BlackJack3D

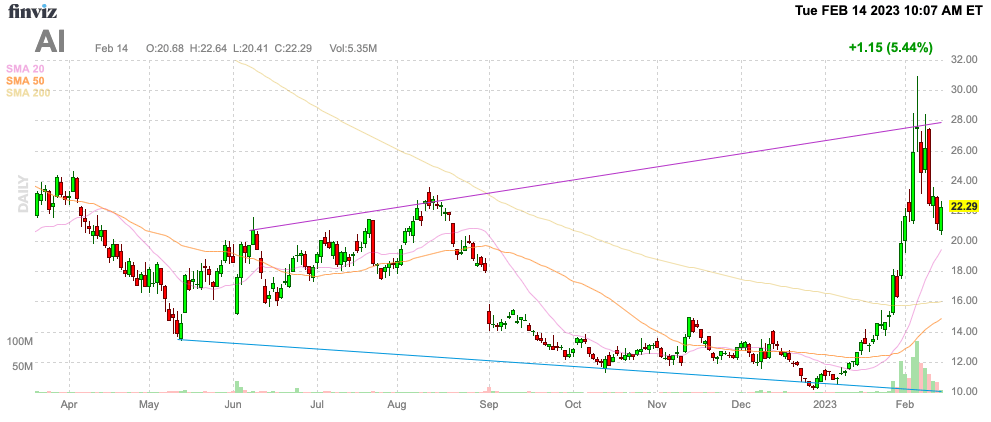

The stock of C3.ai (NYSE:AI) was dumped by wise investors on the recent rally from under $10 to over $30 in just over a month. The enterprise AI software company is cheaper than one thinks after the dip back to $20 following the end of the hype. My investment thesis remains very Bullish on the AI technology company, trading at a major discount due to the painful transition to a pay-as-you-go consumption model.

Finviz

Best Of Both Worlds

The AI chat hype sent every sock in the market with AI in their name substantially higher, regardless of whether the business prospects were improved. C3.ai actually announced a new suite of generative AI chat integrations, but SoundHound AI (SOUN) and BigBear.ai Holdings (BBAI) equally soared in the last couple of months.

C3.ai plans to integrate AI capabilities from Open AI, Google (GOOG, GOOGL) and academia into their new C3 Generative AI Product Suite. The company already announced the C3 Generative AI for Enterprise Search product for release in March 2023.

The good news for C3.ai is that the company is more of picks and shovels software developer of the generative AI chat competition ongoing with Google and the Open AI partnership with Microsoft (MSFT). C3.ai gets to license the best features of the AI chat technology from both tech giants while hopefully avoiding the errors inherent in both products currently.

Value Equation Adjustment

While the initial reaction is to think C3.ai is overpriced after a huge rally, but the stock likely didn’t belong down at $10. The enterprise AI software company is in the process of transitioning to a consumption-based revenue model.

As highlighted back in early December following the FQ2’23 earnings report, the revenue transition was slowing down reported revenue growth. C3.ai was already shifting to Phase 2 of the transition, with new consumption-based trends in early deal ramp.

The company is in the first few quarters of the transition where reported revenues are below the levels under the prior revenue model. The new generative AI search product could further boost AI consumption in the quarters ahead for FY24.

Analysts forecast FY24 revenues jumping to $317 million as the consumption model starts producing higher revenues towards the end of the year next April. Oddly, management guided to FY24 revenues of ~$340 million as the consumption model starts gaining steam, producing 30% growth. The disconnect between analysts and the company is around $23 million now.

The stock value has slumped back to only $2.4 billion, with the enterprise value dipping to just $1.5 billion. C3.ai ended October with a cash balance of $859 million, and the company burned ~$45 million per quarter from operations to start FY23 to grow the business and switch to a consumption model.

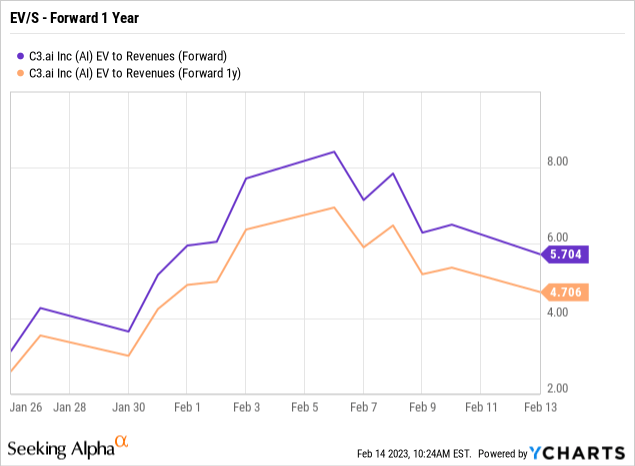

The forward EV/S multiple dips below 5x when using FY24 sales numbers. The stock did get pricey at the recent highs above $30, but C3.ai is now much closer to $20 where the valuation is much more reasonable.

The ironic part about the recent rally is that the stock presumably fell due to the lack of profits, but the company didn’t alter the profit picture and C3.ai tripled in months. Even more amazing, if the company hits the internal revenue targets of $340 million next fiscal year, the FY24 forward EV/S multiple dips to only 4.5x.

As previous research highlighted, the stock traded at only 8x EV/FY24 revenues of $340 million at the recent peak. The model even used an assumption that the cash balance falls to only $750 million due to ongoing cash burn rates.

Takeaway

The key investor takeaway is that C3.ai is far cheaper than the market thinks, due to the irrational value when the stock dipped to only $10. C3.ai tripled in a couple of months, but the valuation remains very appealing here around $20.

Investors looking to own the AI stock should buy a starter position here and look to acquire more shares on any return to the previous trading range starting at $15. After all, C3.ai isn’t forecast to even report growth in the next couple of quarters, likely leading to see dissatisfaction with holding the stock in the near term.

Be the first to comment