Investment Thesis

Braemar Hotels & Resorts (BHR) delivered a solid Q4 2019 thanks to several of its renovation and conversion projects reaching completion last year. These projects should continue to contribute to its revenue favorably in 2020 if everything goes smoothly. However, due to the outbreak of coronavirus, we believe Braemar’s revenue and average daily rates will be impacted negatively. Hence, we are not optimistic about its total growth in 2020. Since visibility is limited, investors may want to stay on the sidelines.

Recent Developments: Q4 2019 Highlights

Braemar reported a strong Q4 2019 as it saw its revenue per available room (RevPAR) increased by 9.9% to $233.70. Similarly, its comparable RevPAR grew by 6.2%. In the past quarter, its comparable RevPAR was about 5.5% higher than the national average for luxury class hotels. Its adjusted EBITDA of $25.5 million was a growth of 25% year over year. This was primarily due to the reopening of its Ritz-Carlton St. Thomas hotel two years after Hurricane Irma, completion of the conversion of its Courtyard Philadelphia hotel to The Notary Hotel, and the opening of The Maple Grove Presidential Villa at the Bardessono Hotel & Spa in Yountville, California.

Earnings and Growth Analysis

The outbreak of coronavirus will impact Braemar’s revenue

The outbreak of coronavirus is quickly developing into a global pandemic. As a result, the hotel industry is now facing a very strong headwind as businesses and individuals avoid any unnecessary travel activities. We expect Braemar’s occupancy ratio and average daily rate to take a significant hit in this environment, especially because its hotels are mostly luxury and upper-upscale hotels located in urban coastal cities (e.g. California, Washington, Florida, New York, etc.). If this virus cannot be quickly contained before the end of April, we think the impact will continue throughout the rest of the year and perhaps even 2021 until a vaccine is developed. We will likely see lower travel activities and this will impact its revenue negatively.

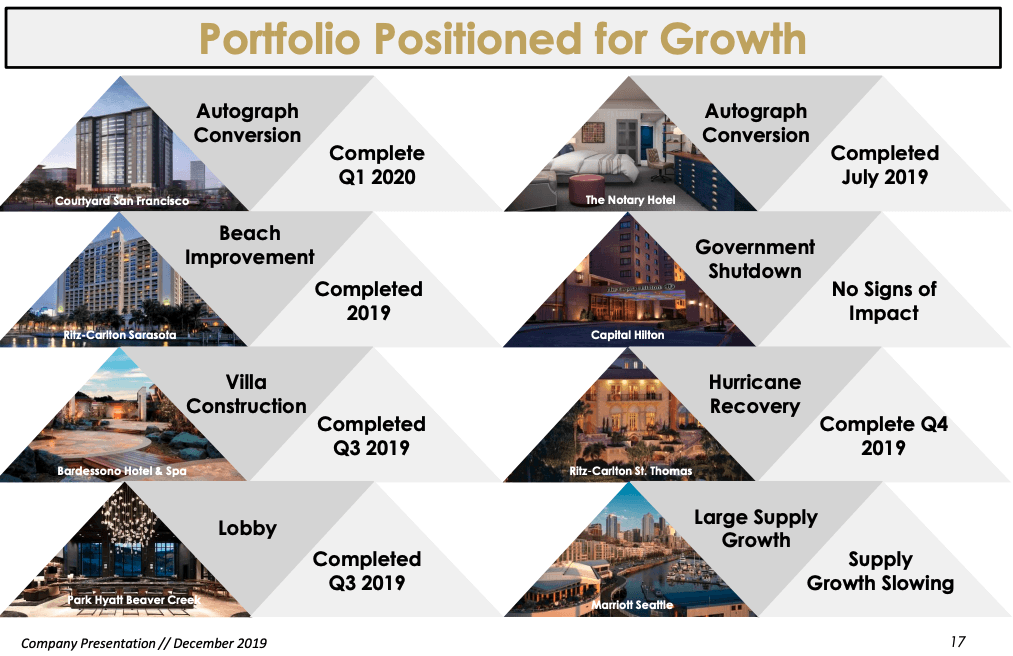

Renovation and conversion projects should improve its portfolio quality

Braemar has several renovation and redevelopment projects to improve the quality of its portfolio. As can be seen from the illustration below, several projects have reached completion in 2019. We expect the conversion of its Courtyard San Francisco hotel to reach completion in Q1 2020. These projects should contribute to its RevPAR, and ADR favorably in 2020 if the outbreak of coronavirus can be contained quickly.

Source: December 2019 Investor Presentation

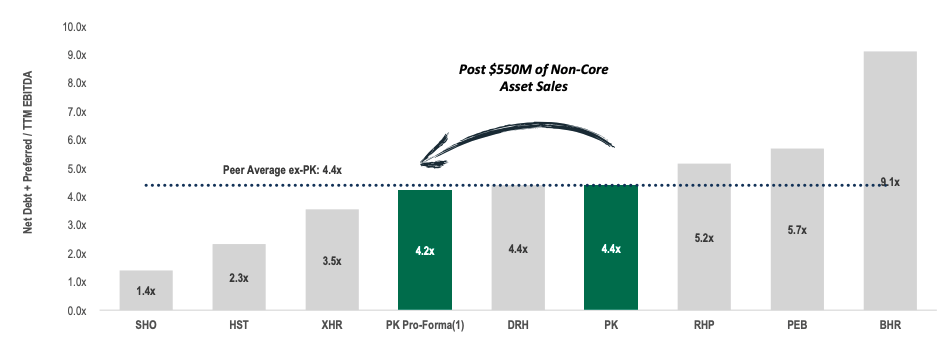

A leveraged balance sheet

Braemar has a leveraged balance sheet with total indebtedness of $1.065 billion. As can be seen from the chart below, the company’s net debt + preferred equity to EBITDA ratio of 9.1x (left in the chart below) is significantly higher than the average of 4.4x of its hotel peers. We do not like its high leverage as its ability to weather some major storms will be limited (e.g. if the outbreak of coronavirus lasts for several years). Fortunately, the company does not have any debt reaching maturity until 2022.

Source: Park Hotels and Resorts Investor Presentation

Valuation Analysis

We expect Braemar’s adjusted funds from operations to decline by 10% in 2020 due to the impact of coronavirus as we believe this will reduce a lot of travel activities in 2020. Therefore, we believe Braemar to generate only $1.27 of AFFO per share in 2020. Using this estimate, Braemar is trading at a price to 2020 AFFO of 2.4x. This is significantly below its historical valuation range of 7x-10x.

An attractive 11.7%-yielding dividend

Braemar currently pays a quarterly dividend of $0.16 per share. This is equivalent to a dividend yield of 21.3%. This dividend appears to be safe with a payout ratio of 45% based on its 2019 AFFO of $1.41 per share. However, we must warn that a significant decline in its AFFO is likely and this could result in a much higher payout ratio in 2020.

Risks and Challenges

An economic recession

The hotel industry is cyclical and the prosperity depends on the strength of the economy. In an economic recession, travel activities may be limited. In addition, a global pandemic such as the outbreak of coronavirus can also cause a significant decline in travel activities.

Risk of elevated supply

Barrier to entry is low for hotels in major markets as cities encourage new hotel supply to promote tourism and increase taxable income. Therefore, the industry will face an elevated supply in many markets from time to time.

Weather

Mother Nature can act as a headwind to Braemar’s revenue. For example, a hurricane can cause a major disruption to its revenues.

Investor Takeaway

Braemar is facing strong headwinds at the moment and we think visibility is very low right now. In this situation, we think it may be wise for investors to wait on the sidelines.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: This is not financial advice and that all financial investments carry risks. Investors are expected to seek financial advice from professionals before making any investment.

Be the first to comment