusted EBITDA increased to $91.3 million during the third quarter of 2022 from $29.8 million in the comparable quarter in 2021, which resulted in a corresponding $52.4 million year-over-year increase in net income from continuing operations. This significant improvement in financial performance was primarily due to more consistent utilization for the company’s 13 fracturing fleets that were operating during the quarter in North America, as well as an boost in pricing to address the significant input cost inflation that was experienced over the past few quarters.

Changes in working capital of $57.9 million during the third quarter versus 40.3 million in the comparative quarter in 2021. This change was largely driven by the significant quarter-over-quarter increase in revenue. Calfrac spent a total of 24.7 million on capital expenditures from continuing operations in the third quarter compared to 24.1 million in the same period of 2021. These expenditures were primarily related to maintenance and sustaining capital to support the company’s fracturing operations, as well as $4.5 million of reactivation costs related to Calfrac’s US division.

During the third quarter of 2022, cash proceeds of 0.6 million were received from the exercise of warrants and stock options. Subsequent to the end of the third quarter, 8.6 million of Calfrac’s 1.5 lien notes were converted into common shares. Following this conversion, the remaining principle amount outstanding was 47.4 million, a decrease of 12.6 million from the original issuance amount of 60 million.

To summarize the balance sheet, at the end of the third quarter, the company had working capital of $208 million from continuing operations, including $11.9 million in cash. Calfrac amended and restated its credit agreement, which included an extension of the maturity date to July 1, 2024. At September 30, 2022, the company had used $1 million of its credit facilities for letters of credit and had 200 million of borrowings under its credit facilities, leaving $49 million in available borrowing capacity at the end of the third quarter.

Risks

Revenue, EBITDA, and utilization of the equipment tripled in 2022 from 2021. The higher oil prices seen over the course of the year were a determining factor in this improvement. Any long-term decrease in oil prices will chip away at the structural story for these gains and could result in a drop in share prices.

Your takeaway

Calfrac is trading at attractive multiples EV/EBITDA 2.9X on a run rate forward basis, even with the 15% bump in shares over the last month. That puts Calfrac in the same neighborhood as Liberty Energy (LBRT) trading at 2.66X, although comparisons between the two companies stop there.

Analysts are high on Calfrac with the current recommendation being overweight. Price estimates range from $8.00 to $14.50, with the average being $11.33 per share. (It should be noted these ratings are for the Toronto, Canada exchange-TSX as the OTC listing doesn’t get analyst coverage.)

Pumping companies in that first tier of OFS companies that will benefit from growing activity across the shale plays in 2023. I hate to bore you, but if you want production out of shale, you have to crack some rock. As such, I think the company represents a good bet for investors at or near present prices.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment