G0d4ather

Broadcom’s (NASDAQ:AVGO) earnings proved the company is not only growing semiconductor revenue in the face of a colossal collapse of the industry’s demand but is proving its already positioned to deal financially with a recession. Of course, this doesn’t mean the company won’t see revenue growth turn negative or its profits won’t decline substantially – no company is immune to this in a recession – but the company has taken a defensive stance going into 2023 in case a recession hits. This allows its dividend to continue to be paid and its debt to continue to be serviced. This is why the company has had some of the best returns in the semiconductor sector and will continue to outperform.

With recession fears stoked to the highest levels, the focus is on which companies are best positioned financially, fundamentally, and managerially to weather a full-on recession. Business practices such as customer engagement and inventory and supply chain management can make or break cyclical-sensitive stocks during an economic downturn. Broadcom hit on these key topics during its most recent earnings call.

The Proof Is In The Pudding

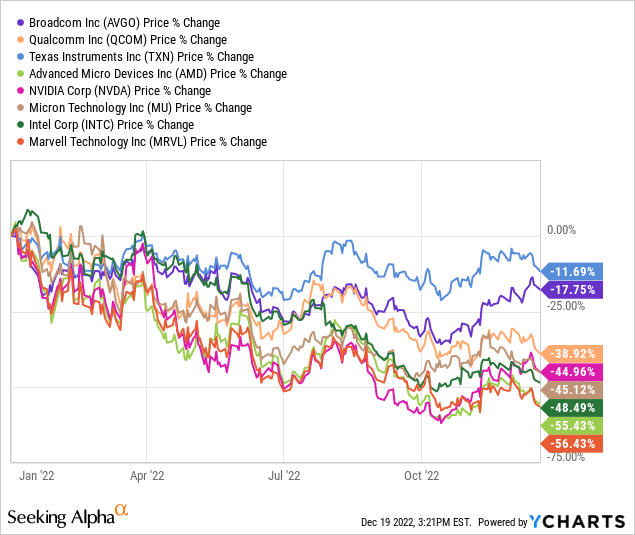

If you compare Broadcom’s 2022 returns with any of its semiconductor peers, it has one of the highest returns. It falls second only to Texas Instruments (TXN), which I have detailed has evaded most of the recessionary selling pressure as it’s the least connected to the retail markets. But Broadcom has the superior financial structure and continues to outperform in the free cash flow department against TXN.

This best-foot-forward entrance to a recession-prone environment allows Broadcom to enact what it already has already set in motion. Moreover, it’s going into a weak economic time with growth flourishing while peers cut estimates wholesale.

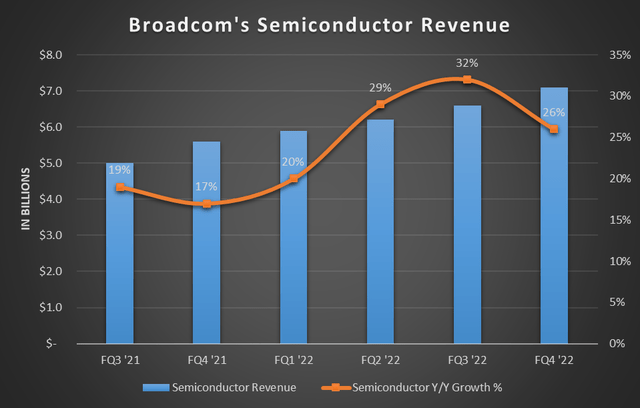

The company’s overall revenue in FQ4 grew 21% year-over-year, but its semiconductor division grew 26%. And with the weakness across the semi industry, it’s worth noting Broadcom hasn’t seen much weakness over the last six quarters, even with the worst for AMD (AMD), Nvidia (NVDA), Intel (INTC), Qualcomm (QCOM), and Micron (MU) coming in the last quarter and continuing through the current quarter.

In fact, the company has accelerated growth in its semiconductor segment from 17% in the year-ago quarter to 26% in the just-reported quarter. And it has done this for at least the last three quarters.

This isn’t the picture we’re getting in other semiconductor corners of the world.

Chart mine, data from AVGO’s earnings reports

In FQ1, management expects semiconductor revenue to grow around 20%, so the growth will continue, matching last year’s quarter. The outperformance comes from divisions like storage connectivity, broadband, and networking, which are expected to grow 50%, 30%, and 20% year-over-year, respectively, in Q1.

Things seem pretty robust for Broadcom’s semiconductors.

The problem is the company is beginning to lap this past fiscal year’s strong growth.

While it’s guiding for 16% year-over-year growth on $8.9B, it’s simultaneously guiding for flat quarter-over-quarter revenue for Q1. The weakness is coming from the software division as it expects to see it flat year-over-year. But, semiconductor revenue is guided for $7.08B, which is down roughly $20M sequentially, even though the semiconductor segment will be up 20% year-over-year. This is the beginning of tough comps going into FY23, and it ramps up from here.

But the reasons for this flattening setup are important.

One of the primary reasons is the company is still planning to ship under demand, as it has been the last year.

I just want to assure you, we don’t believe we are shipping beyond true demand. We continue to scrub — to basically judge orders, the backlog we have, and we also take pains to only ship to customers who can consume it pretty much within the same quarter before we do it. And so, as far as we can tell, based on what we see as a willingness of our customers to accept and consume the products we ship, that’s what we see right now.

– Hock Tan, CEO, Broadcom’s FQ4 ’22 Earnings Call Q&A

This is a good segue into the longer-term look of the fiscal year.

Naturally, the question of, what happens if demand and the backlog fall off? It’s great to be shipping at or under demand, but if demand dives, what then? To start, Broadcom has non-cancellable orders with its customers. But even then, CEO Hock Tan is still unsure how it plays out in a real-world scenario:

What if we all hit a massive recession, depression or recession, late next year, in the next 6 months, 9 months, and customers — and things really collapse around years, what would we do? My answer is I don’t know, which is partly why we’re not giving you annual guidance. We will react as and when circumstances require us to do. But at this point, we have the orders.

– FQ4 ’22 Earnings Call Q&A

Right now, things look good, but if a recession or worse hits, it’s possible Broadcom isn’t going to recover its backlog. There might be cancellation fees in its contracts, and it’s what customers will do as they won’t want to take shipments of products they won’t use, but it won’t make up for the loss of the backlog. Therefore, Broadcom isn’t immune from a total collapse of the economy, but it is one of the better-performing ones while the economy treads water.

Exactly Why Is It The Best Prepared?

At this point, you’re likely wondering why I’ve titled this article around Broadcom being the best prepared. After all, I did say its CEO doesn’t know what would happen if demand disappears.

My point is not necessarily what happens in a worst-case scenario but how the company is set up to handle the worst-case scenario.

First, the company continues to under-ship customer demand.

It comes down very simply to we continue to scrub our backlog in a manner this quarter, last quarter, no differently than we did it six months or a year ago. We haven’t changed our focus on ensuring that we do not ship products to the wrong people who just put it on the shelves. That is still very much, very, very intact in our view.

This means the company keeps inventory low internally and at its customers. Therefore, if demand drops off a cliff, there isn’t a massive overhang of inventory of Broadcom’s products on shelves. Inventory overhangs prolong recoveries in cyclical industries as they must be drawn down before the supply chain ramps up again. This delays purchasing from companies like Broadcom, but when there’s no slack in the supply chain to take up, it more or less immediately goes back to ordering.

Second, the company set up its capital return program to be conservative in FY23. It started with a “modest” 12% dividend raise. The company’s policy has been to return 50% of the prior year’s cash flow to shareholders. However, in keeping with the 22.5% growth in free cash flow for the year and a consistent portion of 50% of last year’s free cash flow would amount to a 21% or slightly more ($19.93 for the fiscal year versus the $18.40 approved) increase in the dividend. Considering it made up 52.3% of the prior year’s free cash flow, this year’s dividend will only make up 48.2% of the prior year’s free cash flow.

The company has taken a conservative approach, admitting as much, and supplementing with the buyback program.

…we’ve always said we would pay out approximately 50% of the preceding year’s free cash flows. And in this economic environment that we’re all seeing, we believe that a 12% increase year-over-year is a robust dividend.

– Kirsten Spears, CFO, Broadcom’s FQ4 ’22 Earnings Call Q&A

According to management, it hasn’t been able to repurchase shares since announcing its acquisition of VMware (VMW). It expects to resume the program once regulations allow. However, management has taken advantage of this self-directed allocation policy to work in its favor of being conservative in committed capital. It can reach its 50% policy on an as-needed basis using the share buyback program. Therefore, it can raise the dividend less, so capital is not overly committed. A 12% increase is meaningful, to the CFO’s point, but it’s less than anticipated, as I described above.

This puts the company in a more flexible position should things go downhill quickly. After all, they aren’t required or committed to using the buyback program, much like any other company’s policy. Therefore, if they miss the 50% capital return program it created, it’s not as big of a deal, nor scrutinized as much, as a dividend cut. The latter would be a black spot in a company’s history for years, if not decades.

Instead, by under-committing to the 50% mark for the dividend, the company only needs to spend $281M in FY23 on the buyback to meet the 50% requirement. In contrast, the company returned 116% of last year’s free cash flow in FY22. Management is set up well to conserve free cash flow in FY23 and meet both its newly raised dividend and its 50% preceding year free cash flow policy. Basically, free cash flow can contract by 50% in FY23 and still maintain its shareholder commitments while using its $12.4B in cash to service debt.

A Cornerstone Of Any Tech Portfolio

The company is being about as defensive as it can manage without materially hurting growth or profitability. In addition, leveraging the share buyback program allows it to moderate how much free cash flow it uses quarter-to-quarter. This gives it the flexibility to hit targets using the visibility of the first half of the year versus committing to a much higher dividend for the entire year.

I’ve always said Broadcom’s management is one of its greatest assets, and this defensive nature is another indication of it. Of course, it doesn’t mean it will make it through a recession unscathed, but it has been taking steps to position itself in the event of one. This is why I let it remain my top holding in my portfolio.

Be the first to comment