Wolterk

When we last covered The Boeing Company (NYSE:BA), we saw a possibility of a cascading sell-off, which would result in a buy opportunity below $100. While we did upgrade it from our previous “Strong Sell” rating, we felt the valuation needed to get more compelling.

So the price today reflects an avalanche of hot money chasing the defense sector. Imagine that. Still, the fundamentals suggest that some bad news is being priced in and we are ready to move to the sidelines. We upgrade this to a Hold/Neutral rating and will look to get long should the stock really move into the deep value zone. That would be below $100/share for us.

Source: Boeing Bulls Capitulate, Look To Buy This Below $100

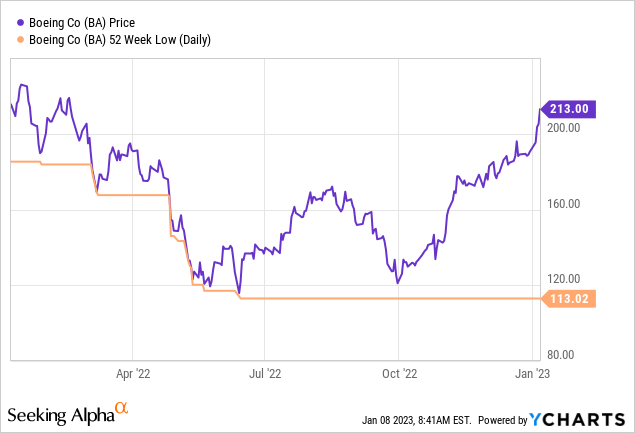

Boeing came close but never got into the two-digit price territory.

To add insult to injury, the stock has soared since then after missing our point by $13 dollars. We look at where things stand today and update our rating.

Q3-2022

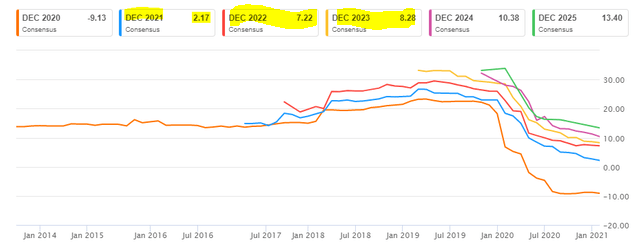

Anyone looking for an explanation of the rally in the last released results, had to use a lot of imagination to do so. Q3-2022 non-GAAP loss was $6.18 and revenues missed by almost $2.0 billion. This was by far the worst quarter of 2022 and total losses for the 9 months exceeded $9.00 per share. Before we proceed with other segments, it is always a good idea to examine the perennial optimism of analysts. We pointed this out in our January 2021 article, where we heavily panned the idea that Boeing would show positive earnings per share any time soon.

Earnings Estimates From January 2021

Not only did Boeing miss the 2022 numbers, it missed them by a mile. We are on course to have $9.00 losses per share for the year, and that is $16 off the mark from 2 years ago.

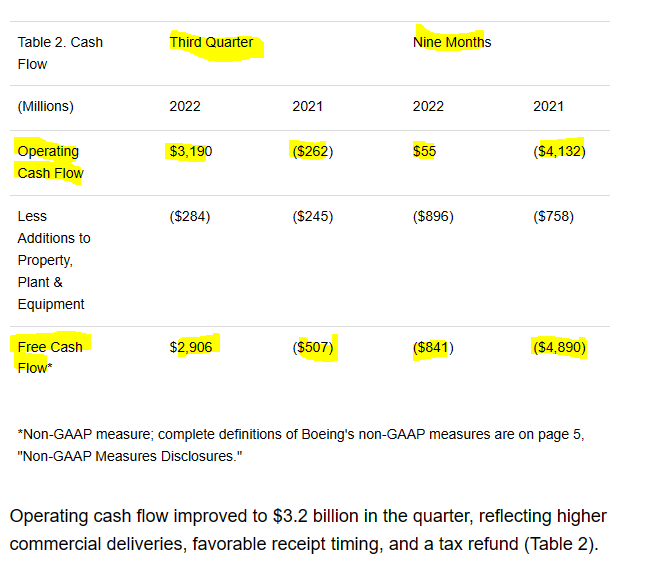

If there was one solace here for the bulls, it was that Boeing had stopped hemorrhaging cash. Despite losses, operating cash flow has pleasantly surprised in 2022. These are good numbers and certainly a relief here for bulls who had gotten used to seeing a massive burn rate quarter after quarter in 2021.

Source Boeing Q3-2022 Press Release

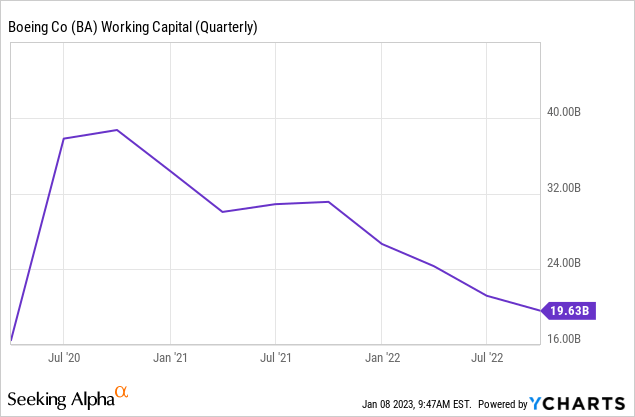

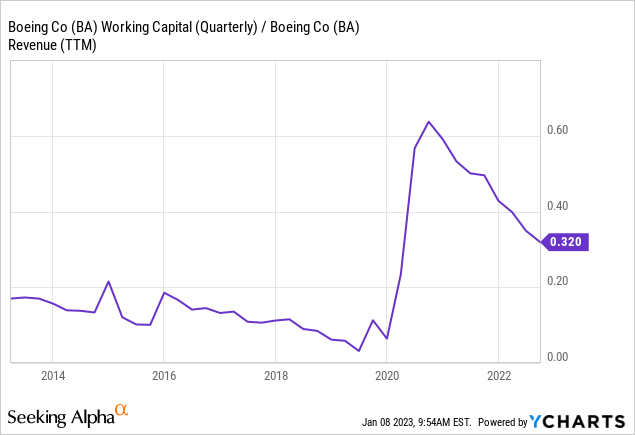

Where did that cash flow come from, though? There are a couple of ways to look at it. The first being what the company mentions, just below the figure. All 3 of those factors, obviously, added to cash flow. But at a broader level, we can see Boeing tightening its working capital usage to liberate cash flow. Working capital (current assets minus current liabilities) has dropped from almost $40 billion in Q3-2020 to under $20 billion today. This included a $1.5 billion drop from Q2-2022 to Q3-2022.

We are likely getting close to how low Boeing can get this number. Assuming historical correlation holds, we can see perhaps a $12-15 billion as the lower limit in 2023 (based $82 billion in sales).

Outlook

With an expected small amount of liberated cash flow from working capital, Boeing’s free cash flow will trend more or less in line with its adjusted earnings. Here, the outlook is not exactly stellar, whether you look at one or two years.

Seeking Alpha

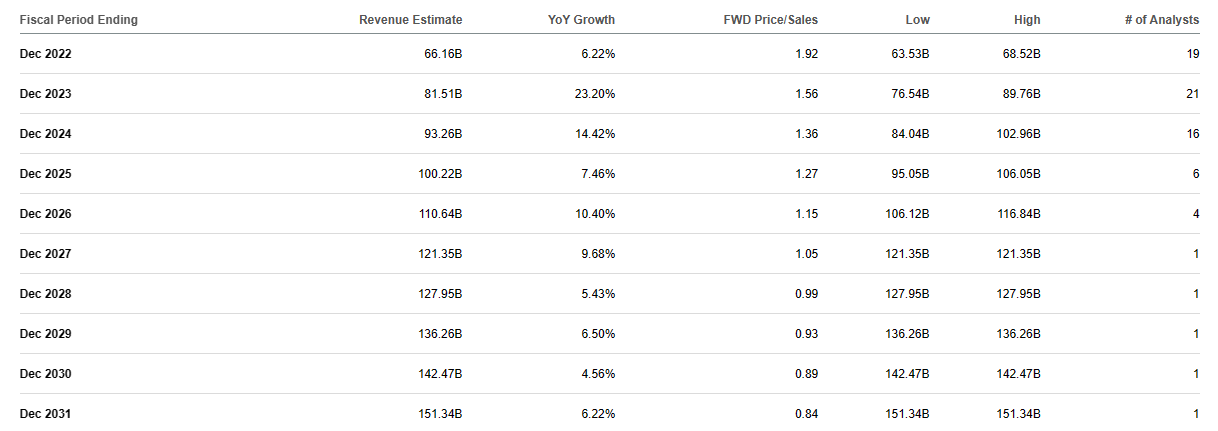

Boeing is trading at over 32X 2024 expected profits. We have to balance that in light of the fact that analysts continue to be hopelessly offside of how bad the numbers have actually been. Bulls will likely argue that the analysts are overly pessimistic at this point. That can certainly happen at economic turns, but in this particular case, we see no evidence for it. Here is exhibit A supporting our theory.

Seeking Alpha

The scramble continues to be to lower earnings estimates to get them where they need to be, rather than the other way around. We are also very close to recessionary readings on multiple fronts, including based on Leading Economic Indicators and ISM readings. This late in the cycle, earnings surprises tend to be predominantly on the downside.

Valuation & Verdict

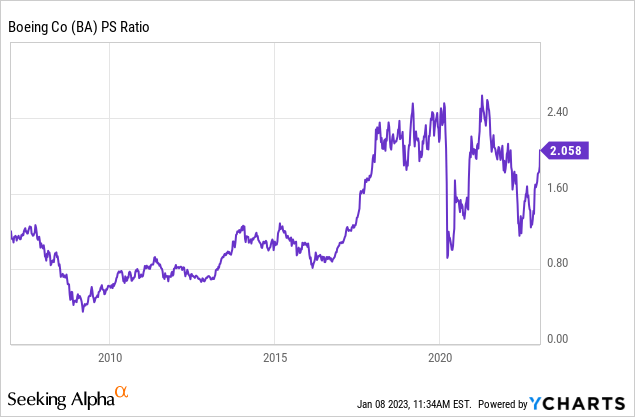

Besides the obvious lack of current profits and the expensive numbers all the way out to the end of 2024, Boeing is not cheap even on a price-to-sales metric.

Trough numbers are likely to be closer to 0.8X, and we are nowhere near that. Even using 2024 sales estimates, we are not in the ballpark.

Seeking Alpha

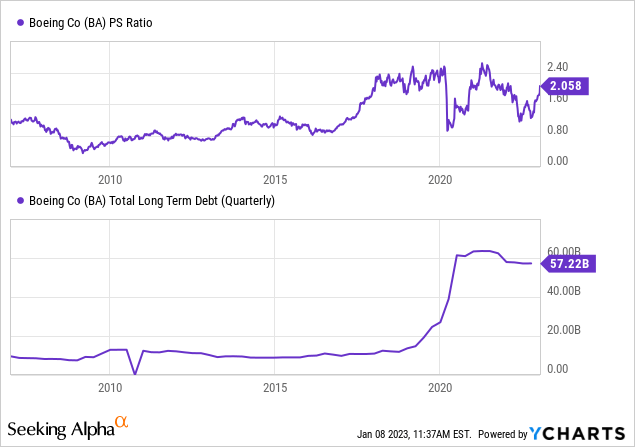

One other aspect here is that the 0.8X price-to-sales ratio was reached even when Boeing carried very little net debt. Compare that to the situation today.

Finally, we will add that 0.8X numbers were hit with 0% interest rates. In all likelihood, we will go lower in this interest rate environment.

As much as we would love to buy the euphoria for this American Icon, we see the stock as fairly expensive by every single measure. Bulls are likely piling on technical breakouts, coupled with expectations for commercial and defense cycles kicking in at the same time. We see that optimism as misplaced and see 0% returns over the next 5 years as the best outcome from this price point. A share issuance to reduce debt levels should not be ruled out here either. We rate the shares as a Sell and think $150 is far more likely to $250 over the course of 2023.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Be the first to comment