Editor’s note: Seeking Alpha is proud to welcome Malak Investment Ideas as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

tiero

Bristow Group Inc. (NYSE:VTOL), a vertical flight solutions provider, reports long-term agreements, and management recently announced a mass emergency communication system to be implemented from 2023. I believe that new successful M&A operations may bring significantly more demand for the stock. I also see risks from the company’s exposure to the energy industry. With that, I believe that the stock appears undervalued.

Bristow’s Business Model And Competitors

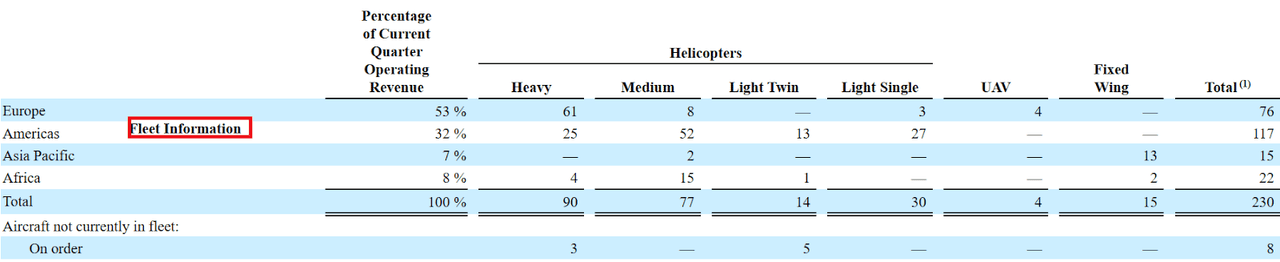

It is not very common to see companies dedicated to this type of service, but the degree of specification and technical development necessary to carry out a business model in this sense is evident. An example is the Bristow Group, which is dedicated exclusively to solutions related to vertical flights for different functions including private transport, energy transport, and rescue services in marine areas. Bristow currently operates in Asia, Africa, South America, the Caribbean, and Europe.

Most of its profit comes from its energy transport segment, representing 67% of the total profit. This is well above the 24% of revenue from government services and aircraft technical assistance.

Out of its active operations, more than half of them take place in Europe, mainly in oil extraction centers and other types of off-shore operations, facilitating the transport of fuels to continental areas. Bristow’s available fleet is of varied aircrafts, with a significant number of helicopters with different designs to offer the solution consistent with the needs of its customers.

Source: 10-Q

Bristow disclosed a sustainability report carried out this year, showing some of the statistics about its commitment to reduce carbon footprint emissions and develop technologies to power its helicopters with clean energy. These objectives also include the transfer of its entire car plant to electric-powered cars as well as various improvements in helicopters to prevent noise pollution in its community.

In relation to Bristow’s future plans, I find remarkable that the company signed an agreement related to the Universal Declaration of Human Rights of the United Kingdom, committing itself to a series of values in relation to non-discrimination, good treatment of its employees, and legality and compliance with contracting requirements. With many investment funds out there looking for companies that present themselves as good employers, Bristow’s new agreements may bring some equity demand.

Bristow offered a list of competitors in the annual report.

Globally, our primary competitors are CHC Group LLC (OTC:CHHCF), NHV Group, Omni Helicopters International, S.A. and PHI, Inc.

I believe that the company has more financial resources than most peers. Hence, I wouldn’t worry much about competition.

Balance Sheet

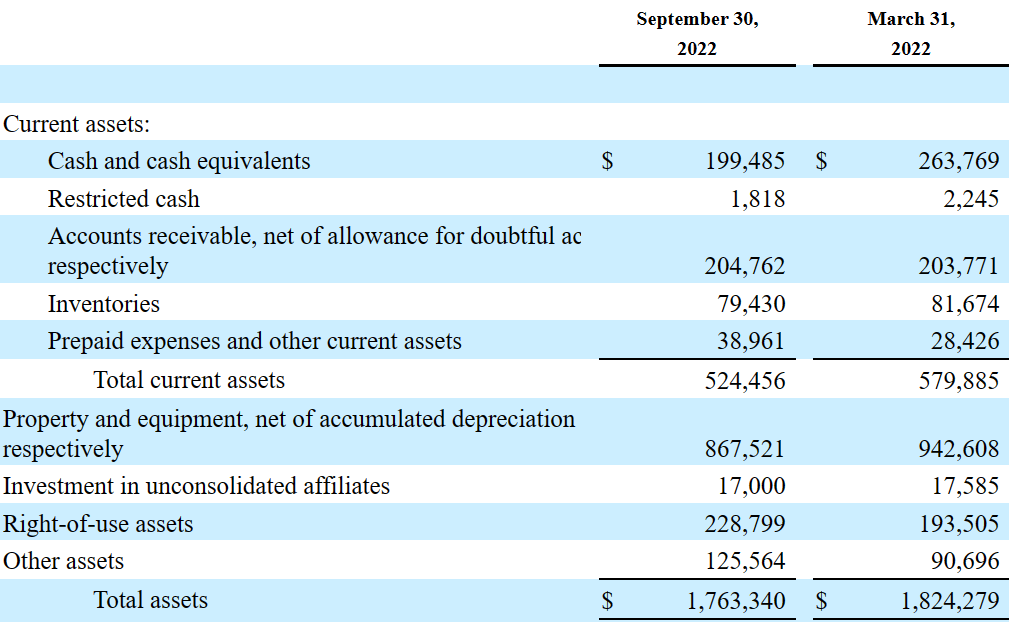

The company’s financial situation as of September 30, 2022 included cash of $199 million, accounts receivable worth $204 million, and inventories of $79 million. Total current assets are equal to $524 million, close to 2x-3x the total amount of current liabilities. Hence, I wouldn’t say that Bristow has a risk of a liquidity crisis.

Property and equipment stood at $867 million, right of use assets were equal to $228 million, and other assets stood at $125 million. Finally, the total amount of assets is equal to $1.76 billion, which implies an asset/liability ratio of 2x. In sum, I believe that the balance sheet appears to be quite stable.

Source: 10-Q

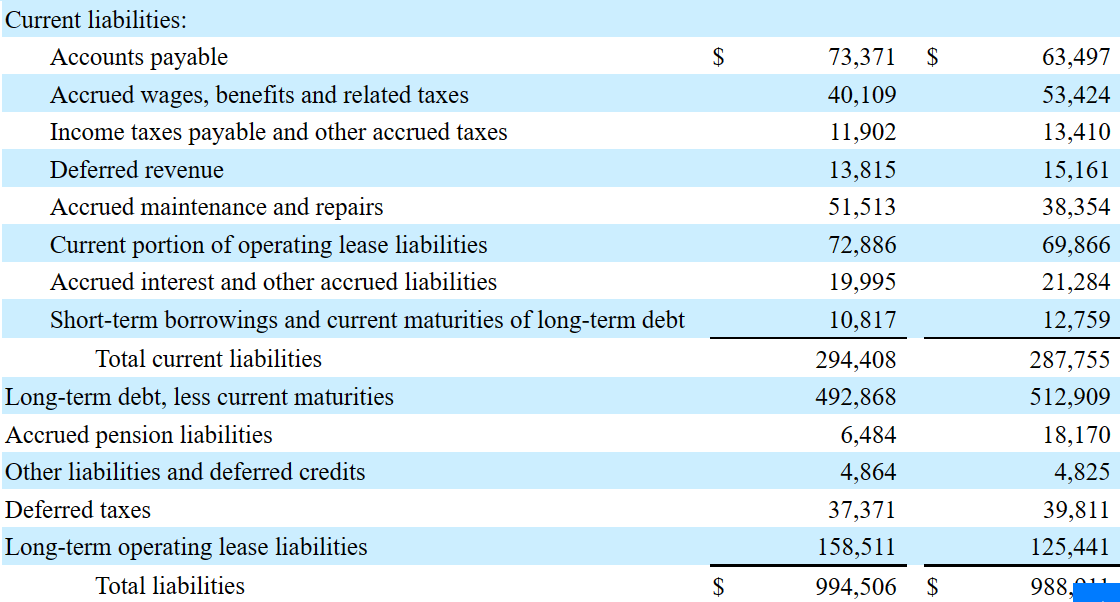

The liabilities include accounts payable worth $73 million, accrued wages worth $40 million, and accrued maintenance of $51 million. Total current liabilities stand at $294 million.

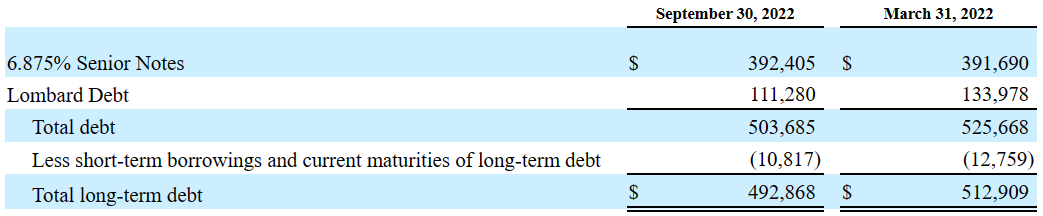

Bristow also reports long-term debt worth $492 million, deferred taxes of $37 million, long-term operating lease liabilities of $158 million, and total liabilities worth $994 million.

Source: 10-Q

Considering future EBITDA, I really don’t believe that the company’s net leverage/EBITDA is at worrying levels. I also believe that EBITDA generation appears sufficiently stable to justify the current amount of debt.

Expectations From Analysts

In order to provide its services internationally, Bristow has signed agreements with pilot associations from different countries in which it operates, providing the logistics plans and the necessary equipment to be operated by third parties.

For future years, management expects certain recurrent revenue due to bidding and long-term contracts. In my view, most investors will be interested in the company because of its long-term agreements as they offer some visibility about future sales growth.

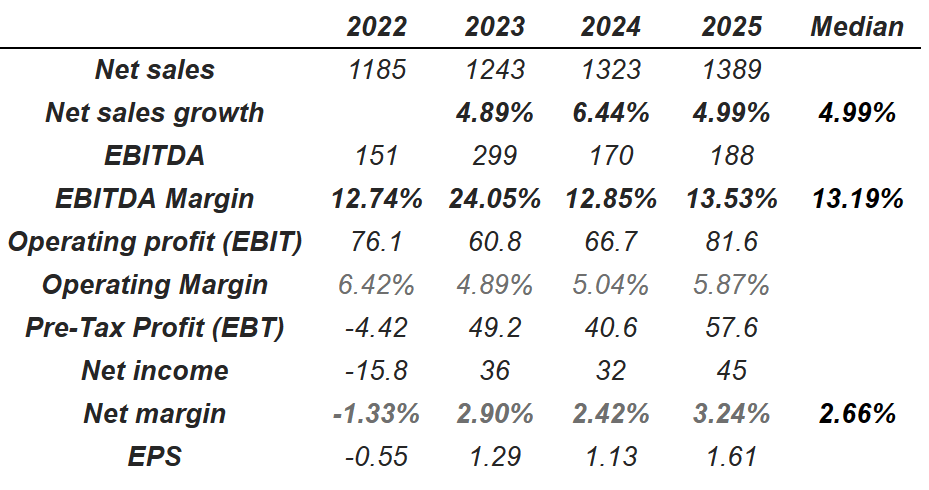

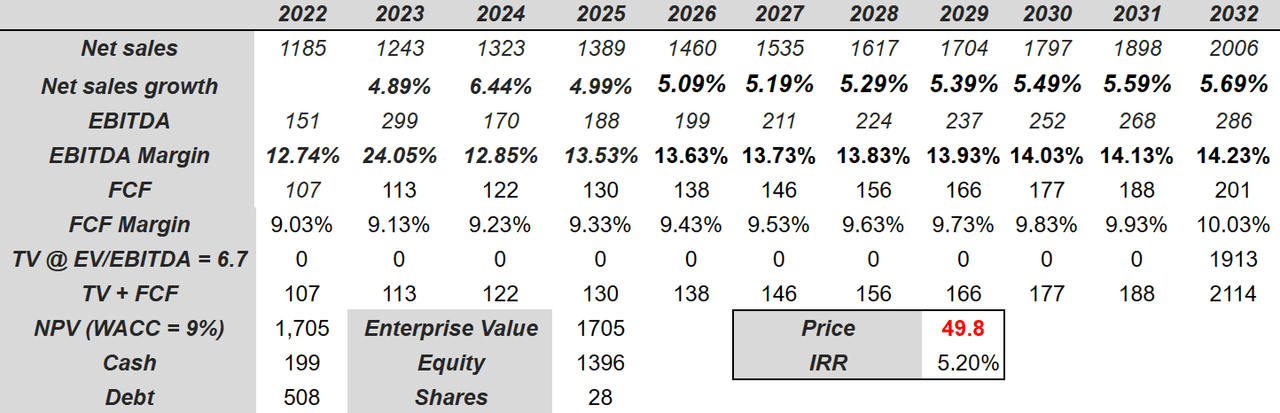

Analysts also report beneficial expectations. Analysts expect 2025 net sales of $1.389 billion together with a net sales growth of 4.99%. 2025 EBITDA is expected to be close to $189 million along with an EBITDA margin of 13.53%. Besides, market estimates include 2025 operating profit of $81.6 million accompanied by an operating margin of 5.87%. Finally, net income would stand at $45 million, with a net margin of 3.24% and EPS of $1.61 per share.

Source: Other Investment Analysts

Mass Emergency Communication Systems May Lead To A Valuation Of $49 Per Share

I am quite optimistic about the new mass emergency communication systems announced in the last quarterly report. The adoption of the new digital incident management system may interest certain clients from fiscal year 2023, which may increase revenue growth.

During the fiscal year 2022, we also enhanced our mass emergency communication system, which we expect will allow for digital incident management to be adopted in fiscal year 2023, and completed the integration of the company safety information system in Brazil, Suriname and the U.S. Gulf of Mexico.

Source: 10-Q

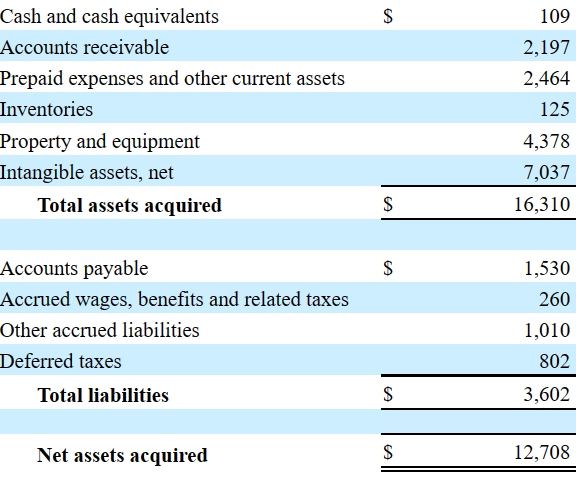

Bristow signed acquisitions in the past like that of British International Helicopter Services Limited among others. Even considering that some of the assets acquired are small, it is worth noting that management has M&A expertise. Inorganic growth may interest investors out there. British International Helicopter’s balance sheet is given below.

Source: 10-k

Let’s also mention that Bristow reported in the last quarterly report that management continues to evaluate new acquisitions. In my view, if the market appreciates new transactions, the stock price may trend north.

We continuously evaluate the acquisition or disposition of operating businesses and assets and may in the future undertake one or more of such transactions. Any such transaction could be material to our business and could take any number of forms, including mergers, joint ventures and the purchase of equity interests. We also routinely evaluate the benefits of disposing of certain of our assets.

Source: 10-K

Finally, I believe that further reduction in the long-term debt as we saw in the last quarterly report may bring stock demand. In my view, lower debt may justify higher EV/EBITDA multiples, which would lead to higher stock valuation.

Source: 10-Q

Under this scenario, I assumed 2032 net sales of $2.006 billion and net sales growth of 5.69%. In addition, I included 2032 EBITDA of $286 million accompanied by an EBITDA margin of 14.23%. I also believe that 2032 FCF will likely be close to $201 million with a FCF margin of 10.03%.

Source: Author’s DCF Model

If we include an EV/EBITDA multiple 6.7x, 2032 terminal value would be $1.913 billion. The NPV of future FCF and the terminal value would be $1.705 billion. Besides, with cash of $199 million and debt of $508 million, I obtained an equity valuation of $1.396 billion, a fair price of $49.8 per share, and an internal rate of return of 5.20%.

Risks Could Imply A Valuation Of $20 Per Share

The long-term commercial agreements and agreements with regional pilot associations are expected to expire during the fiscal years of the next decade. This means that the company may be forced to expand its client portfolio and generate new commercial and government sponsorship agreements. With new clients, I would be expecting sales growth declines and perhaps diminishing EBITDA margins. Changes in regulations, not only regarding flight conditions and technical requirements of aircraft, but also changes in the provision of international trade agreements according to each region, are among various risk factors.

Another risk factor is the company’s dependence on the income generated by the energy transport services. This makes Bristow indirectly dependent on the commercial decisions of its clients or the resources and durability in extracting them. As pointed out earlier, this segment of its business model represents 67% of its annual profits. If Bristow does not diversify its activities a bit, I believe that demand for the stock may diminish.

In the last annual report, Bristow reported that a few customers were responsible for close to 66% of the total operating revenue. In my view, certain investors may not appreciate the concentration of clients as losing one of them may lead to revenue declines and stock price declines.

During the fiscal year ended March 31, 2022, our top ten customers accounted for approximately 66% of operating revenues, and the combined revenues from DfT, Equinor ASA and ConocoPhillips Co. accounted for 38% of our operating revenues.

Source: 10-K

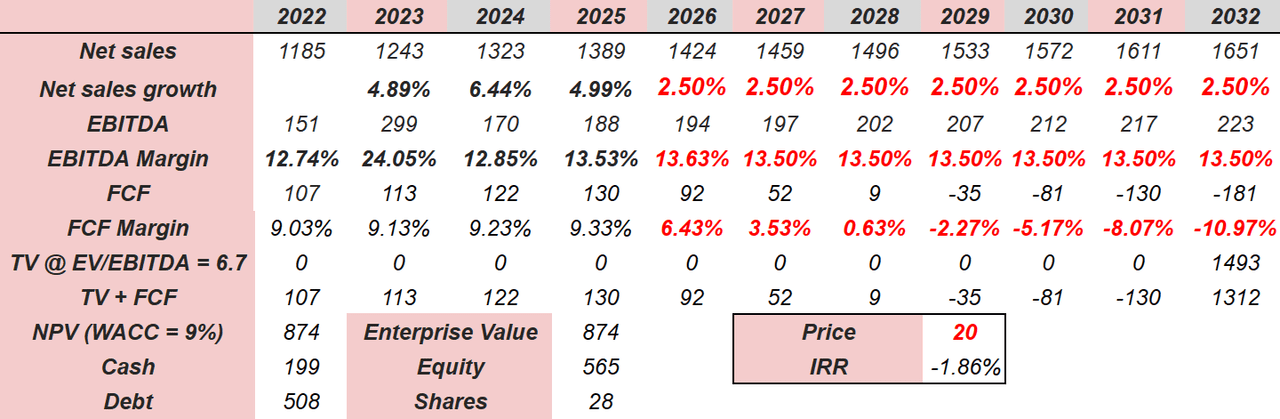

Under the previous conditions, I assumed 2032 net sales of $1.65 billion, 2032 EBITDA of $223 million, and an EBITDA margin of 13.50%. In addition, I included 2032 FCF of -$181 million accompanied by a FCF margin of -10.97%.

If we also assume an EV/EBITDA multiple close to 6.65x, the sum of the terminal value and FCF in 2032 would be close to $1.312 billion. My results with a WACC of 9% would include a net present value of $874 million. Also, with cash of $199 million and debt of $508 million, the equity would be $565 million. Finally, the fair price would be close to $20 per share with an IRR of -1.86%.

Source: Author’s DCF Model

Conclusion

Bristow reports a significant number of long-term agreements with clients from many countries, which many investors will consider recurrent revenue. I also believe that the new mass emergency communication system to be implemented from 2023 could bring the attention of many investors. Finally, if management successfully continues to reduce its long-term debt, and finds more beneficial M&A operations, Bristow may receive even more attention from the investment community. Even considering risks from concentration of clients and dependency on the energy industry, in my view, the stock is undervalued.

Be the first to comment