Torsten Asmus

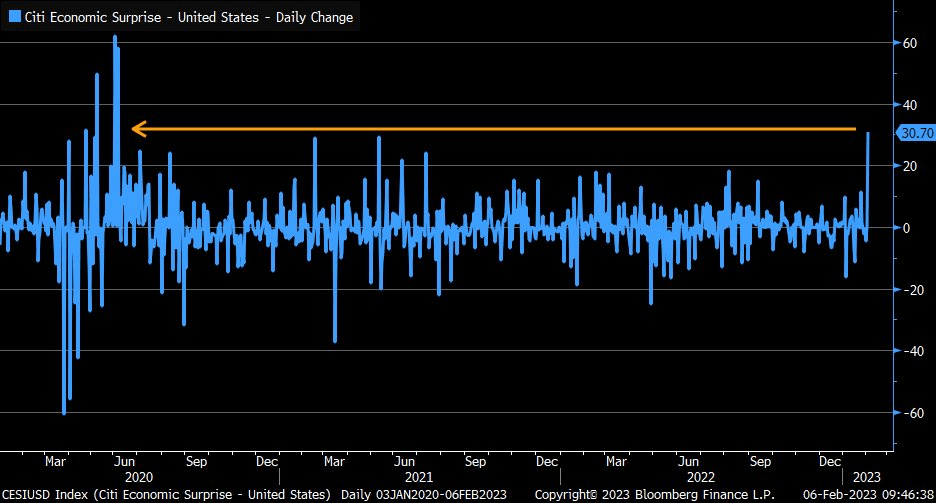

A gangbusters January jobs report last week and some hawkish Fed jawboning early this week have sent bond investors scurrying. Yields are up across the curve, but I view the move as a buying opportunity for investors looking to get a solid yield with minimal credit and duration risk. The Citi Economic Surprise Index had its biggest one-day advance since June 2020, according to Schwab’s Liz Ann Sonders. I see a way to play this market shift.

Surprise! Impressive Economic Data Lately

Schwab, Bloomberg

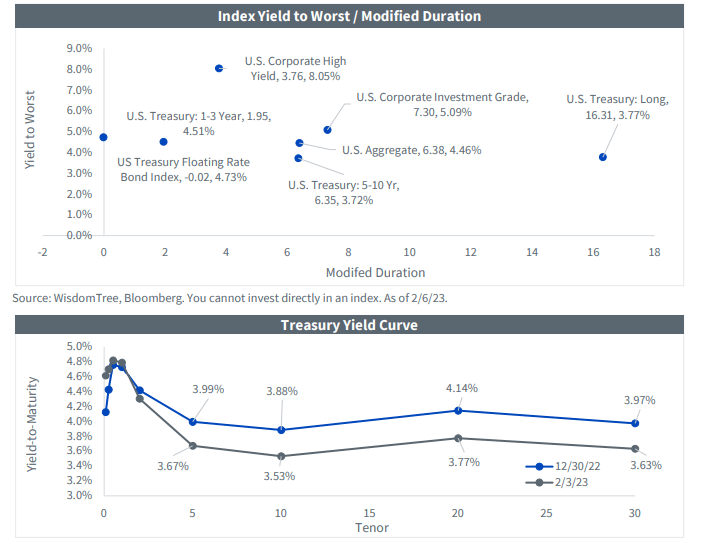

According to the company site, the Vanguard Short-Term Bond ETF (NYSEARCA:BSV) tracks the performance of the Bloomberg U.S. 1–5 Year Government/Credit Float Adjusted Index, a market-weighted bond index that covers investment-grade bonds with a dollar-weighted average maturity of 1 to 5 years. The fund has a low 0.04% annual expense ratio and pays a 4.27% 30-day SEC yield.

It’s a liquid fund with a 30-day median bid/ask spread of just a single basis point while it trades more than three million shares daily. It’s key to look at a bond ETF’s current yield-to-maturity for a gauge on your expected return, and that figure has jumped back up to 4.6% after a significant jump in the front end of the Treasury yield curve since late last week.

US Bond Market Yields & Maturities

WisdomTree

With money market rates near 4.5% these days, you might wonder why even bother owning the bond market. Well, there’s something to be said for locking in some yield with a longer duration rather than relying on Fed policy to dictate your money market return. So, taking a smidgen of duration risk might be wise in case rates drop from here.

With an average effective maturity of 2.8 years and an average duration of 2.6 years, even a big rise in rates from here will not wipe away the income yield enough to make your overall total return negative. What’s more, with short-term inflation swaps pricing in an inflation rate barely above 2%, you can certainly expect a positive real yield on BSV. Of course, a major rise in rates could lead to an NAV drop.

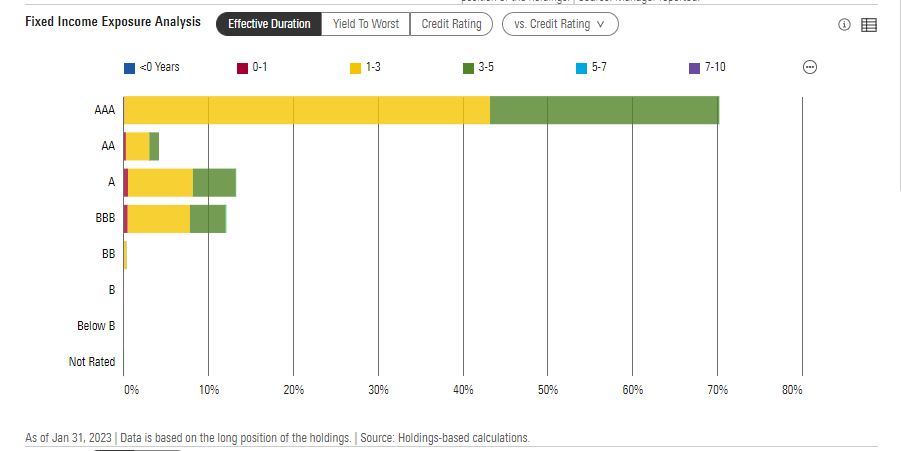

I like BSV since it spreads out risk a bit compared to owning something like SHY which is purely Treasuries. BSV has some investment-grade corporate debt which also features modestly higher yields versus T-notes and T-bills. 68% of BSV is U.S. government securities while slightly more than a quarter of the ETF is actually on the low end of the quality spectrum for high-grade corporate issues.

BSV: Mainly AAA-Rated Holdings

Morningstar

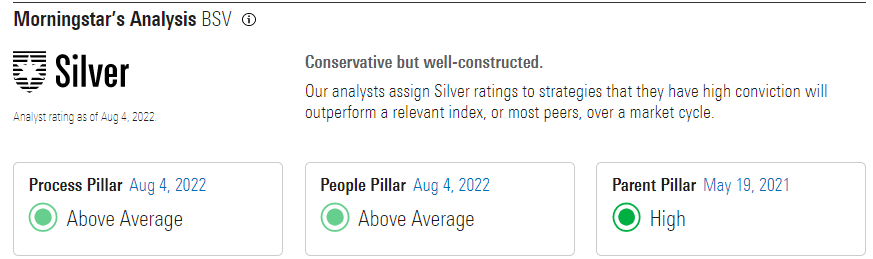

Morningstar rates the fund with a solid silver. According to the fund research site, BSV has above-average process, people, and parent pillars. I am confident that this index will do its job, so what I look to the most is the ETF’s expense ratio and tradeability – both of which are great with BSV compared to similar products.

BSV: Highly Rated by Morningstar

Morningstar

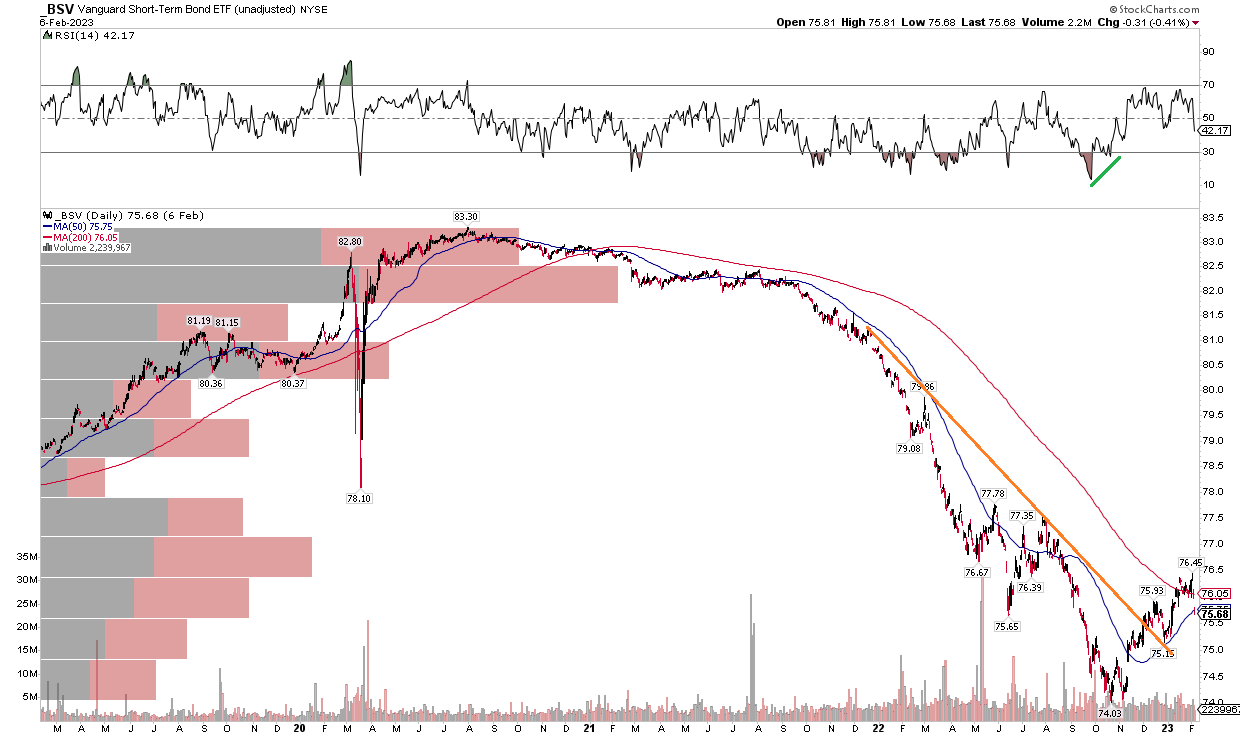

The Technical Take

In my previous write-up, I didn’t look at the chart very much. But let’s do a little technical work on BSV to see if there are any clues on where the near-dated fixed-income market may go from here.

Notice in the graph below that shares put in a low back in October around the September CPI report when yields surged and then began to fall into year-end. BSV successfully held that low on a retest in early November (which occurred on bullish RSI divergence), and has since rallied.

A quick and hard bond market selloff following the January NFP report has brought BSV about one percent off its highs – back to its 50-day moving average. I think now is a good spot to reach for some yield – I see support potential at the June low of $75.65 and further cushion likely at the early 2023 low near $75.15. With a 200-day moving average turning flat, the trend may change in favor of the bulls.

BSV: Downtrend Broken, Bullish Divergence at the Low

Stockcharts.com

The Bottom Line

I continue to like BSV and see the recent rise in yields as a chance to secure some better rates through high-quality corporates with near-dated maturities as well as in elevated Treasury rates.

Be the first to comment