nycshooter

Shares of The Boeing Company (NYSE:BA) picked up further momentum in the first few days of 2023 and broke out above $200. The aircraft manufacturer benefits from improving sentiment after United Airlines placed a large order for Boeing’s 787 Dreamliners and 737 MAXs in December 2022 and investors are expecting a continual turnaround in air travel. The United Airlines deal was an important catalyst for Boing after the company suffered for years from a COVID-19 induced down-turn in passenger travel as well as the 737 Max disaster which caused aviation regulators to ground the plane. After a near-20% return since I last covered Boeing here on Seeking Alpha, I believe investors may want to sell at least a part of their Boeing holding into the strength!

Recent aircraft orders lead to upside breakout for Boeing

I wrote about Boeing in the first week of December 2022 — Boeing: Turnaround Time — and I specifically highlighted the accelerating momentum in the commercial aircraft division in a post-COVID world as a strong reason to buy shares of Boeing. Since December 5, 2022, the share price of Boeing has increased by about 17%.

A key reason for improving investor sentiment was the placing of a large order by United Airlines. In December, United Airlines placed an order for 100 787-Dreamliners and 100 737-MAXs in a deal worth $43B with Boeing as the airline seeks to upgrade its aging fleet and has laid out plans to invest more heavily into energy-efficient planes. United Airlines’ record order also signaled confidence in the post-COVID recovery potential of long-haul travel… which also boosted the long-term prospects of Boeing’s commercial aircraft division.

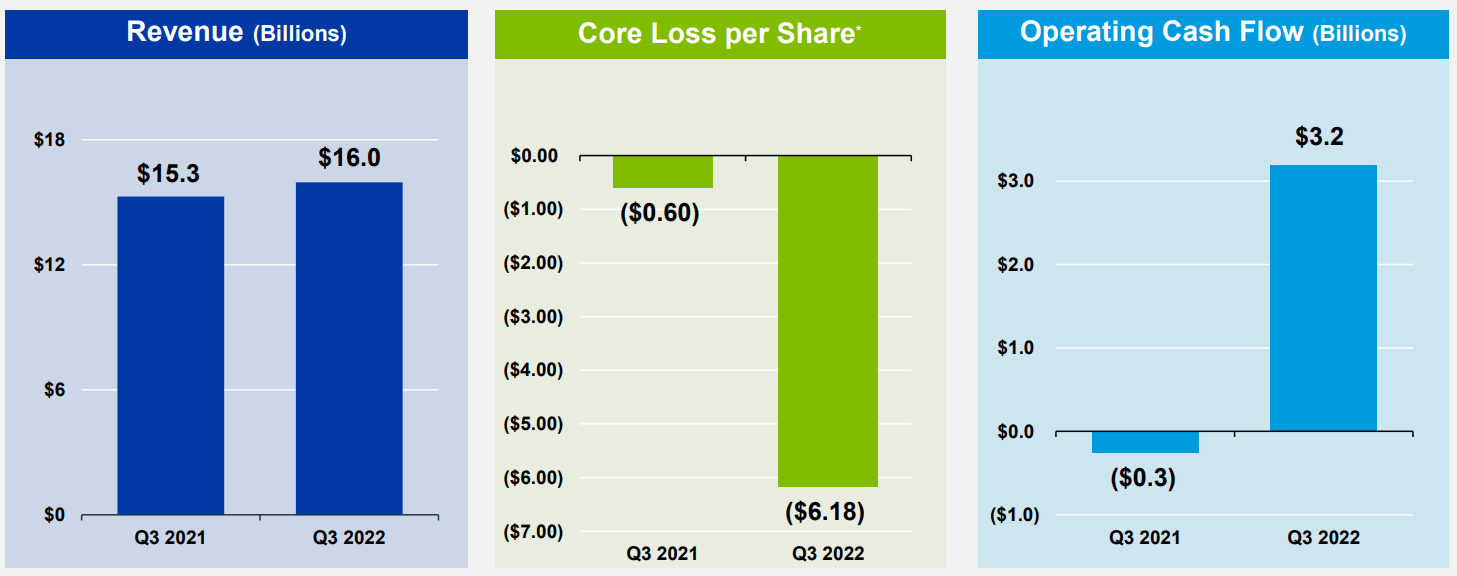

The UAL order was the first major aircraft order for Boeing in years. Boeing is looking back at nearly three years of disappointing company performance and major losses which were driven by a collapse in airline travel at the onset of COVID-19 as well as 737 Max airplane crashes that caused a confidence crisis in the market and at Boeing. More recently, Boeing reported a large Q3’22 loss of $6.18 per-share due to losses on fixed-price defense development programs and higher costs.

Source: Boeing

At the end of December, Boeing also announced the order of 40 737 MAXs by aircraft lessor BOC Aviation Limited. Since the end of FY 2020, Boeing has amassed more than 1,500 737 MAX orders and the momentum clearly points in the right direction for Boeing.

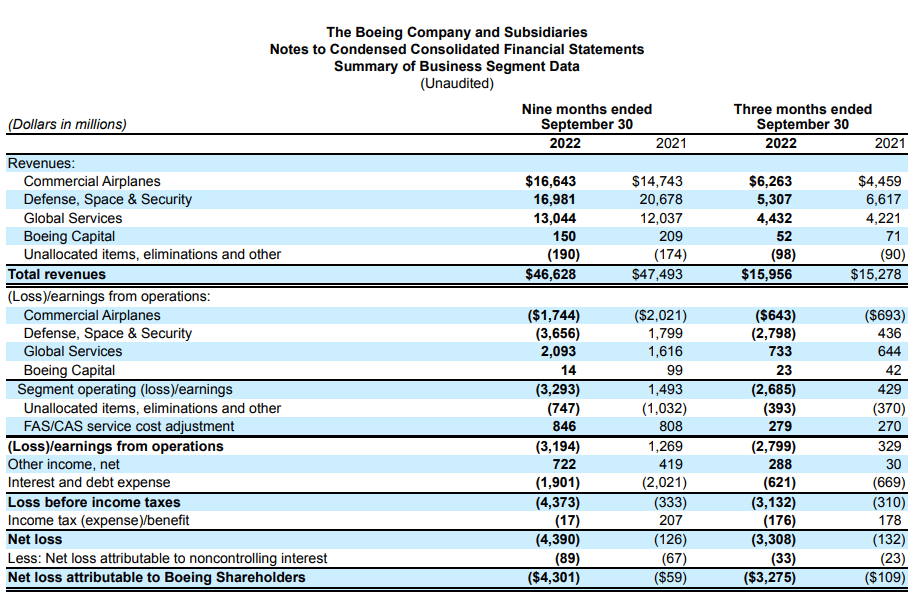

Boeing’s commercial aircraft division is the second-largest business for the company regarding revenue contribution, after Defense, Space & Security which is Boeing’s government business. Still, Boeing’s commercial aircraft business did not turn an operating profit in the first nine months of FY 2022 as the company continues to struggle with delays in deliveries and high costs. Recent airplane orders from UAL and BOC Aviation improve the longer term prospects for Boeing’s commercial aircraft business and I believe the airplane manufacturer could see an operating profit in this segment in FY 2023.

Source: Boeing

Higher P/S ratio, Boeing is overbought

While the UAL aircraft order especially helped create excitement around Boeing’s shares, I believe investors are faced with a good opportunity here to sell into the strength.

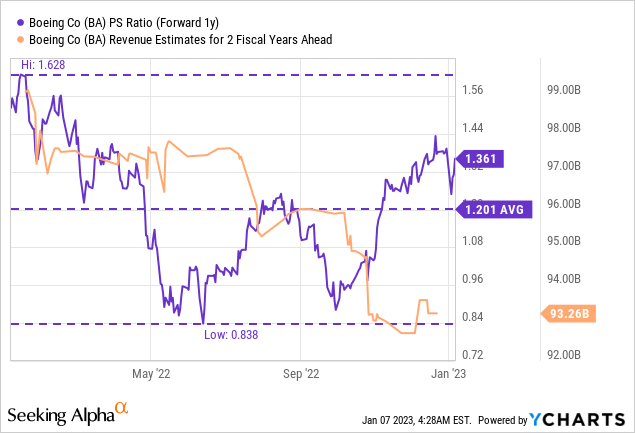

Boeing is expected to generate $93.3B in revenues in FY 2024 which implies a year over year top line growth rate of 14.4 %. The aircraft manufacturer currently trades at a P/S ratio of 1.36 X… which is above Boeing’s 1-year average P/S ratio of 1.2 X.

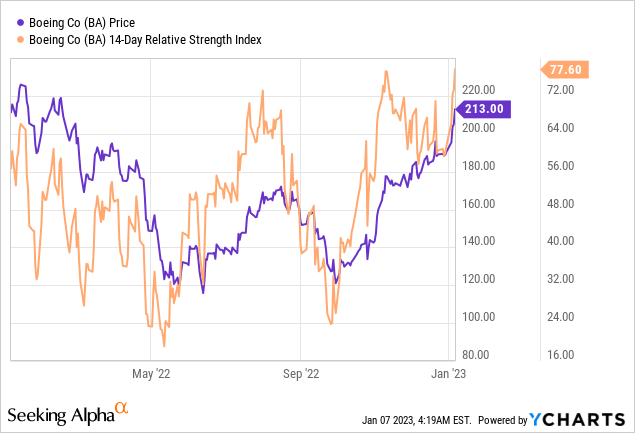

Additionally, Boeing is now overbought based off of the RSI which indicates a growing risk that investors could lose recent gains if Boeing’s shares consolidate.

Risks with Boeing

The air travel industry is volatile and unpredictable and so is the profit potential of Boeing’s second-largest business, the commercial aircraft manufacturing segment. New pandemics or a major air travel disaster also have the potential to cause passenger attitudes toward air travel to change again. I believe the biggest commercial risk for Boeing is a new pandemic or a recession which could dampen passenger travel just at a time when it is set to return to pre-COVID levels.

Final thoughts

I like Boeing and the company’s recovery potential after the entire industry has been decimated by COVID-19 in the last three years. However, after booking a nearly 20% gain in just one month and considering that Boeing’s shares are now heavily overbought, I believe investors may want to consider selling into the strength and taking some profits here. While shares of Boeing are not necessarily expensive with a P/S ratio of 1.36 X, I believe the risk profile is now much less rewarding than it was back in December. For those reasons, I have sold my shares in Boeing and will now sit on the sidelines until a new engagement opportunity presents itself!

Be the first to comment