Thomas Barwick

Company description:

Booking Holdings Inc. (NASDAQ:BKNG) is one of the largest international online travel providers, supporting consumers in over 220 countries.

The Group trades through six main brands:

- Priceline – offering several services, such as Hotel, flights and rentals. Targeting the USA and discount shoppers. This is the first trading business of the Group.

- Booking.com – offering several services, such as Hotel, flights and rentals. Targeting predominantly Western nations. Booking.com was acquired in 2005.

- Agoda – offering several services, such as Hotel, flights and rentals. Targeting predominantly Asian nations. Agoda was acquired in 2007.

- KAYAK – Similar to Booking.com but specializes in price comparison, was acquired in 2015.

- Rentalcars.com – Specializing in vehicle rentals across Western nations.

- OpenTable – Offering restaurant table bookings in Western nations. OpenTable was acquired in 2014.

All acquisition occurred several years ago and have been integrated successfully. Interestingly, although they operate in the same / similar markets, BKNG has done well to separate them slightly, thus making incremental gains rather than cannibalizing sales.

BKNG has had an eventful few years, with COVID-19 bringing all businesses to a standstill. Subsequently, they have ridden the volatility of lockdowns and restrictions ending.

With COVID-19 finally behind us (at least outside of China at the time of writing), now is a good time to assess the attractiveness of BKNG. We will look at the macro-economic factors which are dominating the headlines, BKNG’s financial performance and how BKNG stands in the travel and hospitality industry, relative to other companies.

Travel and hospitality:

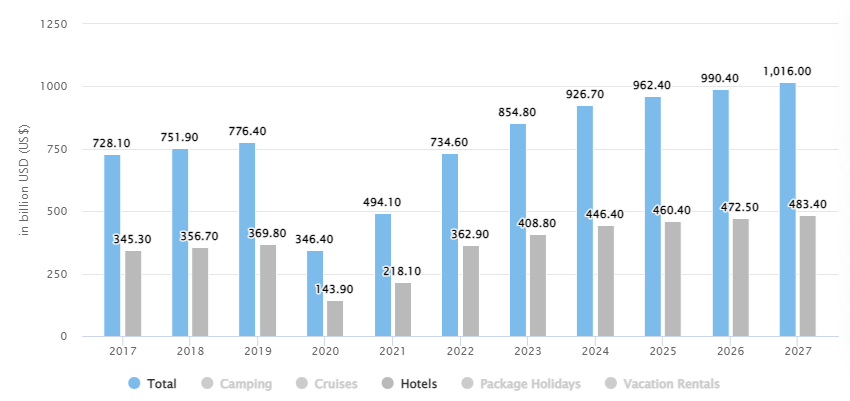

As we mentioned previously, the travel and hospitality industry has been heavily disrupted in the last few years. Patrick Andersen, CWT Chief Executive Officer, said “Demand for business travel and meetings is back with a vengeance, of that there is absolutely no doubt”. The recovery has been strong, reaching levels similar to 2019. Growth is expected to be moderate going forward, in the mid-single digits. This is in line with the years prior to 2019.

Revenue – Travel and Tourism (Statista)

Interestingly, 74% of total revenue is expected to be generated through online sales. This is because consumers are increasingly looking for ease of booking and optionality, as opposed to speaking to travel agents. This has been a contributing factor to BKNG’s growth, who has utilized their technical capabilities to make comparing and booking hotels / flights very easy.

PwC believes the recovery may stall in 2023, however. The reason for this is slowing growth, especially in regional locations outside of major cities, such as London. Slowing growth usually has a negative impact on tourism as discretionary income falls and consumers focus on necessities.

Furthermore, we are seeing substantial price increases across the travel industry in recent years. Air fares are expected to rise 48.5% in 2022 and hotels at 18.5%.

There are multiple reasons for this, firstly inflation has caused rising prices of input costs, such as fuel and other commodities. These costs are being passed on directly to consumers and in many cases at a mark-up. Further, due to said inflation, wages have been forced upwards, inadvertently also causing a labor shortage as employees move to higher paid jobs. The net impact on BKNG is difficult to predict, rising prices are good because they make a greater amount per booking but as travel is elastic in demand, the quantity of bookings will fall. In 2022, the net impact has been positive as the business has grown but we are in a cost-of-living crisis and people can only bare the price increases (which are expected in the high single digits in 2023) for so long.

Economic conditions:

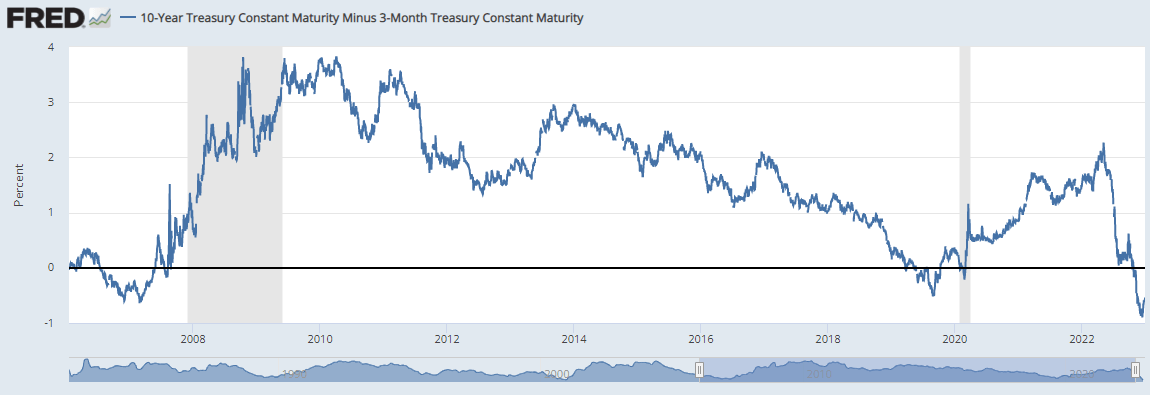

As we have touched on previously, we are currently experiencing a cost-of-living crisis in many western nations. Inflation is >5% and interest rates are rising in response. This is noticeably reducing consumers’ discretionary income and causing businesses to cut unnecessarily expenditure, such as travel. Central bankers are failing in the balancing act of bringing down inflation without causing a recession. GDP is near zero in the UK and things do not look much better in the rest of Europe. Looking at the 10Y / 3M yield curve, we observe an inversion for the first time, and to a level exceeding 2008. For this reason, pricing in a recession seems like a prudent decision.

10Y / 3M yield curve (FRED)

Should a recession occur, it is expected that travel will slow in 2023, until expansionary policy can be initiated once again. This is serious headwinds for BKNG as bookings may fall, with greater pressure to be price competitive as consumers become more price conscious.

Financials:

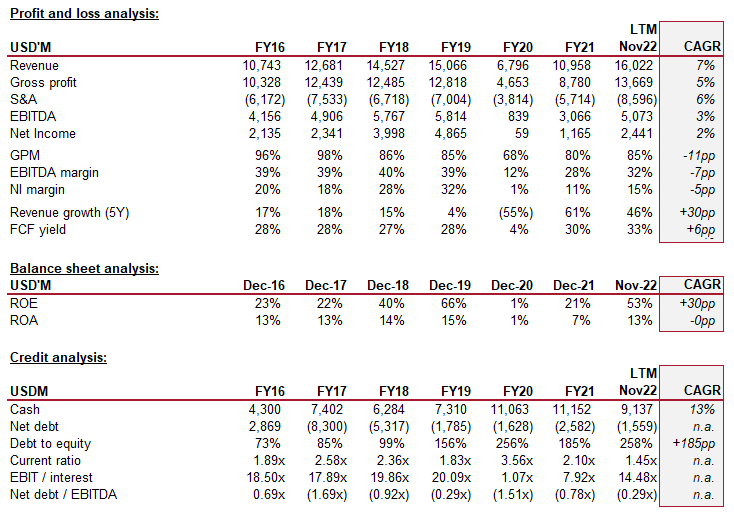

BKNG – Financial analysis (Tikr Terminal)

BKNG has performed very respectively over the historical period, achieving revenue growth at a CAGR of 7%, which factors in a large dip during COVID-19 (CAGR between FY16 and FY19 was 12%). BKNG has managed to achieve growth in excess of the travel market due to a superior offering and successful marketing. Booking.com for example is likely the leading online agency in Europe for hotels, with Agoda the same for Asia. Agoda was responsible for all bookings to Thailand when tourism first opened, given its size in the region. Bookings across the board are up and in the high double digits.

BKNG – Bookings (BKNG – Q3 Quarterly report)

What may be slightly concerning is the dip in Q3 2022, which has historically been a quarter for growth. This could be early signs of growth slowing, although it has yet to be seen if this will continue and to what levels it may fall.

