fotoVoyager/E+ via Getty Images

Investment thesis

Our current investment thesis is:

- Brexit, e-commerce, working-from-home, and economic conditions are acting as a drag on BL’s performance. We are concerned that the company faces a continued decline.

- BL is highly indebted but we are not too concerned given the low LTV and negative real rates.

Company description

British Land Company (OTCPK:BTLCY) is a prominent real estate investment company with a diverse portfolio focused on high-quality commercial properties in the UK. Its primary assets are London Campuses and Retail & Fulfilment properties throughout the country. With a portfolio valued in excess of £10bn billion, BL is one of Europe’s largest listed real estate investment companies, with a significant portion owned or managed.

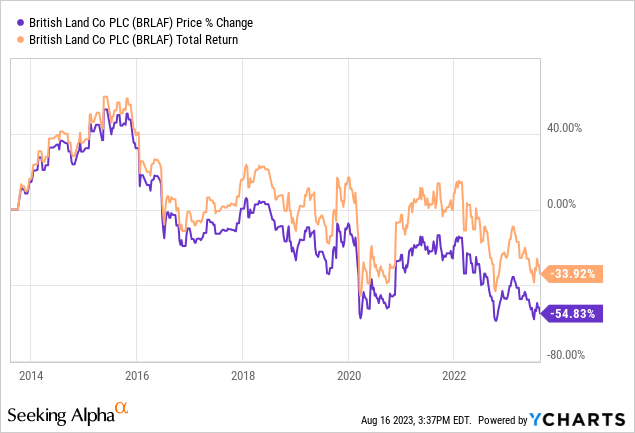

Share price

BL has had a terrible decade, losing almost 51% of its value across the decade. This is driven in part by the value of the properties held by the company but also by a period of commercial difficulty.

Financial analysis

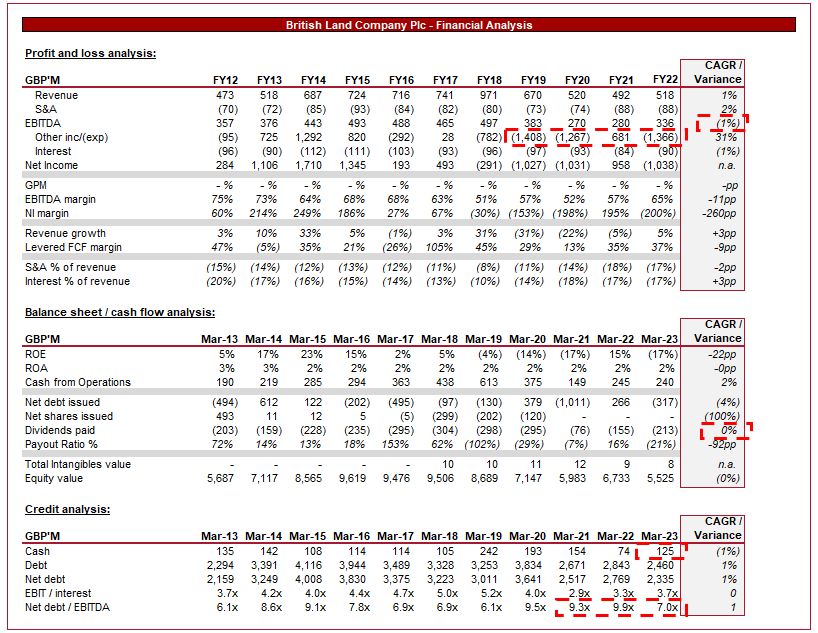

British Land financials (Capital IQ)

Presented above is BL’s financial performance for the last decade.

BL’s revenue has remained flat across the historical period, growing at a rate of 1%. The vast majority of BL’s revenue is rental income from its portfolio of properties. Further, BL’s expenses relate primarily to the maintenance and improvement of said properties, as well as the servicing of financing debt.

Given we are discussing a property company operating solely in the UK, it is inevitable that we must discuss Brexit. The UK voted to leave the European Union in late 2016, contributing to global dismay at what was seemingly an own goal. For many decades, the UK has been home to substantial global investment, and the vote created material concerns about if the UK would lose economic value. This immediately contributed to a softening of investment in commercial real estate. The immediate concern here is that BL relies on both rental income and capital appreciation. The latter allows for long-term expansion as when capital value increases, the company is able to raise further debt to finance projects / acquisitions. If the opposite occurs, the likes of BL face solvency risks and thus most downside / shore up finances.

The rapid growth of e-commerce has led to reduced retail footfall, as consumers value the benefits of delivery convenience and the ability to shop around. This has been partially offset by a rapid rise in the demand for logistics and warehousing spaces, particularly for last-mile delivery operations. British Land has recognized this trend and strategically invested in logistics properties located near major urban centers. This has reduced the impact of softening retail demand, where many of their locations have seen valuations flatline / decline.

In recent years, Covid-19 has compounded the impact of these factors, giving rise to a structural shift in consumer behaviors. The most recognizable change is the rise of working from home. A recent report has found workers in Central London are attending the office an average of 2.3 days. Consumers are increasingly valuing the benefits of staying at home, as such spending more time with their family, which for commercial real estate owners is a disaster. Not only is office occupancy at record low levels (outside of Covid-19) but related industries are being impacted, such as retail (If a consumer doesn’t go into the office, they are not going to buy lunch and may not engage in retail after). This is perfectly exemplified by British Land’s Broadgate campus, which is in the heart of the City of London. This location relies heavily on the footfall of financiers on a daily basis. If the WFH continues, the ability to continually raise rent and benefit from capital appreciation will be reduced relative to the past.

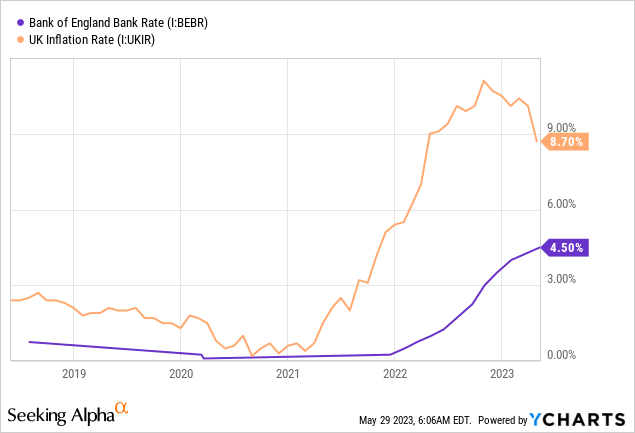

The real estate industry is heavily intertwined with the economy as a whole. The UK has seen rampant inflation, which is showing itself to be incredibly stubborn, contributing to consistent rate hikes as a means of bringing it under control.

The impact on BL is multifaceted. Firstly, property values and rates are generally negatively correlated. This is because as rates rise, the cost to finance purchases increased, contributing to a decline in demand.

Secondly, BL is the largest owner and operator of retail parks in the UK. Inflationary pressures are contributing to reduced retail spending, increasing the risk of rent defaults, tenancy changes, and value depreciation.

These 4 overarching factors have contributed to the large NI losses BL has posted in recent years, as its portfolio is marked-to-market for reporting purposes. The concern is that rental income is not increasing and in fact, has fallen since the middle of the decade while property writedowns have contributed to a 42% fall in equity value over 5 years.

Balance sheet

BL is highly indebted. For most businesses, a 3x ND/EBITDA ratio is a healthy maximum. For a property business, significantly more can be sustainably managed due to the nature of property loans. When the loans were agreed upon, BL will have provided sufficient equity so as to protect against solvency risks. If the company needed to sell for whatever reason, it would be in a position to repay the principal and have capital left over.

The key risk is that with rates rising substantially, BL will see a decline in its equity value as property prices fall. The company is in a sufficient equity position to alleviate immediate concerns with a LTV of 26.2%.

Further, with this level of debt, the other concern is that the cost of financing rises. Although this will be a drag on finances given BL has some floating rates, we must remember that inflation is just under double the BoE rate (BL will be borrowing at more than this), and so on real terms, BL is benefiting.

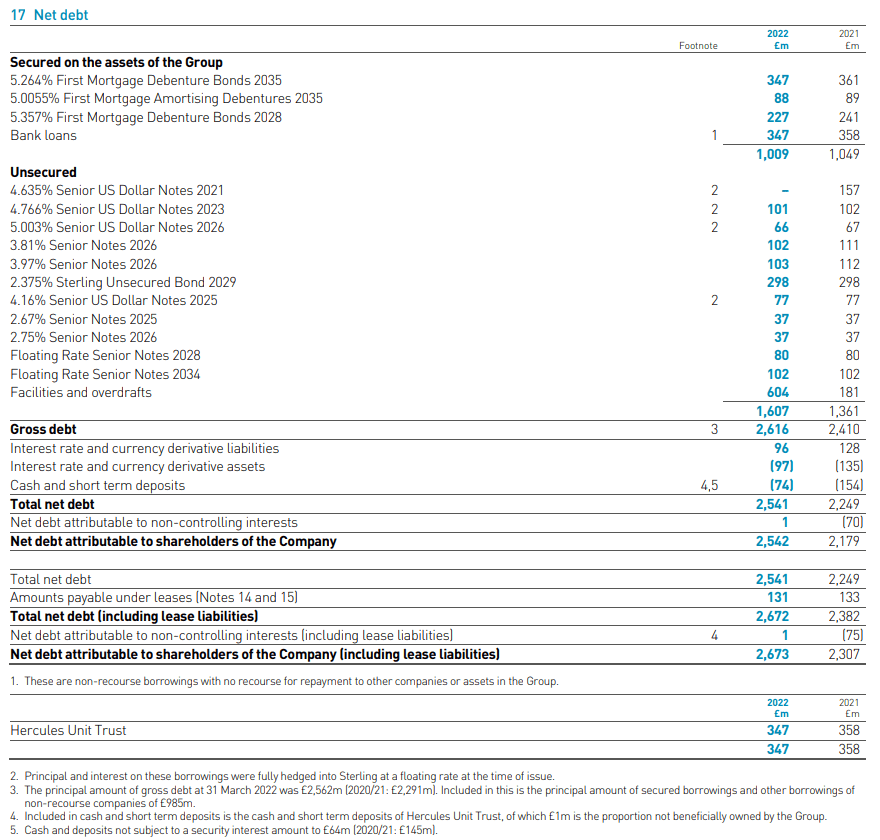

Find below BL’s debt profile.

Debt (British Land)

Valuation

Valuation (Seeking Alpha)

BL is trading at 16x LTM EBITDA and 13x Cash flow. This reflects a noticeable discount to its historical trading range, implying a decline in performance.

This looks to be warranted, given the issues the company has faced in recent years. We are concerned with the decline in rental income, which will impact yields.

BL has developments/projects ongoing which should support rental growth in the future, however, the current iteration is unattractive in our view.

Final thoughts

BL owns several highly valuable assets with good rental yields. However, the current position of the company makes it unattractive. We are seeing trends working against the company, rental income is poor, and short-term headwinds from economic conditions mean we are unlikely to see positivity in the next 12-18 months. We believe dividend payments and its share price could fall further.

BL would do well to further expand its portfolio and invest in growth areas rather than increasing its exposure to more of what it already offers.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment