AvigatorPhotographer

Note: I have covered Borr Drilling (NYSE:BORR) previously, so investors should view this as an update to my earlier articles on the company.

Two months ago, junior offshore driller Borr Drilling or “Borr” managed to address most of its long-standing debt and liquidity issues at the price of substantial dilution for common equity holders.

In aggregate, the company raised gross proceeds of $275 million in an underwritten public offering which resulted in outstanding shares increasing by approximately 50% to 229.3 million.

The majority of the funds was used for partial repayments under the company’s numerous debt facilities. In turn, lenders agreed to extend maturities to 2025.

In addition, Borr agreed to sell three jackup rigs currently under construction with Keppel FELS in Singapore for $320 million with the proceeds being used to pay the remaining delivery installments for the rigs. The sale resulted in a $124.4 million impairment charge.

The company also succeeded in selling the warm-stacked jackup rig Gyme for $120 million ahead of the November 15 deadline set in the agreement with creditor PPL Shipyard Pte. Ltd. Singapore (“PPL”). The proceeds will be applied to repay principal, back-end fees and accrued interest for the rig while any excess amounts received by PPL are to be applied to the accrued interest for eight other rigs also financed by PPL.

The Gyme sale will likely result in another $25 million in impairment charges in Q4.

Depending on the company’s cash usage, I would expect Borr to report unrestricted cash and cash equivalents between $80 to $100 million in the upcoming Q3 report, up substantially from $29.7 million at the end of Q2.

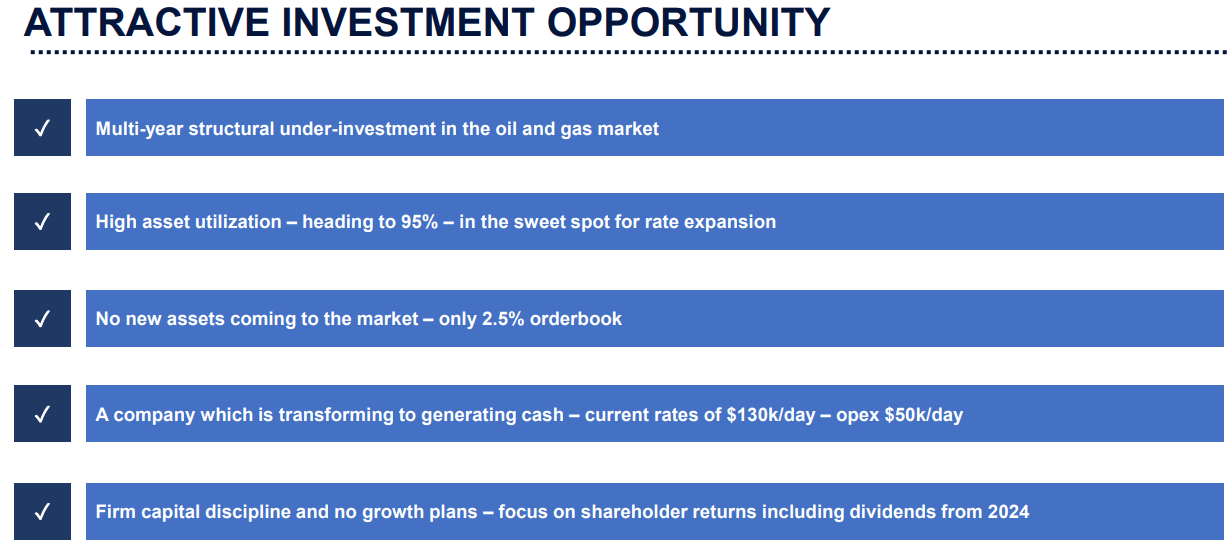

While ongoing rig activation and contract preparation costs are likely to cause some additional cash outflows in H2, the company’s outlook for 2023 presented in the recent Q2 report points to solid cash generation in the not-too-distant future (emphasis added by author):

Based on the conservative market outlook for our available rigs being fixed at current market rates, already contracted revenue, and operating costs, we anticipate generating $290-330 million Adjusted EBITDA in 2023, with an early estimate to double this number again in 2024. Our industry has shown an incredible ability to rebound from an extended downturn. We are now putting the recent challenging periods behind us and entering into a phase which will provide shareholders with the returns they expect, while we maintain our focus on providing customers with assets that are performing safely and with operational excellence.

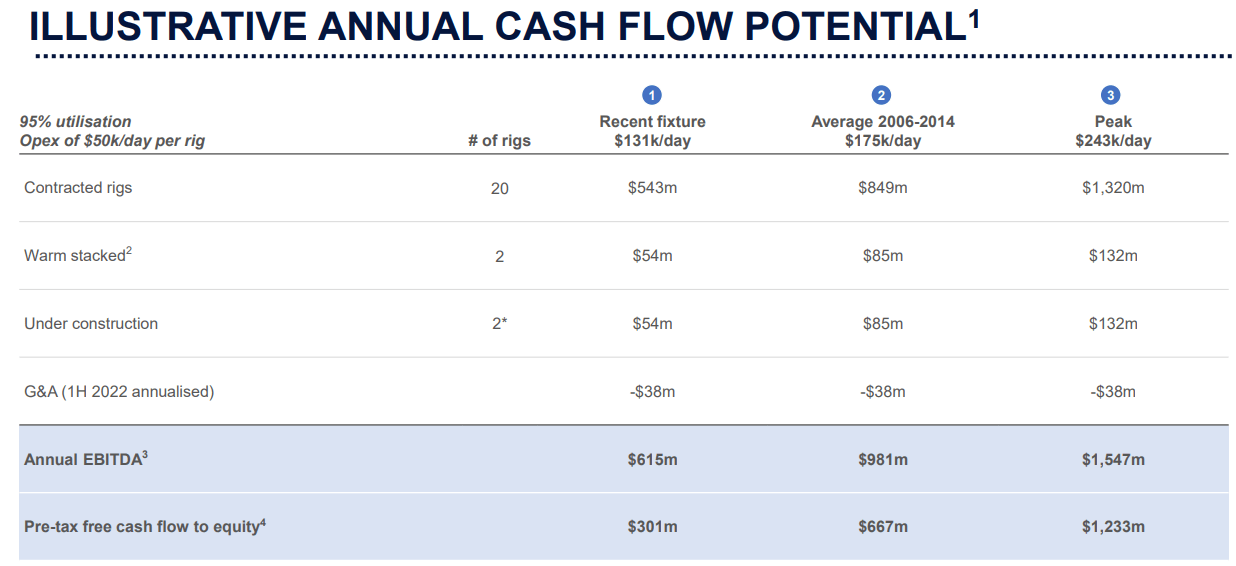

At the EBITDA level projected for 2024, Borr Drilling expects to generate approximately $300 million in pre-tax free cash flow:

Company Presentation

Even better, the company currently expects to reward shareholders with a dividend starting in 2024:

Company Presentation

Unfortunately, Borr Drilling is still required to address $350 million in convertible debt until the end of January:

We have not made any agreement with holders of our convertible bonds due 2023 and we intend to refinance these prior to maturity in May 2023 through a combination of cash flow from operations, asset sales, refinancing or equity. In our agreement with Hayfin and DNB, we undertake to refinance the convertible bonds by the end of January 2023.

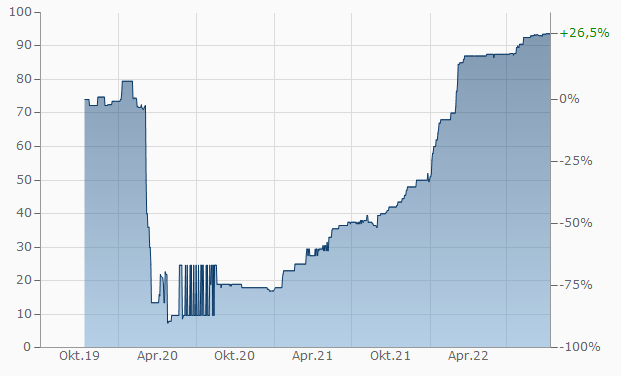

With the bonds currently trading just slightly below face value after dipping below 10% in early 2020, I would expect a successful refinancing rather than additional asset sales or another equity raise.

Finanzen.net

That said, an element of risk apparently remains and more conservative investors would be well-served to remain on the sidelines until the convertible notes have been successfully addressed without additional dilution for common equity holders.

Bottom Line

Borr Drilling appears to be well on its way to successfully address its remaining short-term debt maturities without the need for additional asset sales or shareholder dilution.

Even when assuming no further recovery in the jackup market, the company is likely to generate substantial amounts of free cash flow in 2024, which bodes well for management’s stated intent to initiate a dividend by that time.

Based on the company’s projections for 2024, shares are currently trading at an inexpensive 4x EV/EBITDA. Speculative investors might consider using temporary weakness to build a position.

At this point, I remain positive on the entire industry including leading US exchange-listed players like Seadrill (SDRL), Valaris (VAL), Noble Corp. (NE), Diamond Offshore Drilling (DO), Transocean (RIG), Helix Energy Solutions (HLX) and offshore drilling support providers like Tidewater (TDW) and SEACOR Marine Holdings (SMHI).

Be the first to comment