8vFanI

Chatham Lodging Trust (NYSE:CLDT) is restoring its dividend after the real estate investment trust suspended it at the start of Covid-19 in 2020.

In addition to the dividend being reinstated (albeit at a lower rate), Chatham Lodging is experiencing a fundamental turnaround in its operating metrics, such as RevPar and occupancy, as people begin to travel again.

Back in August last year, I wrote an article highlighting how Chatham Lodging Trust was ready for a rebound. Now, with the trust’s business on a clear path to normalization, I believe Chatham Lodging could provide generous dividend increases to shareholders in the future.

The stock’s book value valuation is not expensive, and if the business continues on its recovery path, Chatham Lodging may be able to close the gap between market price and book value.

The Dividend Is Back

Because of the impact Covid-19 had on the trust’s operating performance, Chatham Lodging suspended its dividend in 2020. The trust announced in December that it will resume paying a quarterly dividend of $0.07 per share, making Chatham Lodging an appealing dividend stock once again.

The trust used to pay $0.11 per share per month prior to Covid-19, so the dividend will not be reinstated anywhere near the old level. However, the reinstatement is significant for Chatham Lodging because it demonstrates that the trust’s operational and financial health is improving.

Improving Business Fundamentals

Occupancy rates and a metric known as RevPar are two of the most important portfolio metrics for lodging trusts.

RevPar is a hotel industry performance measure, as well as one used by lodging trusts, that shows how much money operators can charge customers per room per night.

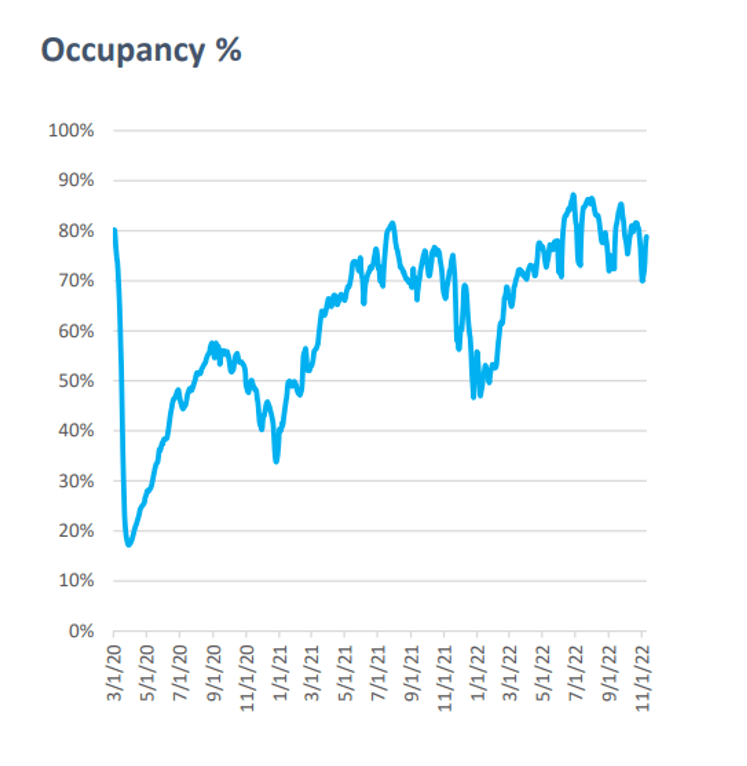

Both Chatham Lodging’s occupancy and RevPAR crashed at the start of Covid-19, and while the last three years have been extremely difficult for the trust, the recovery trend clearly points upwards. Chatham Trust’s same-portfolio occupancy was 80% in 3Q-22, and it has been gradually recovering since the occupancy rate briefly fell below 20% in 2020.

Occupancy Rates (Chatham Lodging Trust)

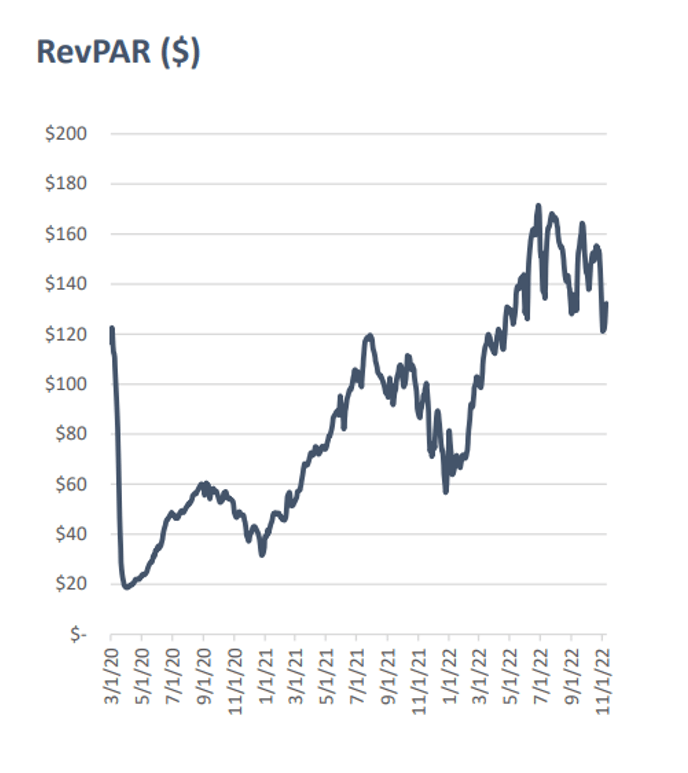

In terms of RevPAR, Chatham Lodging’s key metric continued to improve throughout 2022. Despite a recent drop in the RevPAR metric, the trust’s RevPAR was $150 in 3Q-22, compared to $149 in 3Q-19. In other words, Chatham Lodging’s RevPAR has fully recovered all of its 2020 Covid-related losses.

RevPAR (Chatham Lodging Trust)

AFFO Recovery And Pay-Out Ratio

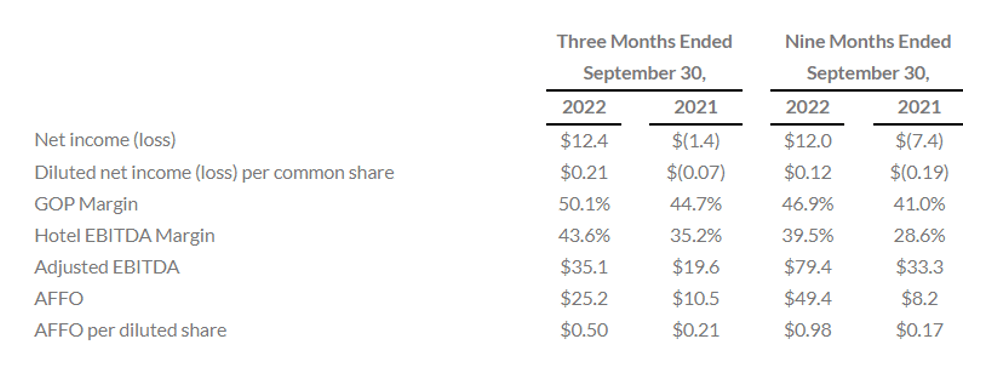

In 3Q-22, Chatham Lodging earned $0.50 per share in adjusted funds from operations, a 138% increase YoY. Returning travelers to the trust’s properties drove the recovery, which resulted in improvements in the two key metrics discussed above.

Chatham Lodging is playing it safe by paying out only 14% of its adjusted funds from operations through a quarterly dividend of $0.07 per share.

In the future, the trust could earn $2.00 per share in AFFO and easily double or triple its dividend payout without hitting coverage constraints.

AFFO (Chatham Lodging Trust)

Cheap Book Value Multiple

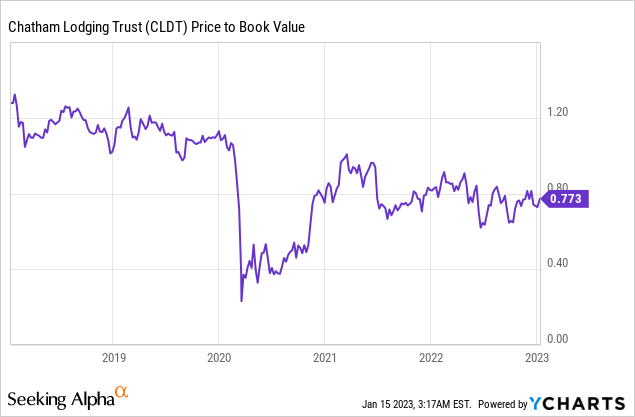

The stock of Chatham Lodging is trading at a compelling book value multiple of 0.77x, implying a 23% discount to book value. Because the trust’s stock is trading at a discount, passive income investors can acquire a high-quality portfolio of branded hotel properties at an attractive price.

Considering the significant recovery in key operating metrics RevPAR and occupancy, I believe there is no real reason for CLDT to continue trading at such a large discount to book value.

Encouraging News

In other encouraging news, Chatham Lodging increased the size of its unsecured credit facility in December. Thanks to a commitment from Royal Bank of Canada, the trust increased its senior unsecured revolving credit facility by $45 million to $260 million.

The increase in available liquidity indicates that lenders are willing to lend larger sums of capital to the lodging trust, which supports my claim of a fundamental recovery at Chatham Lodging. Following the announcement of the dividend reinstatement, the revolving credit facility was increased.

Why CLDT Could See A Lower Valuation

Because of their reliance on the overall health of the economy, the lodging and hospitality sectors are inherently volatile. People travel and spend more money during good economic times, so CLDT should be viewed primarily as a cyclical business with higher-than-average AFFO and occupancy risks.

If the U.S. economy avoids a recession, Chatham Lodging will perform well, and occupancy/price trends will continue to improve. A downturn in the economy would almost certainly be a bad omen for Chatham Lodging and the trust’s dividend growth prospects.

My Conclusion

Chatham Lodging Trust is experiencing a significant rebound in key portfolio metrics, indicating improved financial and operational health. The trust also reinstated its dividend a month ago, putting the stock back into play for passive income investors.

Despite the fact that the dividend has been reinstated at a much lower level than before the pandemic and the stock yields only 2%, I believe that a continued recovery trend could result in generous dividend increases in the future.

Despite major performance benchmarks pointing upwards, Chatham Lodging is currently available for a 23% discount to book value and pays out only 14% of AFFO. Both the stock and the dividend are appealing and have potential.

Be the first to comment