wildpixel

British American Tobacco (NYSE:BTI) has outperformed the S&P 500 (SPY) (SPX) since we encouraged investors to buy in September. However, a selloff leading to its September lows likely freaked out some weak holders as they reacted negatively to the market volatility in Europe then.

However, BTI recovered all its losses and more toward its December highs before it met with robust selling resistance. Accordingly, sellers forced a bull trap before the company released its FY22 pre-close update on December 8. Accordingly, BTI highlighted FY22 revenue growth of 3% (midpoint) and reaffirmed mid-single growth in its adjusted EPS guidance. Both metrics are based on constant currency terms.

BTI’s robust dividend yields have also helped lift its performance against the SPY over the past four months. Despite the surge from its September lows, BTI still posted an NTM dividend yield of 7.3%, well above its 10Y average of 5.7%. Therefore, the market remains tentative about its transformation to reduced risk and oral products.

However, the critical question facing investors now is whether the recent pullback represents an opportunity to pull the buy trigger if they missed BTI’s September lows.

We believe the key to assessing the market’s confidence in continuing BTI’s recovery is how worsening macroeconomic headwinds could impact its growth cadence in 2023.

Europe is likely already in a recession due to surging energy costs. However, the company highlighted in its pre-close call that it sees more resilience in the US. Consumers have traded down. However, energy costs have declined, while inflationary pressures could moderate further through 2023.

As such, the company expects to remain solidly profitable through the cycle and continue its transformation, as it aims to reach post “£5 billion in new category revenue and profitability by 2025″ while also adding 50M consumers for its noncombustible products by 2030.

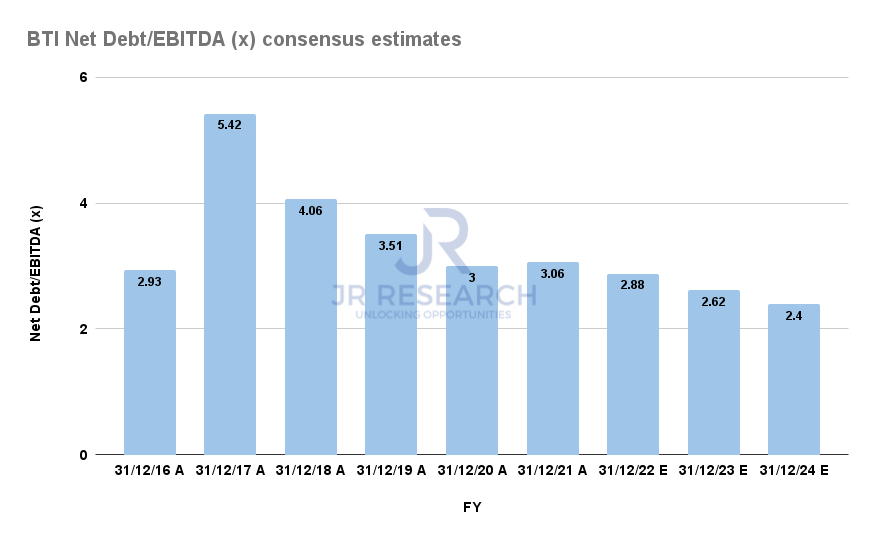

BTI Net debt/EBITDA consensus estimates (S&P Cap IQ)

Also, the company indicated that it intends to continue reducing its leverage, which should help mitigate its interest expense, and improve its free cash flow (FCF) conversion.

Analysts’ estimates suggest it should hit its 2.4x Net debt/EBITDA multiple of 2.5x by the end of 2024. The company also highlighted that its capital allocation priorities would remain prudent, likely expecting elevated interest rates to continue in the medium term.

Therefore, we believe it suggests that BTI is increasingly confident that it can continue improving its dividend payout ratios, providing more security for investors. Also, it should proffer investors more confidence that the company could provide a positive FY23 outlook on its buyback program, on top of the £2B share buybacks it committed in 2022.

Hence, we expect the market to be more confident in BTI over 2023 despite worsening macro headwinds, as the world could fall into a recession.

So, the question is whether long-term buyers have defended BTI’s recovery?

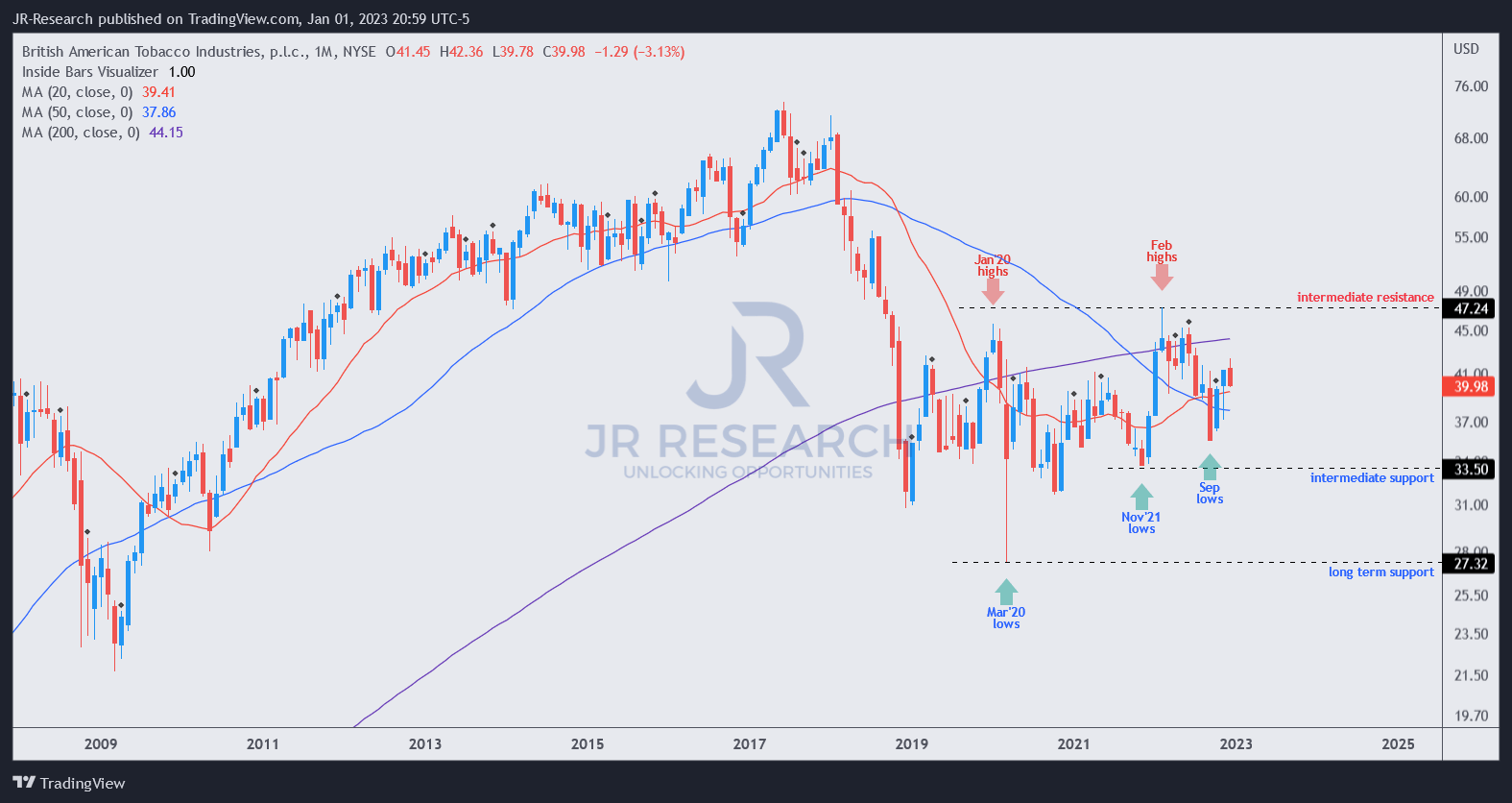

BTI price chart (monthly) (TradingView)

As seen above, BTI has been consolidating remarkably well since its April 2020 bottom. It continued to form higher lows, suggesting buyers returned strongly to undergird deep pullbacks.

Accordingly, we gleaned that BTI remains well supported, even though investors should avoid adding close to its February highs, given the bull trap.

Hence, the price action is constructive, highlighting the market’s increased confidence in BTI executing through the cycle.

Despite that, we think investors need to curb their enthusiasm in expecting BTI to retake its pre-pandemic highs anytime soon until it could breach its February high decisively.

For now, we believe the reward/risk is pretty well-balanced, with upside surprises potential if the company could deliver a better 2023.

Rating: Buy (reiterated)

Be the first to comment