Stephen Brashear

Boeing (NYSE:BA) reported second quarter earnings before the opening bell on Wednesday, the 27th of July. Post earnings, shares traded roughly flat and maybe there’s good reason for that as I discuss in this report analyzing the segment results.

Mixed results across Boeing segments

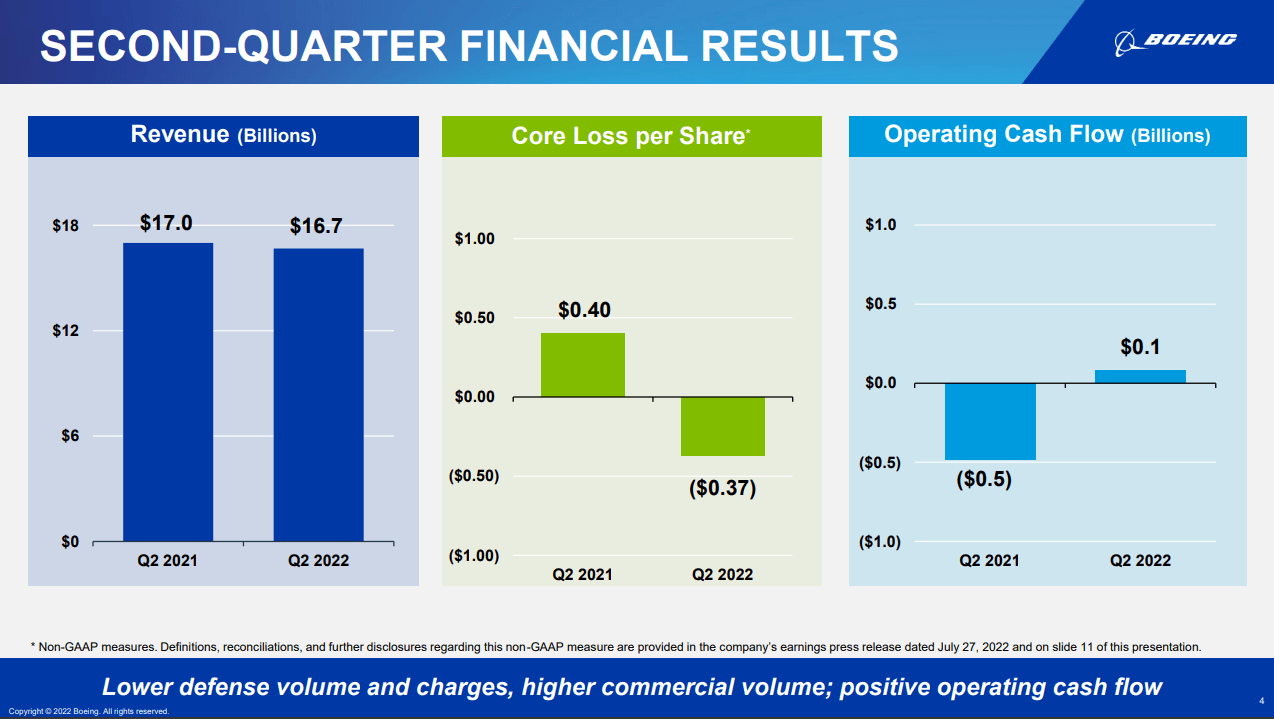

Overview Q2 2022 results (Boeing)

So, the first thing we’re having a look at is the global overview. That the results are mixed already shows from this slide. Boeing reported revenues of $16.7 billion, down from $17 billion in the same quarter last year, missing analyst estimates by $830 million. Earnings per share were -$0.37 compared to $0.40 last year missing the estimates by $0.27 million. Those two elements provide two global negatives in Boeing’s earnings. The slightly positive element was that Boeing reported positive operating cash flow realizing a strong sequential improvement driven by negative timing impact in the quarter flowing through the second quarter as a positive timing impact. Free cash flow improved from a $705 million cash burn last year to a negative cash burn of $182 million.

So, we’re seeing revenues and EPS being worse than last year and cash flows being better than last year.

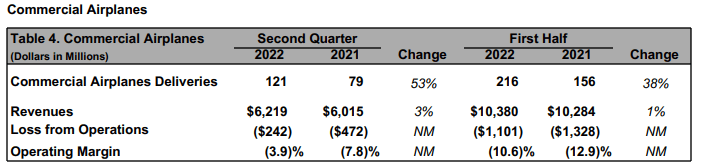

BCA results (Boeing)

During the second quarter Boeing saw a 53% increase in deliveries, but its revenues increased by 3% only. Those are not the results investors were looking for. Base market values of the commercial aircraft deliveries would suggest that Boeing should have reported revenues around $1 billion higher. However, as previously observed current market values likely are significantly lower than base values, and using our CMV estimates we get to revenue of $6.089 billion, meaning that Boeing did beat my expectations by $130 million. We also did see improvement in the operating margin going from -7.8% to -3.9%. Boeing Commercial Airplanes is still not profitable, which is unfortunate, but there is progress. The quarterly results included a $283 million expense of abnormal production costs for the Dreamliner which Boeing continues to expect will total $2 billion once all is set and done. So, without this cost growth Boeing would actually have been profitable during the quarter. Furthermore, Boeing increased its R&D spending for BCA by $169 million. So, we’re seeing that Boeing is stepping up with its R&D spending and that’s important as the company should at some point decide on the launch of its next commercial aircraft program. Not spending the R&D funds now would bolster profits, but leave Boeing with an even bigger problem in the future.

Boeing now expects deliveries for the MAX in the low 400s. That’s a nice guidance to have, because at least there’s somewhat of an indication but it also somewhat indicates a slow unwinding from inventories as Boeing hit a production rate of 31 aircraft per month while 189 aircraft were delivered in the first half of the year. That would bring the remaining deliveries to around 40 aircraft per month in the remainder of the year which would indicate a net reduction of only 50 737 MAX jets from inventories in the second half of the year. So, while demand for air travel is improving we’re not seeing an acceleration in the inventory unwind. That, in part, is driven by China still being a closed market for the MAX

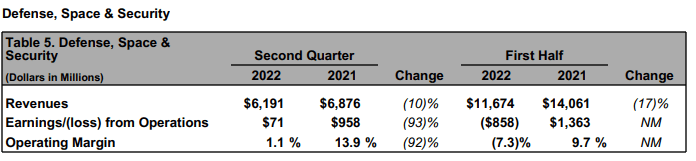

BDS results (Boeing)

Yesterday, I analyzed the quarterly results of Raytheon (RTX) and what I concluded was that commercial aerospace strength was visible, but the desired stability of Defense was largely absent. Boeing’s results showed somewhat of the same. Revenues declined by 10% as Boeing rather quietly slipped in a production rate reduction on the P-8 Poseidon from 1.5 per month to 1 per month and top line was also pressured by some negative adjustments on development programs. Boeing saw a total of $327 million in cost growth, $147 on the MQ-25, $93 million on the Commercial Crew Program, $51 million on T-7A Red Hawk production options and $36 million on the Engineering and Manufacturing Development for the T-7A. Absent of these cost items margins would be around 5%.

The performance that we see at BDS is not great. In fact, it’s bad. It’s better than last quarter but Boeing’s Defense programs once hailed as the future of its defense business are currently providing the company with a headache and cost headwinds. So, BDS really was a disappointing item once again.

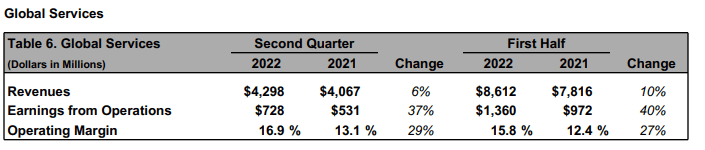

BGS results (Boeing)

Boeing Global Services showed strength during the quarter. Boeing has been working on expanding its services portfolio for years and we’re seeing that with growing flight hours, revenues are increasing, and margins are being boosted by favorable mix.

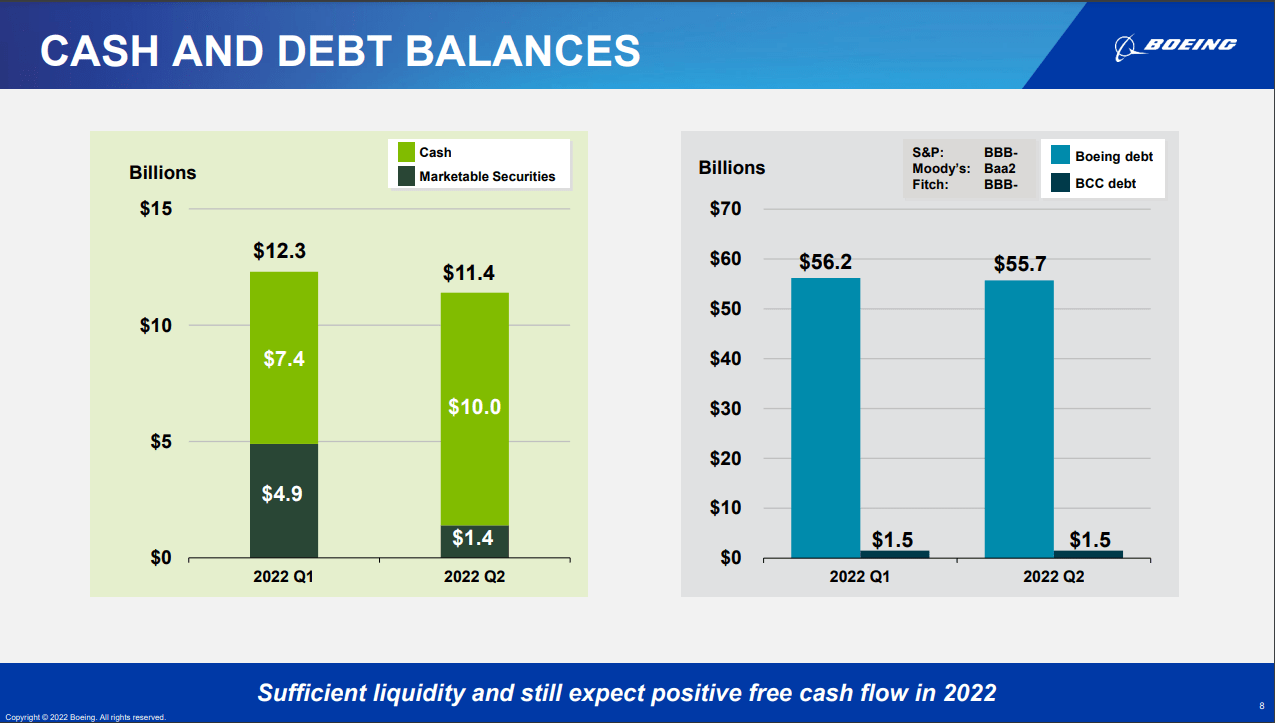

Debt balance barely improves

Debt and cash balance (Boeing)

During the quarter we saw that Boeing debt reduced by $0.5 billion while cash and marketable securities reduced by $0.9 billion reflecting in part the debt reduction, investments and operating inefficiency.

Conclusion

Looking at Boeing’s Q2 results, I wouldn’t say it was extremely bad or extremely good. Boeing’s revenues suggest that aircraft are being sold at prices below base value, on Defense we are seeing disappointing performance while Global Services are exceeding expectations. So, we really see differences between the segments. Overall, I would say that the current delivery flow is not allowing Boeing to meaningfully reduce debt levels. The big pile of Boeing jets in inventories that continuously had been pointed at as being a strong buffer for Boeing to release to the market and get some cash is really being released to the market at a rather disappointingly slow pace and over time that has turned more into an inventory buffer to render compensations.

However, it wasn’t all that bad I would think. Defense is disappointing and the current CEO has not been able to improve anything about that, but overall, we see Boeing pushing R&D higher, a production rate of 31 per month has been achieved for the MAX and would be pushed higher if it weren’t for disruptions in the supply chain around forgings and castings slowing engine deliveries.

Shares of Boeing have not moved much in response to earnings and there also is no need for it. While I remain critical on management, I do think that the message they conveyed showed a slow turn around maybe slower than one would hope but the message overall was realistic admission of the realities we see today throughout the industry. Investors are not known for being patient and as a Boeing investor you have to be extremely patient, but I believe that with a realistic approach to the supply and demand side and required investment in development programs Boeing can positively surprise.

Be the first to comment