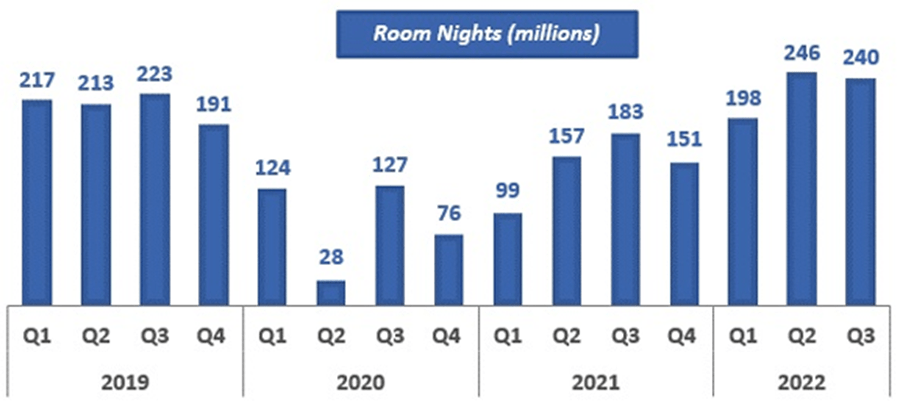

BKNG – Room nights (BKNG – Q3 Quarterly report)

Revenue is split between two main streams, Agency and Merchant fees, with Advertising relating to OpenTable and KAYAK referrals. Merchant revenues are derived from travel-related transactions where BKNG does facilitate payments from travelers for the services provided. This stream is more lucrative as BKNG can earn additional fees such as payment facilitating fees and insurance. Growth in the 9M Sept22 period has been impressive, at a rate of over 100%.

BKNG – Revenue split (BKNG Quarterly report)

Unfortunately, things look less good the further down we look. EBITDA margin has fallen 7% and NI margin 5% between FY16 and LTM Nov22. This suggests operations are becoming less efficient in order to achieve growth.

Interestingly, Marketing expenditure has remained fairly flat across the current period, representing a similar % to revenue when compared to 2021.

BKNG – Marketing expenses (Q3 Quarterly investor pack)

The increase in costs has thus come from “sales and other expenses”. This includes items such as, credit card fees, call centre and website fees, credit loss provisions and other tangential services. This is likely as a result of inflationary pressures which cannot be passed on to customers.

Sales and other expenses (Q3 Quarterly investor pack)

From a balance sheet perspective, BKNG did well to shore up its financial position and so was not material impacted by COVID-19. Debt was raised in order to support any liquidity needs but on a net debt basis, BKNG continues to maintain a strong cash balance. BKNG has aggressively repurchased shares in recent years (lifting ROE and reducing D/E artificially), while paying down substantially less debt. As prudent investors, we would like to see this flipped in the coming years with interest payments creeping up. Regardless, at this current juncture, the company has healthy coverage over interest payments and operates with a healthy working capital position.

What may pique investor interest is BKNG’s long-term investments. BKNG currently holds over $2.6BN in equities (valued at almost $4BN at Dec21). This includes investments in 3 main companies:

- Meituan – E-commerce platform in China ($136BN market cap)

- DiDi Global – Ride sharing business in China ($15BN market cap)

- Grab Holdings – E-commerce “super-app” in Asia ($12BN market cap)

All 3 companies are very highly rated and are commonplace in their various countries. Problematically, Asian stocks have performed poorly on top of general market weakness, with Chinese stocks coming under fire due to the risk of delisting and new legislation. These stocks will likely need to be held for many years but could easily become over 10% of market cap, given the potential for growth.

BKNG’s financial profile is very good in our view, Management have done well to grow the business in an accretive manner while maintain a healthy balance sheet. The most impressive aspect is their continued revenue growth at levels one would not expect from a mature, highly competitive market. This is a testament to the quality of their product and investment in effective marketing.

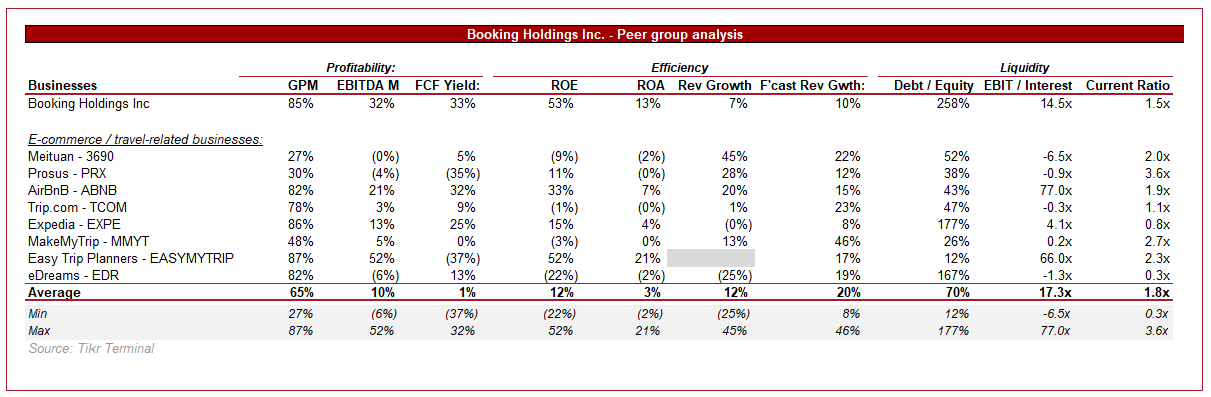

Peer comparison:

Peer group analysis (Tikr Terminal)

BKNG stacks up well against a peer group of e-commerce businesses and online travel agencies. It is more profitable on both a GPM level and FCF. In many cases, BKNG is further along the life cycle when compared head-to-head, which explains the bottom-line outperformance. However, even when we look at revenue growth, BKNG has done well. The peer group has grown at an average of 12%, only marginally ahead of BKNG at 7%.

Going forward, BKNG is forecast to grow revenue at 10%, which on an absolute basis is very good, although is a relative underperformance. That said, BKNG does well against an equally mature Expedia (EXPE) and will make up for its lower growth in relative profitability.

The only business which wholly outperforms BKNG is Airbnb (ABNB), but we must consider the valuation of businesses in conjunction with their performance.

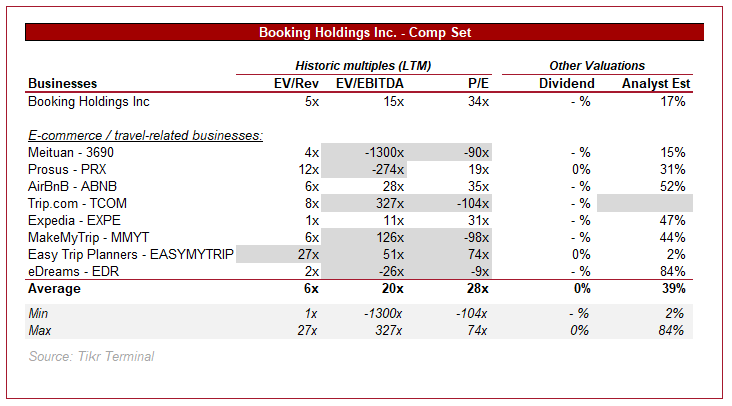

Valuation:

Peer group valuation (Tikr Terminal)

When looking at the valuation of these peers, it is very messy. Many of the businesses are loss-making or are trading at a large valuation. These valuations come from investors hoping for high growth continuing when the businesses move towards maturity and profitability.

We should note that BKNG’s P/E ratio is abnormally high, this is due to the loss on investments held at fair value mentioned previously. As this is a non-trading expense, we propose exclusion of this for comparisons purposes. This brings the multiple down to 17.6x.

Revenue multiples may be quite useful to observe given the outliers. BKNG is valued in line with its peers yet is profitable. Given its profitability, we believe BKNG’s revenue to be “worth” more, as every $ more translates into profits to shareholders. For this reason, BKNG is certainly well priced relative to its peers.

Further, BKNG has traded at an average of c.18-20x LTM EBITDA historically. This suggests that economic conditions may be priced in, as growth and profitability remain strong.

Expedia is slightly cheaper, but investors trade slightly lower growth and profitability for this discount. Although we have not investigated Expedia in detail, this is an option for investors who believe forecast growth can be exceeded.

Airbnb is a much younger and faster growing business, with a valuation to reflect this. This is a business we intend to cover in the future and provides investors with a greater risk / reward appetite exposure to the industry.

Conclusion:

When we first started researching BKNG, we were surprised by the quality of the business. It is growing at a respectable rate and is very profitable. The balance sheet was not destroyed by COVID-19 and investors can gain exposure to high-growth businesses through its investments. The future should hold continued buy backs and reliable sustainable growth.

The biggest risk we see is in a deterioration of macro conditions. A recession would lead to reduced travel and greater competition for a smaller pie. Although BKNG is down c.23% from its ATM, it could certainly fall further. This said, attempting to time an investment perfectly is folly. For this reason, those considering investing would do well to average in progressively over the coming 6-12 months.

Be the first to comment