z1b

Over the past weeks, a lot of dividend stocks have sold off because of fears that inflation might be stickier and that interest rates could stay higher for longer.

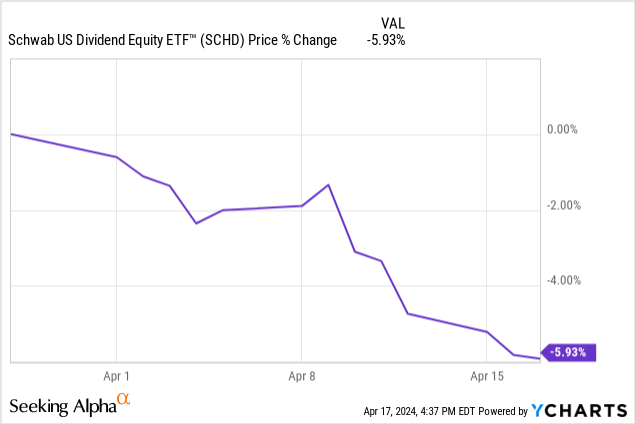

As a result, the popular dividend ETF, Schwab US Dividend Equity ETF (SCHD) dropped by 6% in the past weeks:

And that’s just the average of dividend-paying stocks.

Many smaller and lesser-known names dropped by closer to 15%, especially in higher yielding sectors of the market that are today out-of-favor. Good examples include financials, banks, asset managers, and REITs.

We think that this is a buying opportunity.

The headline CPI is not really “stickier”. It only seems so because of how the shelter component of the index is calculated. In the last month, they had shelter inflation at 5.7% and this is a huge deal given that shelter represents a massive 36.2% of the CPI.

But in reality, anyone who follows the housing market will know that real-time shelter inflation is far lower than that. The apartment sector is today oversupplied and most apartment REITs, including Mid-America (MAA) and Camden Property (CPT), have guided for stagnating or even slightly declining rents in 2024.

Therefore, real-time inflation is now quite a bit lower than the headline CPI. The way they calculated shelter CPI is lagging and it is keeping the headline figure higher than it should be.

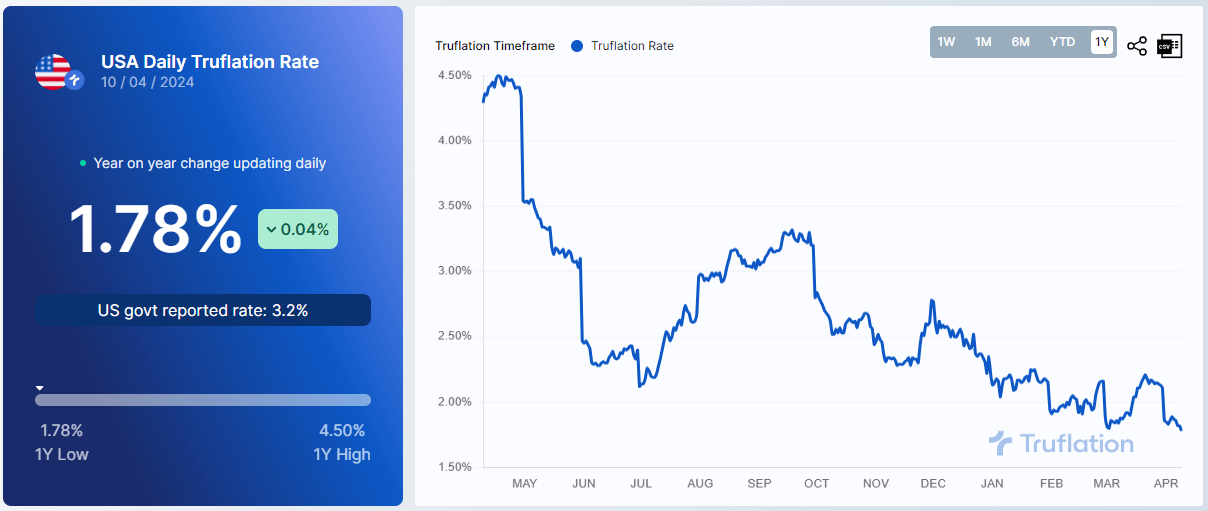

According to Truflation, the real-time CPI is today just 1.8% and it has been around the 2% mark for a while already:

Truflation

Truflation correctly predicted the surge in inflation ahead of the Fed, and I think that they are now correctly predicting its end as well.

This is the reason why interest rates are still likely to be cut in the future, even if it may take a bit more patience.

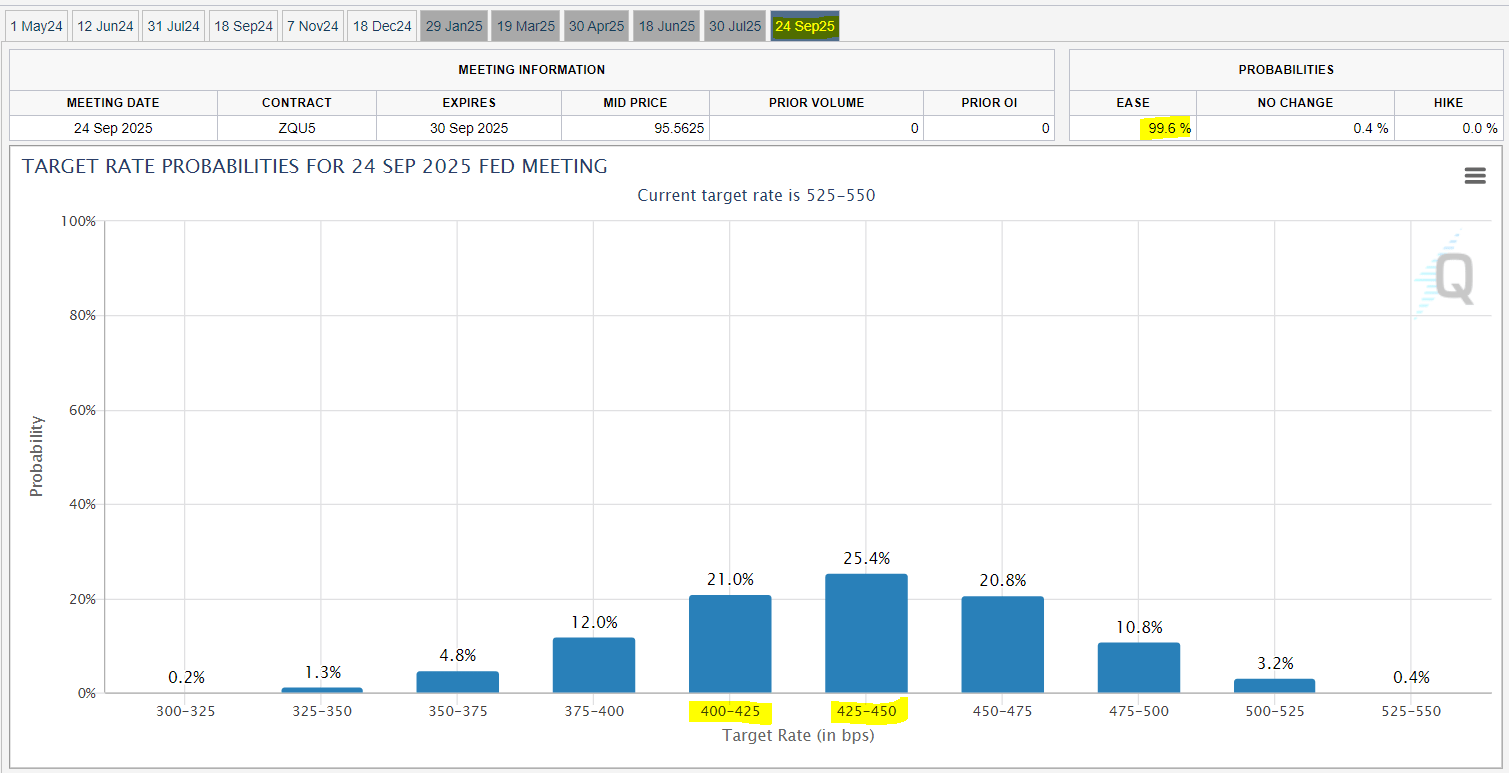

The Fedwatch tool is today predicting a 96% change of at least one cut within a year from now, and by September 2025, it appears likely that interest rates will be 100-150 basis points lower:

Fedwatch

This bodes very well for beaten-down dividend stocks that are discounted because of fears of a “higher for longer” environment.

In what follows, I will discuss two opportunities to buy the dip:

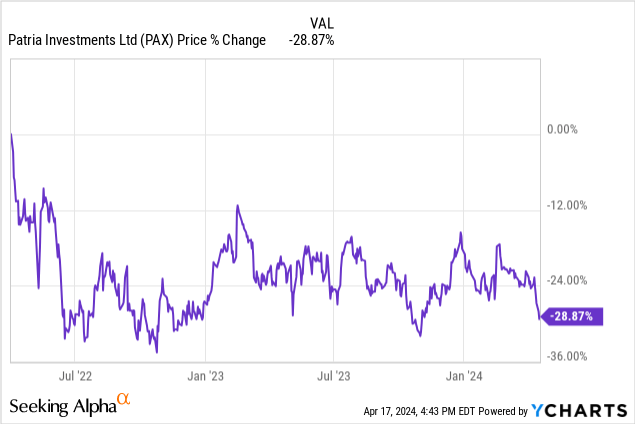

Patria Investments (PAX)

PAX is probably my single favorite “buy-the-dip” opportunity.

That’s because the company is doing very well and isn’t heavily impacted by the surge in interest rates. In fact, the company has very little debt, it is growing rapidly, and it has recently posted good news for shareholders.

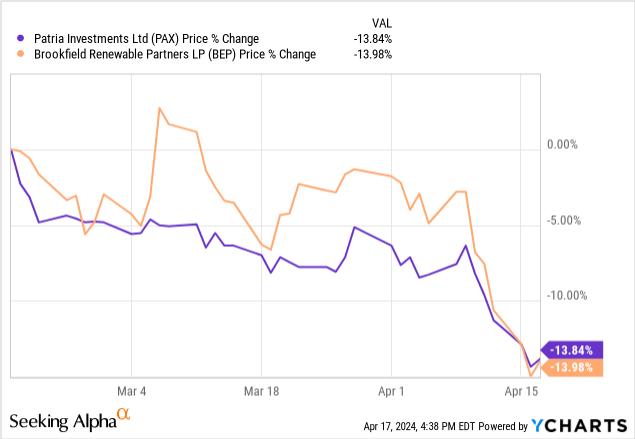

But despite that, its share price has dropped quite significantly from its recent highs:

I just cannot make sense of it so I am buying more of it.

PAX is an alternative asset manager just like Blackstone (BX), Brookfield (BN), KKR (KKR), and Blue Owl (OWL). They all earn fee income for managing investments for others, and they grow by raising additional capital.

They each have their unique focus.

Blackstone focuses mainly on private real estate investments. Brookfield is more focused on infrastructure. KKR owns mainly private companies. And Blue Owl specializes in private credit.

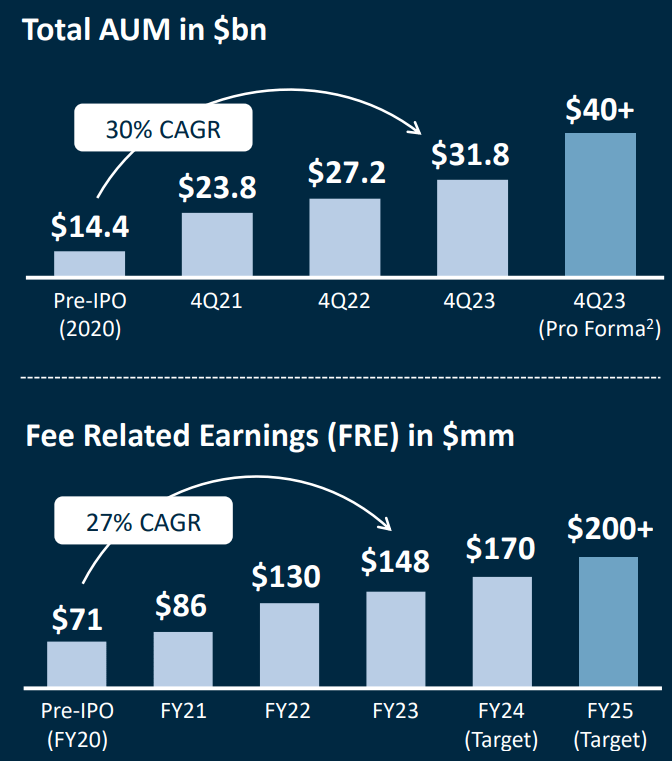

PAX is unique in that it focuses on Latin American markets. It is the leading private equity investment firm in the region, and it has been very successful at growing its assets under management and its fee income.

Patria Investments

I expect this strong growth to continue because Latin America is becoming increasingly attractive for investors due to several reasons:

- Geopolitical uncertainty: First of all, Latin America is today seen as a safe haven while there is war in Ukraine and in the Middle East and high risk of growing conflicts in Asia. Latin America was a safe haven during the second World War, and many perceive it that way today as well. It provides much needed diversification in a chaotic world.

- Nearshoring: Western companies are learning the hard way that dictatorships like Russia and China cannot be trusted, and they are now gradually reconfiguring their supply chains, often bringing back large portions of them closer to their end consumer. This benefits Central and Latin America, as a lot of US companies heavily invest there.

- Relatively low valuations: Finally, Latin American markets remain highly fragmented and less competitive and as a result, valuations are typically a lot lower and opportunities are abundant, especially for sophisticated private equity players like Patria.

This is a great environment for Patria, and it is well reflected in its most recent results. Its fee related earnings per share have now reached $1.25 annualized in Q4, which was up 31% year-over-year.

That prices the company at just ~8x its FRE if you remove the net accrued performance fees from its share price. This is far lower valuation than its close peers, and that’s despite growing at a faster pace and having little debt on its balance sheet.

The company also earns irregular performance fees, which result in somewhat bumpy dividend income. They have a variable policy, but we have good reasons to believe that its performance fee realizations will continue and its latest dividend annualized results in a near 12% dividend yield.

That’s extremely cheap for a high-quality asset manager with double-digit annual growth prospects.

I am buying the dips.

Brookfield Renewable Partners (BEP / BEPC)

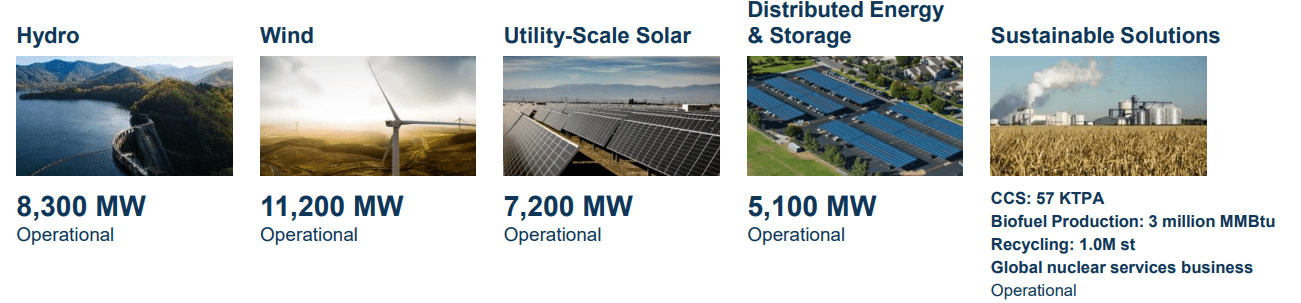

BEP is a massive renewable energy platform that’s operated by the private equity giant, Brookfield (BN).

It owns a vast portfolio of hydro, wind, solar, and other renewable assets throughout the world:

Brookfield Renewable Partners

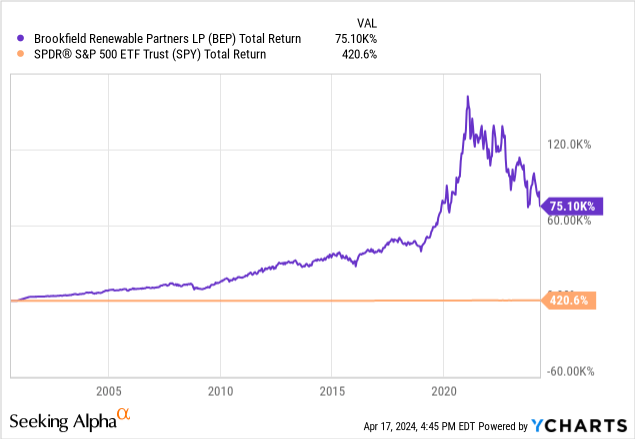

The company has an exceptional track record, having managed to grow its FFO per share by 12% annually, resulting in enormous returns when combined with its high dividend yield. It has massively outperformed the S&P500 (SPY) and most other stocks:

And we think that they can keep this going.

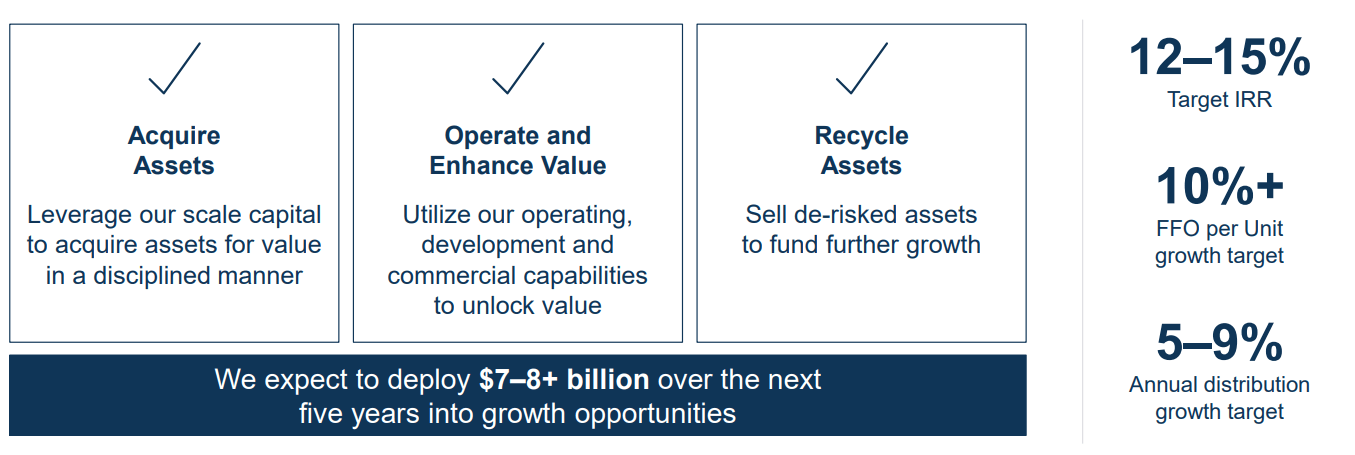

The company has a strong BBB+ rated balance sheet with fixed rate debt and long debt maturities at 12 years. Moreover, its revenue is contracted for 13 years on average and 70% of that is linked to inflation. Finally, they have a large development pipeline that should result in significant growth in the coming years.

Therefore, they are confident that they will be able to keep growing their FFO per share by 10%+ annually:

Brookfield Renewable Partners

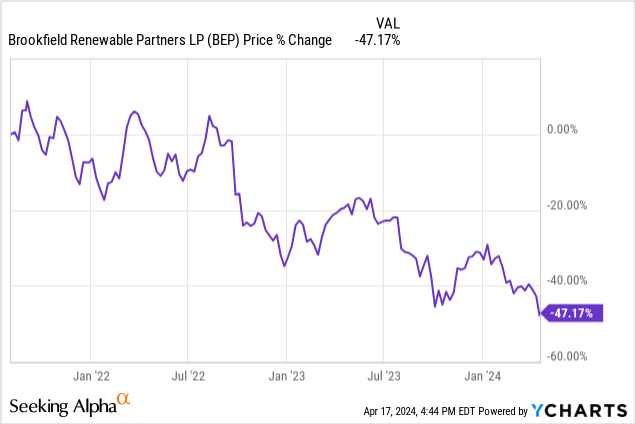

Even then, its stock price has crashed because of fears of rising interest rates. Year-to-date, it has dropped by ~50%:

As a result, it is now priced at one of its lowest valuations ever, trading at just 11x its AFFO compared to its 21x three-year average.

As a result, I believe that the stock today offers a strong margin of safety and significant upside potential as interest rates return to lower levels. And if they don’t, I would still expect BEP to do well over time given that it offers a 7% dividend yield and is expected to grow its cash flow by 10%+ annually.

Hard to beat that.

Closing Note

The recent dip has resulted in some exceptional buying opportunities among dividend stocks.

PAX and BEP are some of my favorites, but there are many more that we are buying today.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment