Leon Neal

Thesis

BP p.l.c. (NYSE:BP) shares are up by as much as 5% in the trading session (London exchange reference) following the oil major’s Q4 and FY 2022 reporting. Supported by elevated energy prices, BP posted exceptional profitability and retired the 2008 net income record. Moreover, reflecting on the China COVID reopening, paired with depleted oil inventory levels, BP voiced confidence going into 2023. And management voiced commitment to further boost shareholder returns with higher dividend payouts and additional share buybacks. Personally, I raise my EPS expectations for BP through 2025, and I now calculate a base case target price of $70.68/share, as compared to $66.55 prior.

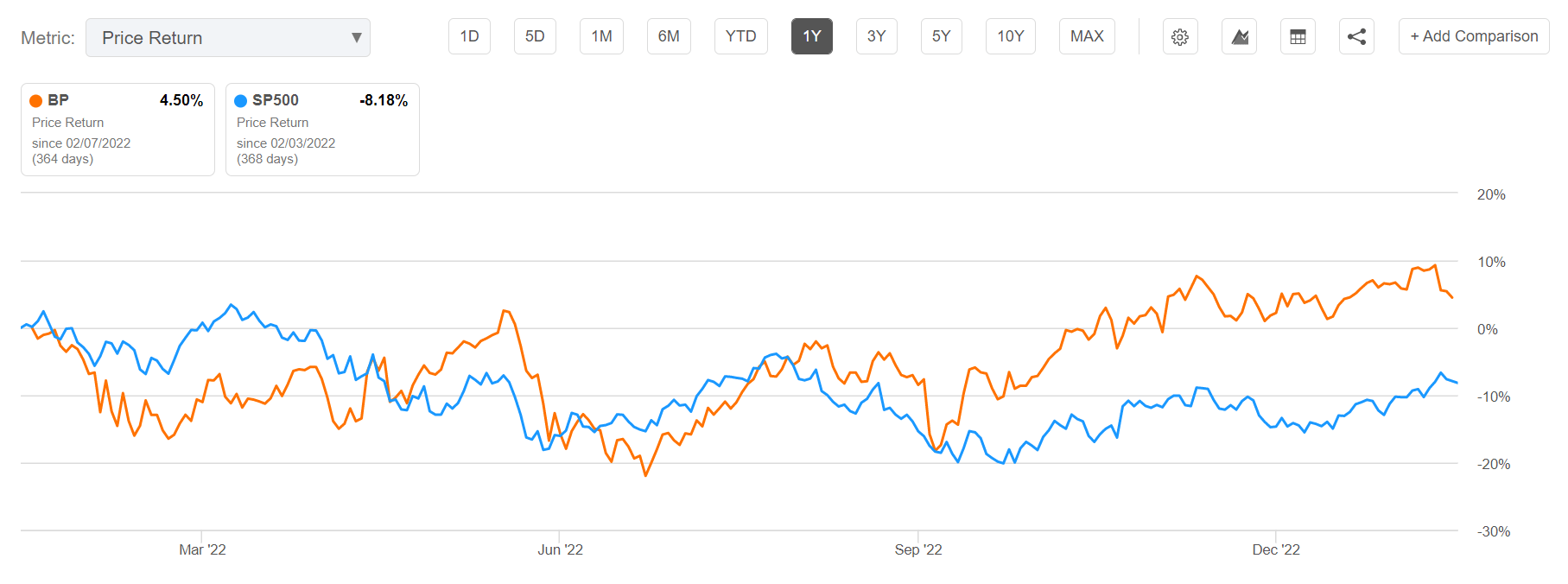

For reference, BP stock continues to outperform the broad market: The oil major’s shares are up approximately 4.5% for the past twelve months, as compared to a loss of about 8% for the S&P 500 (SP500).

Seeking Alpha

Strong Q4 And Record 2022

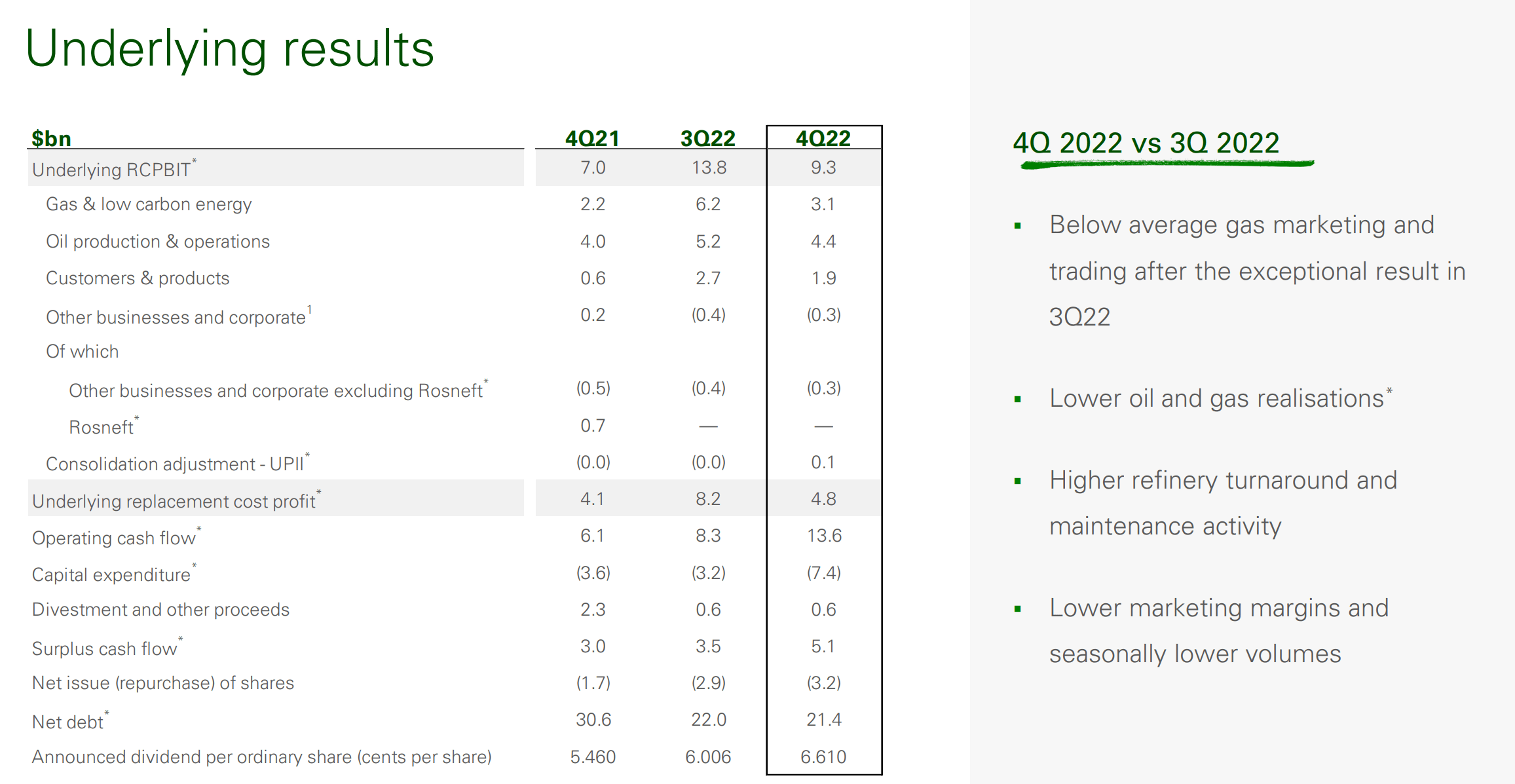

As expected, BP’s delivered a solid performance in the December quarter, despite a challenging macroeconomic backdrop. During the period from September to end of December, BP generated total group revenue of about $69.2 billion, reflecting a topline expansion of approximately 37% as compared to the same period one year earlier, and an expansion of about 26% as compared to Q3 2022. With regards to profitability, BP’s underlying replacement cost profit for the quarter fell to $4.8 billion, as compared to $8.2 billion for the previous quarter — highlighting that the decrease was primarily due to a below-average gas marketing and trading result (but Q3 2022 provides undoubtedly a tough comp).

BP Q4 2022 results

Although BP missed analyst consensus estimates with regards to Q4 profits, $5.11 billion expected, the oil major undoubtedly performed exceptionally well, closing 2022 with another strong quarter.

Closing A Record 2022

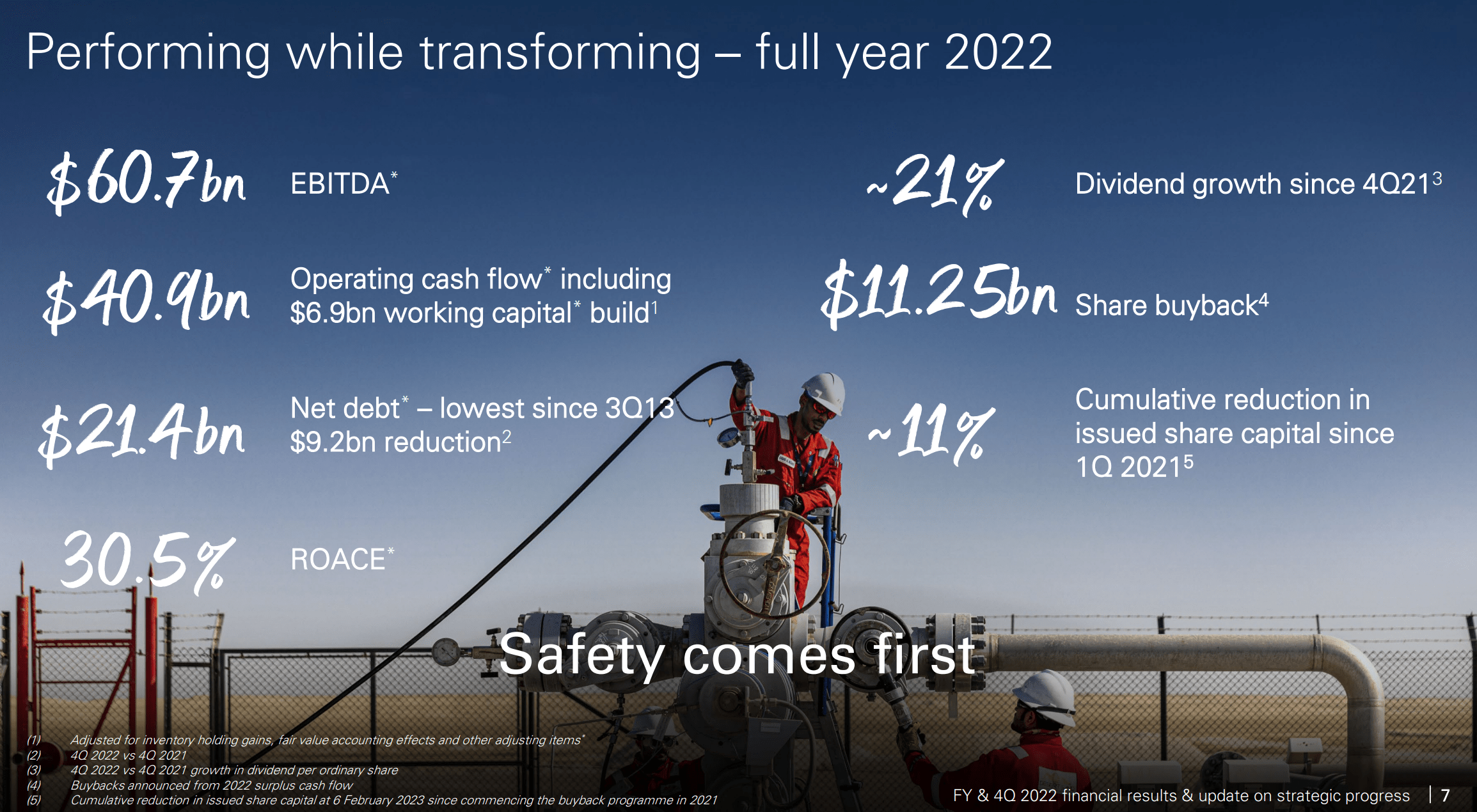

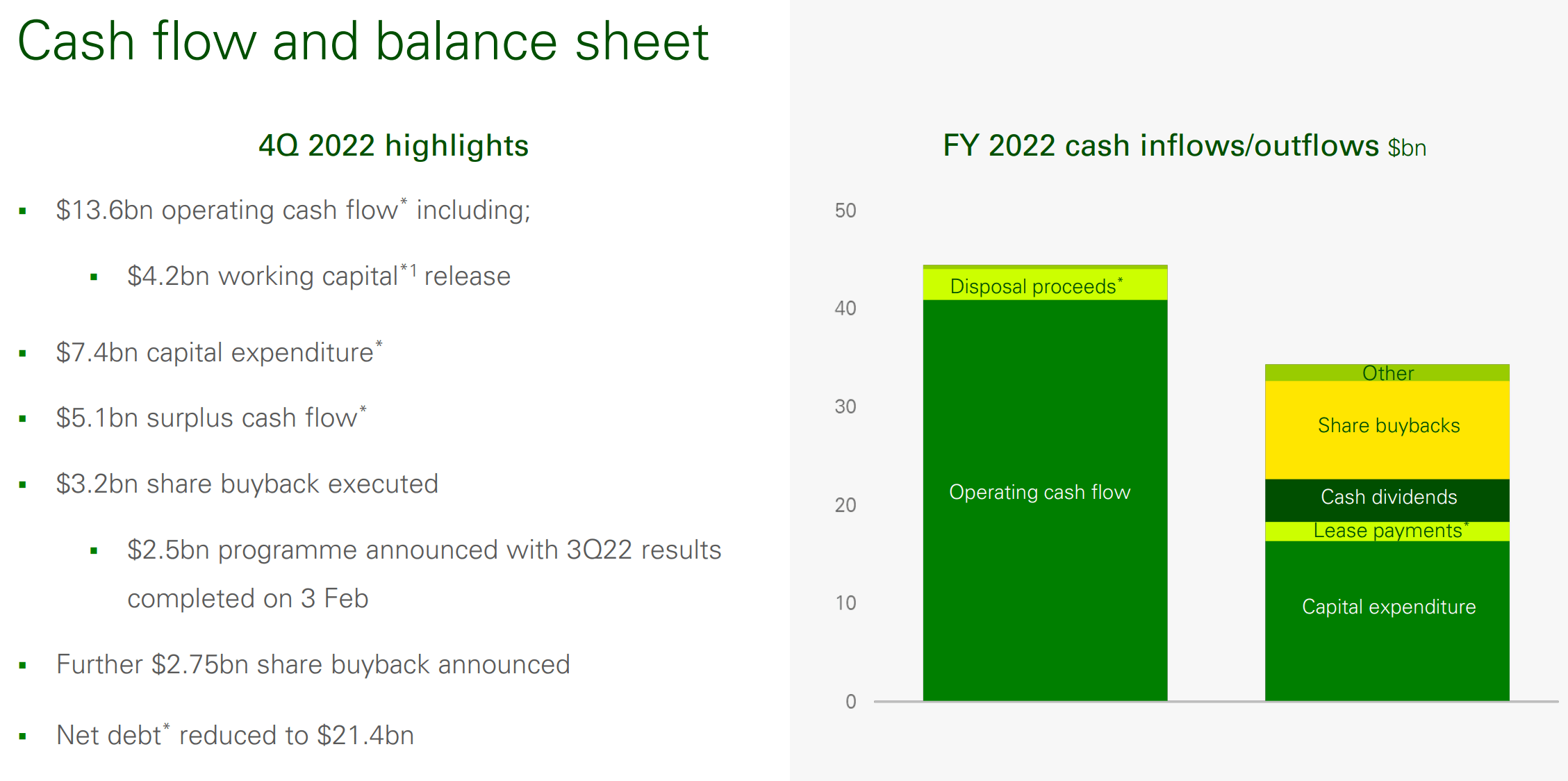

For the FY 2022, the oil major recorded $60.7 billion of EBITDA, $40.9 billion of operating cash flow–despite adding approximately $6.9 billion to working capital– and $27.7 billion of operating profits. Notably, as compared to 2021 ($12.8 billion), profits more than doubled. And BP’s 2022 profit retires the 2008 record of $26.3 billion.

BP Q4 2022 results

BP’s exceptional cash inflow in 2022 enabled management to de-lever the company’s balance sheet while also distributing significant returns to investors- ending FY 2022 with an equity yield of close to 15%. Moreover, on the backdrop of a strong December quarter, BP committed to a 10% increase in dividends and an additional $2.75 billion of buybacks.

BP Q4 2022 results

Positive Outlook Supports Bullish Thesis

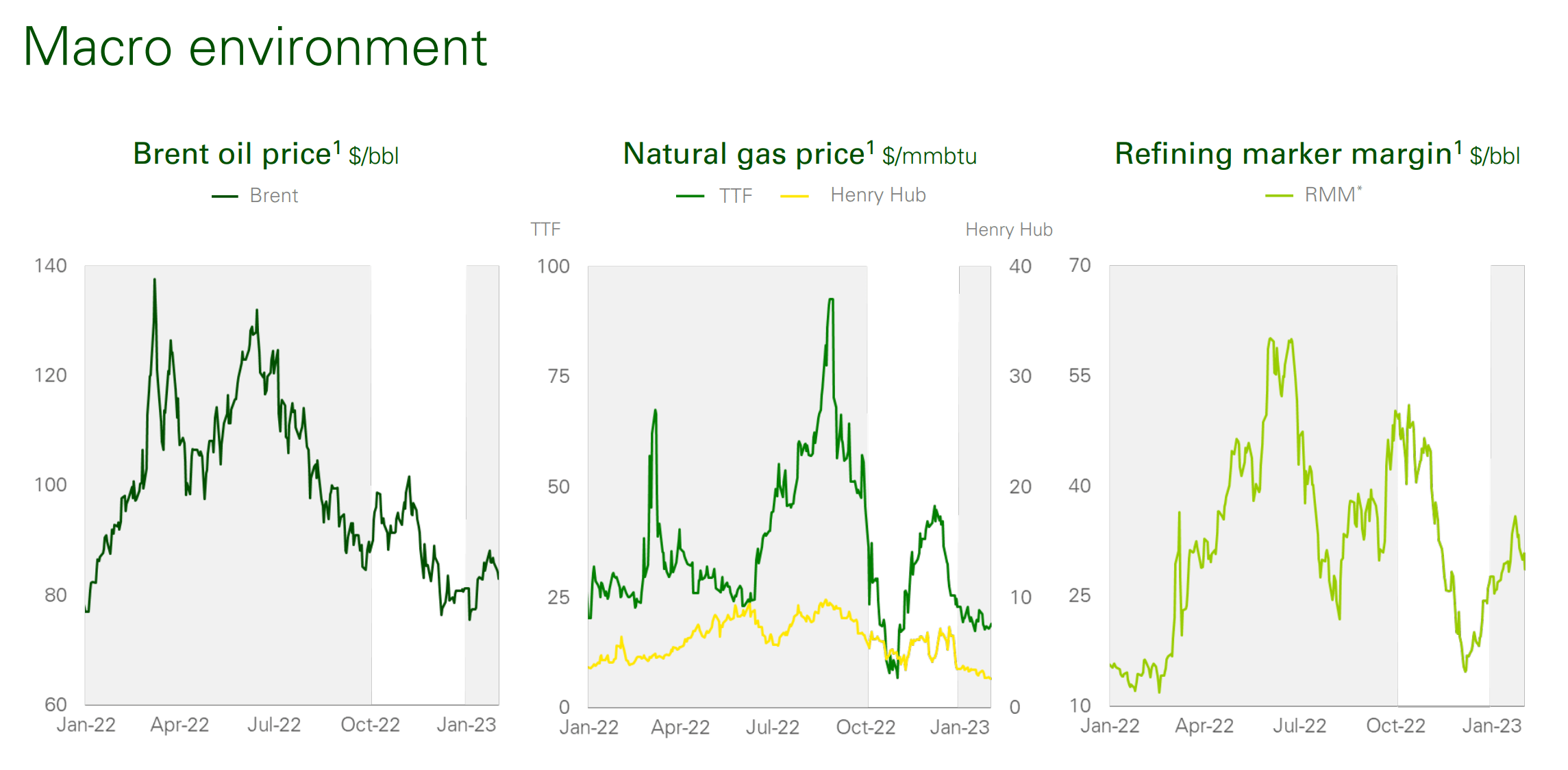

According to management commentary, BP expects oil prices to be supportive in Q1 due to recovering Chinese demand, Russian export uncertainty, and relatively depleted oil inventory levels across the world. Or in other words, investors should consider that the energy market was already tight in 2022, despite the year-long COVID lockdown in China. With China ending COVID restrictions and Europe also recovering, a solid demand recovery is expected in the first half of 2023. And modelling the Brent benchmark in the range of $70 to $80, BP could potentially write $20 to $25 billion of profits in 2023.

BP Q4 2022 results

But even if energy prices would depreciate further, the British oil major would enjoy attractive operating cash flows as long as the brent reference remains above $60/barrel.

Looking ahead, on average, based on BP’s current forecasts, BP continues to expect to have capacity for an annual increase in the dividend per ordinary share of around 4% through 2025 at around $60 per barrel Brent and subject to the board’s discretion each quarter. (Emphasis added.)

And as long as the brent reference remains above $40/barrel, BP would operate cash neutral. According to the release (emphasis added):

[cash neutrality] is underpinned by an average 2021-5 cash balance point of around $40 per barrel Brent, $11 per barrel RMM and $3 per mmBtu Henry Hub (all 2020 real).

Moreover, and perhaps this is a major argument why shares are up sharply following the Q4 reporting, management reduced the firm’s aggressive roadmap to lower oil and gas production by 2039, from 40% to 25%. Although BP’s CEO Bernard Looney announced that the oil major will increase its spending on its “transition” businesses (biofuels, convenience, charging, renewables, and hydrogen) by $8 billion from now until 2030, he also said that the company will aim to increase its oil and gas investments by the same amount, adding that (emphasis added):

It’s clearer than ever after the past three years that the world wants and needs energy that is secure and affordable as well as lower-carbon

Target Price: Raise To $93

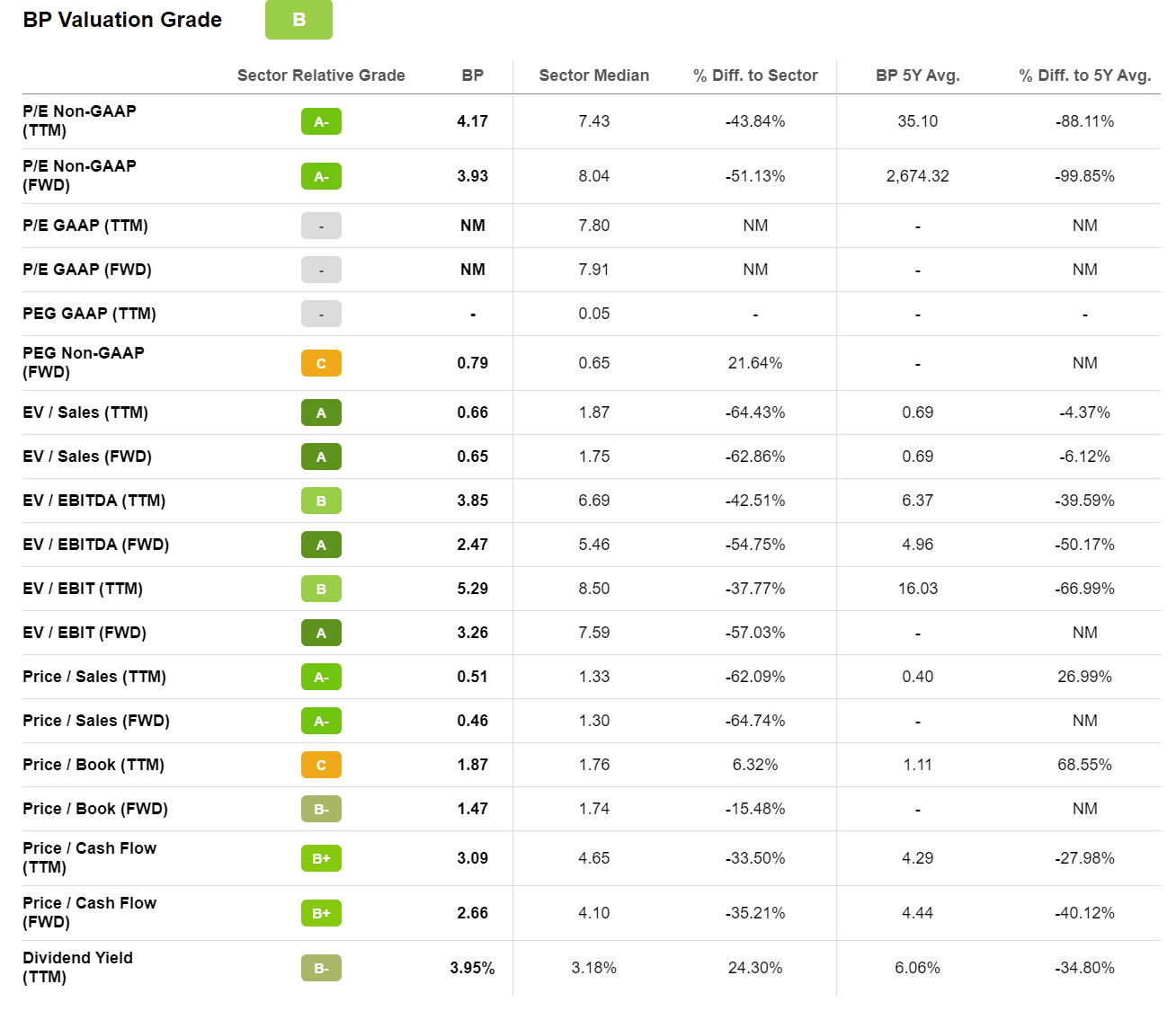

Despite the strong 2022 results, paired with a positive outlook going into 2023, BP continues to trade exceptionally cheap. For reference the Oil Major’s FWD EV/Sales multiple is priced at an x0.7 and the EV/EBIT is priced at x3.3. Notably, these metrics reflect a discount to the comparable industry median of 63% and 57%, respectively.

Seeking Alpha

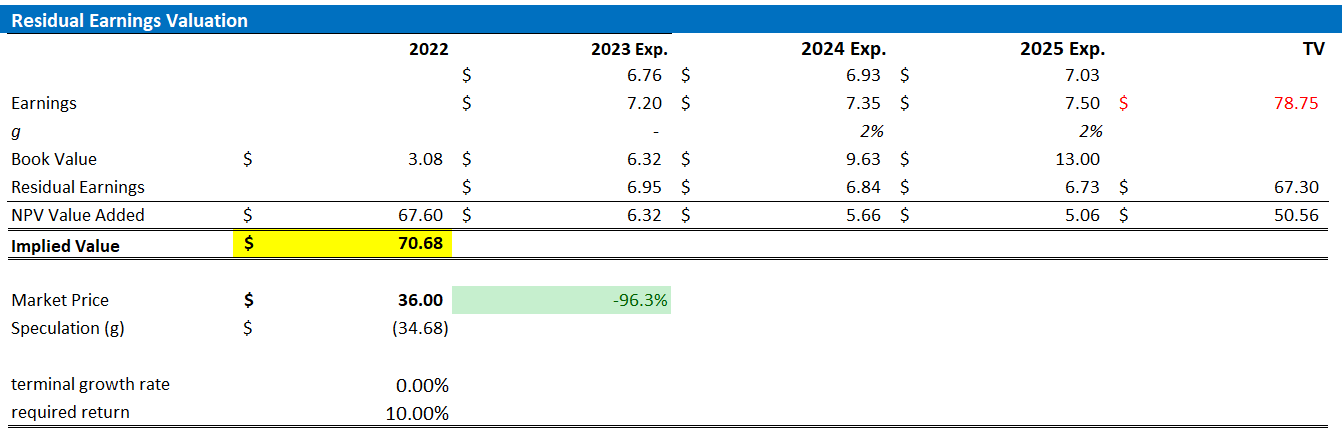

Residual Earnings Model – Update TP To $70.68

Expecting a sharp economic rebound in China, I estimate that BP’s EPS in 2023 will likely fall somewhere between $7.1 to $7.3. Moreover, I also update my EPS expectations for 2024 and 2025, to $7.35 and 7.5, respectively.

I continue to anchor on a 0% terminal growth rate (one percentage point higher than estimated nominal global GDP growth), as well as on a 10% cost of equity.

Given the EPS upgrades as highlighted below, I now calculate a fair implied share price of $70.68 (BP reference).

Author’s Assumptions and Calculations

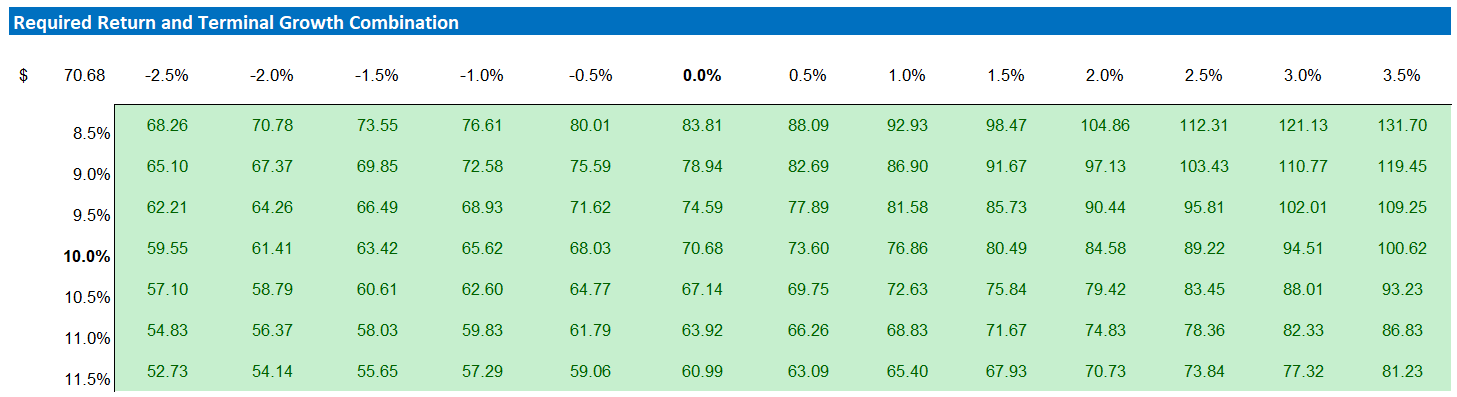

Below is also the updated sensitivity table.

Author’s Assumptions and Calculations

Risks

As I see it, there has been no major risk update since I have last covered BP stock. Thus, I would like to highlight what I have written before:

… investors should note that I assume a sustainable oil price of about $60/barrel. While this might seem bearish for some readers, others might argue that the fair value for oil is much lower.

As the 2020 COVID-19 induced sell-off has shown, oil can even trade at negative price-levels. If oil would break considerably below $60/share and does not recover within a sensible time-period, the bull thesis for BP would break.

Conclusion

BP’s profitability continues to be supported by a strong energy market. And reflecting on the company’s optimistic outlook for 2023, paired with a strong demand tailwind coming from the China COVID reopening, I am confident enough to model strong EPS though 2025. With that frame of reference, BP looks undervalued at an EV/EBIT of about x3.3. Personally, I argue BP stock (BP reference) should trade close to $70/share to be fairly priced. Reiterate “Buy.”

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment