Vertigo3d

Overview

C3.ai (NYSE:AI) is an enterprise software company focused on proving artificial intelligence enabled application products. The core of their offering is an ‘enterprise AI development platform’. In essence, this is a set of services (snippets of code that do a particular, focused, task) that allows developers to readily integrate AI capabilities into their programs.

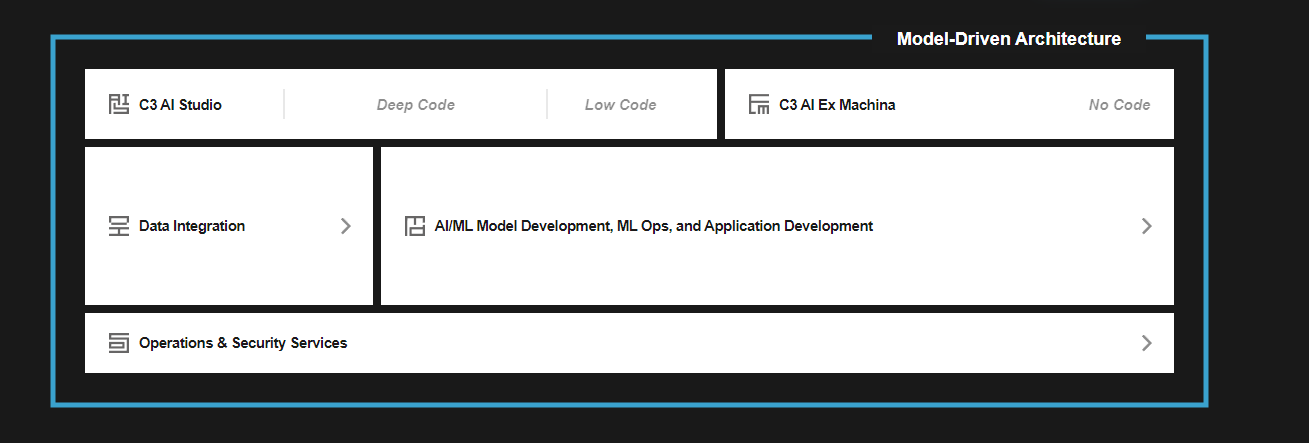

Looking into their product further, we see that this includes ‘deep code’ as well as ‘low code’ components. By deep code they are referring to full-on software services connecting into popular development environments such as Visual Studio Code as well as Python’s Jupyter Notebook (data processing tool). The low code side of the offering provides a primarily visual interface allowing for the construction of AI workflows, which primarily involve processing data and setting up models. In addition, they provide the capacity for data integration tooling for working across a range of disparate data sets – something that is quite common in the context of machine learning and AI.

c3.ai 2.8.23

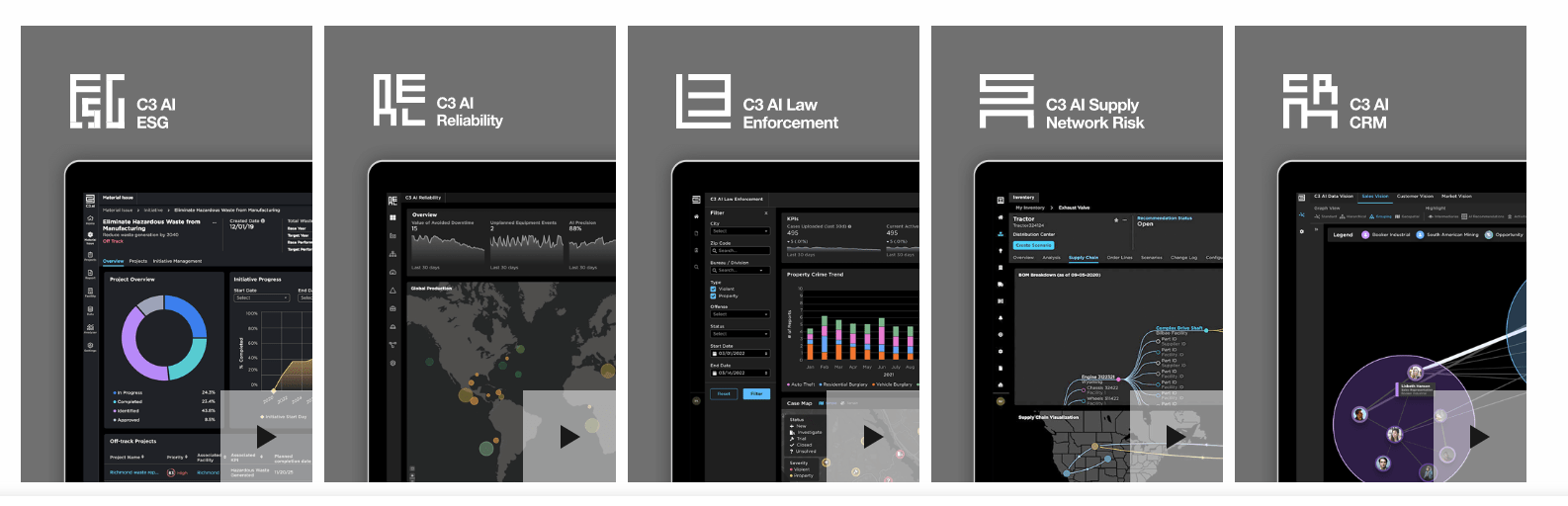

Along with code-level components, C3.ai also provides tailored applications for common use cases. This includes things such as reliability engineering (ensuring uptime of critical computing systems), networking, and customer relationship management (managing data around customer base).

c3.ai 2.8.23

C3.ai first entered the public markets in Q4 2020, conducting an initial public offering at $42 per share. Notably, the company had a private placement commitment from Microsoft (MSFT) at the time of its IPO for just over a million shares; since this was contingent on a successful offering, it’s safe to assume Microsoft vested the shares. It is unclear at present whether they are still holding on to them, however. Nonetheless, we can take this as a vote of confidence in C3 from a marquee technology player.

sec.gov c3.ai 2.8.23

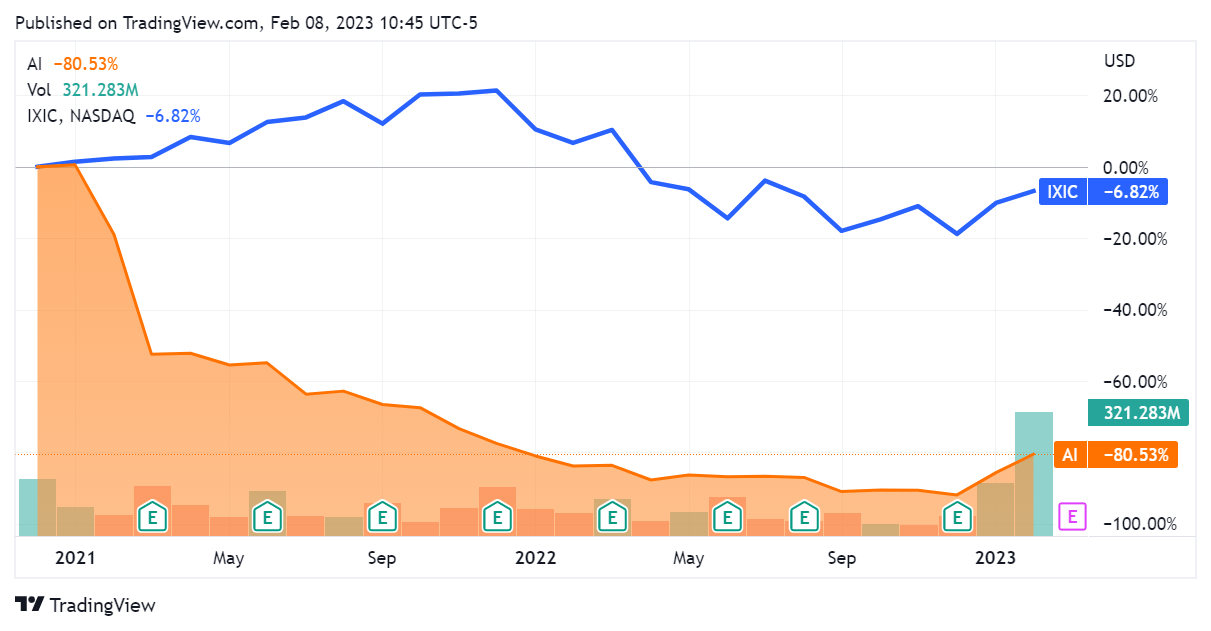

Subsequent to its IPO at $42 per share, C3.ai has depreciated significantly and underperformed the NASDAQ composite significantly.

Seeking Alpha AI 2.8.23

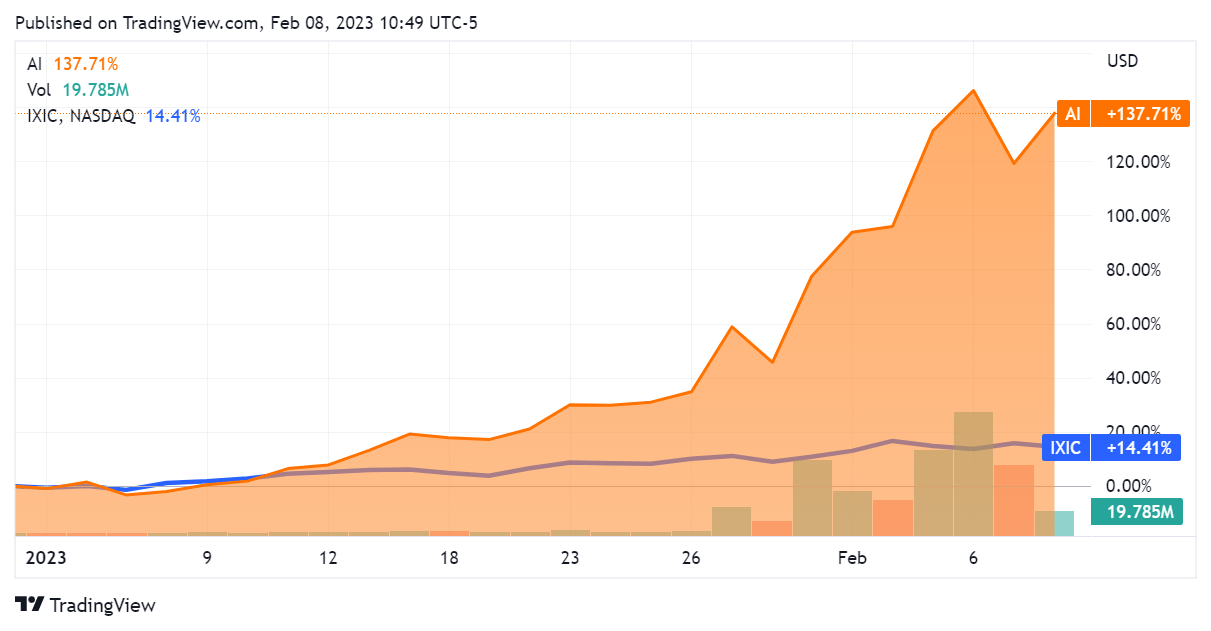

2023 has a reversal of this trend, with C3.ai now outperforming the NASDAQ by quite a bit – in line with the ongoing buzz around ‘AI stocks’. Nonetheless, the security continues to trade at a material discount ($26.71 as of this article) to its IPO price.

Seeking Alpha AI 2.8.23

This article will review the financials of in order to see if this recent appreciation is warranted as well as quality of the underlying business.

Financials

C3.ai is a relatively recent IPO and most certainly what we can consider a growth stock. Looking over at its revenues, we see it has been able to post double-digit YoY growth over the last couple of years. Yet, the quarter-to-quarter performance is far from ideal, with downward quarter-over-quarter occurring relatively consistently over this timeframe. It is a point of concern that the company achieved record revenues in Q1 2022 but has since posted 2 quarters below that number, with the recent figure again coming in lower than the previous one. This is generally not something that I like to see in the context of growing technology entities, as it may imply a smaller total addressable market or a weaker product than may have been previously expected. Year-over-year growth aside, these numbers are certainly a mixed bag in my view.

Seeking Alpha AI 2.8.23 Seeking Alpha AI 2.8.23

Looking at the firm’s operating picture, we see that the firm has actually been losing more money from operations than previously – with a concomitant increase in its operating expenses, which are now roughly double what they were at the time of its IPO. It is worth noting that a significant portion of this operating expense growth is being driven by R&D, which brings along certain tax efficiencies but also implies an ongoing investment in the product offering. That aside, the operating picture is overall inflecting towards the negative.

Seeking Alpha AI 2.8.23 Seeking Alpha AI 2.8.23

This operating performance unfortunately translates into an ongoing loss as to the bottom line. Posting only one marginally profitable quarter over the last 10, the company’s increasingly-expensive operations have driven it to higher net losses. Q2 2022 saw the company post its largest net loss to date, with Q3 2022 coming in quite close to that number.

Seeking Alpha AI 2.8.23

Altogether this has fed into a severe and growing accumulated deficit as to retained earnings. Certainly this company isn’t going to have positive per-share fundamental value any time soon, with retained earnings coming in at negative $682M as per its latest filing. The trendline here is clear, and C3.ai hasn’t shown anything indicating that it is turning the corner to profitability as of just yet.

Seeking Alpha AI 2.8.23

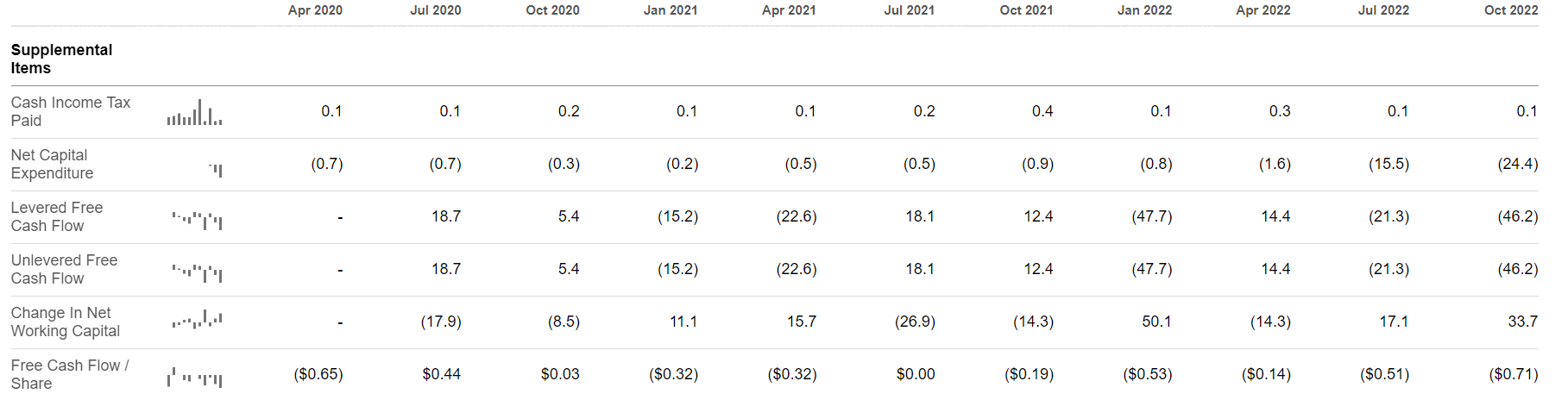

Rounding all of this out via the cash flow statement, we see a few bright spots. Namely, C3.ai has indeed had several quarters wherein it generated positive free cash flow, although this is certainly not the norm. Additionally, its debt service is minimal and shouldn’t burden the company should it begin to perform from an operating perspective. While the several positive FCF quarters give me a degree of confidence that the company can self-sustain and push towards profit through its own cash generation, it hasn’t maintained any semblance of consistency in this regard.

Seeking Alpha AI 2.8.23

Overall these financials indicate to me a company that is still finding its footing, and is perhaps having more difficulty doing so than may have been expected. Volatile revenues, growing losses, and a declining operating picture all serve to corroborate this.

Conclusion

C3.ai does not appear to be a good investment at this time. While there are a few bright spots, namely the small buy-in it received from Microsoft as well as a few positive cash flow quarters, the picture overall is too murky to say that it is headed in the right direction. In particular, I am concerned to see revenue declines in a company this early in its growth cycle. If C3.ai can’t scale its revenues, its poor operating performance will only act as that much more of a burden on its capacity to generate cash flow and net profits. The counterpoint to this is its ongoing, significant, R&D spend – something that may or may not change this trend. Since AI stock is already down significantly from its IPO price, I’ll call this a hold at best for now.

Be the first to comment