Central Bank Watch Overview:

- Against the backdrop of rising bond yields, both the Bank of England and European Central Bank will meet over the next two weeks.

- However, in some form or fashion, policymakers at both central banks have made clear that they’re looking past inflation pressures – and by extension – rising long-end yields in the short-term. Markets are likely to continue to test their resilience (same for Fed).

- Retail trader positioningsuggests that both EUR/USD and GBP/USD rates have mixed biases in the near-term.

Rising Yields Attract Central Bank Attention

In this edition of Central Bank Watch, we’ll cover the two major central banks in Europe: the Bank of England and the European Central Bank. The circumstances each central bank faces are similar in some regards and dramatically different in others.

For the BOE, it has recently quashed talk of moving rates into negative territory, thanks in part due to the rebound in the UK recovery thanks to among the best COVID-19 vaccination rate in the developed world, which has enabled the British Pound to soar at the start of 2021. For the ECB, a pedantic recovery plagued by slow vaccination rates among EU-member countries, thanks in part to equally slow fiscal stimulus efforts, has prompted talk among ECB policymakers of “exchange rate studies” to try and talk down the Euro.

In both cases, however, the recent rise in global bond yields will be a significant part of the conversation moving forward, particularly as the ‘inflation versus reflation’ debate rages among market participants.

For more information on central banks, please visit the DailyFX Central Bank Release Calendar.

Bank of England Not Raising Rates Soon

The last time the BOE gathered, it was for ‘Super Thursday,’ when a fresh batch of BOE forecasts for growth, inflation, and employment (among other items) was produced. An ongoing theme for the UK, the recent vaccination developments have been a positive influence on UK growth expectations, and BOE policymakers have indicated that negative interest rates are not in the cards.

In recent days, with UK Gilt yields on the rise alongside their American counterparts, UK officials have said that elevated yields are indicative of a strengthening economic outlook, brushing aside inflation concerns.

Bank of England Interest Rate Expectations (March 4, 2021) (Table 1)

At the end of 2020, there was a 32% chance of a 25-bps rate cut by the BOE by the end of 2021. Now, that measure stands at 3%. As long as the post-Brexit UK economy remains on pace to overcome COVID-19 faster than most if not all other major developed economies, the BOE is unlikely to act again on the rates channel – even if UK Gilt yields continue to rise.

Recommended by Christopher Vecchio, CFA

Get Your Free GBP Forecast

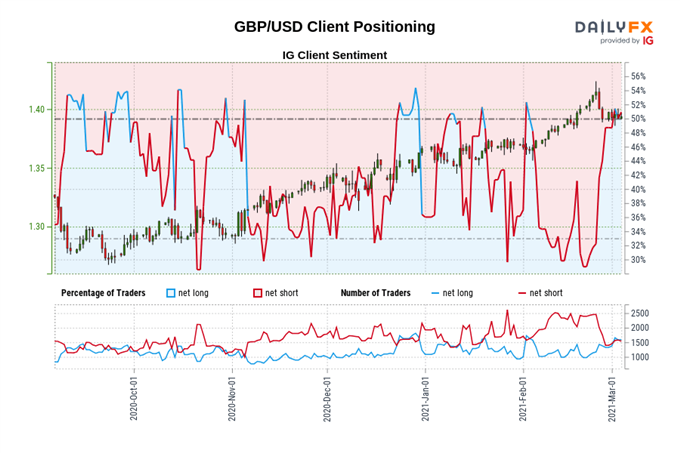

IG Client Sentiment Index: GBP/USD Rate Forecast (March 4, 2021) (Chart 1)

GBP/USD: Retail trader data shows 51.85% of traders are net-long with the ratio of traders long to short at 1.08 to 1. The number of traders net-long is 10.90% lower than yesterday and 13.55% higher from last week, while the number of traders net-short is 0.06% higher than yesterday and 24.10% lower from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-long suggests GBP/USD prices may continue to fall.

Positioning is less net-long than yesterday but more net-long from last week. The combination of current sentiment and recent changes gives us a further mixed GBP/USD trading bias.

ECB May Reconsider Stimulus Pause

In recent weeks, the ECB acknowledged that “if favorable financing conditions can be maintained with asset purchase flows that do not exhaust the envelope over the net purchase horizon of the PEPP, the envelope need not be used in full.” A few weeks later after the global bond yield spike, it seems that the ECB may rethink their plans to provide less stimulus as previously anticipated.

For now, however, like the BOE and the Federal Reserve, there has been a clear drumbeat of ‘higher yields is a positive development!’ Or, in ECB Governing Council member Klaas Knot’s exact words, “what the market is actually doing is pricing that optimism” about a recovery in the second half of 2021.

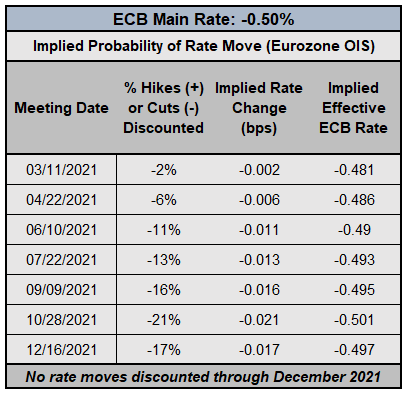

EUROPEAN CENTRAL BANK INTEREST RATE EXPECTATIONS (March 4, 2021) (TABLE 2)

According to Eurozone overnight index swaps, the jump in global bond yields has spilled over to ECB interest rate expectations. In mid-January, when we last looked at ECB interest rate expectations, there was a 54% chance of a 10-bps rate cut by December 2021; that probability has dropped to 17%. This is a deep retracement from where we were at the end of 2020, rates markets were pricing in a 10-bps rate cut in July 2021. It very much seems like the prospect of further ECB stimulus can’t be ruled out if yields keep spiking (as the ECB needs to do the dance of chasing inflation higher), but those stimulus efforts may not be coming vis-à-vis the interest rate channel (e.g. increasing the net purchase horizon of the PEPP).

Recommended by Christopher Vecchio, CFA

Get Your Free EUR Forecast

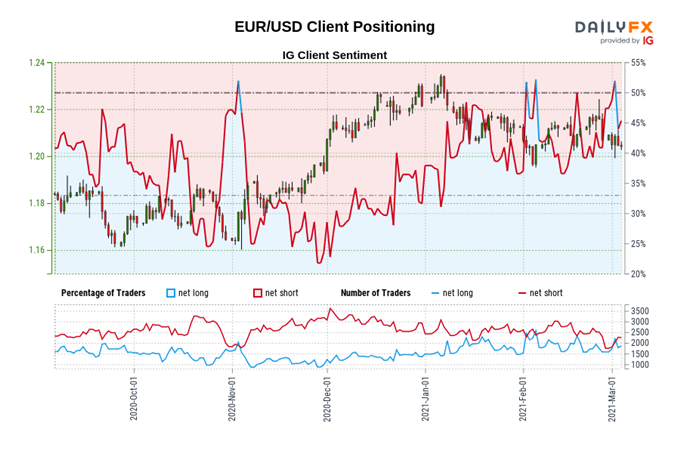

IG Client Sentiment Index: EUR/USD Rate Forecast (March 4, 2021) (Chart 2)

EUR/USD: Retail trader data shows 44.83% of traders are net-long with the ratio of traders short to long at 1.23 to 1. The number of traders net-long is 0.41% lower than yesterday and 10.02% higher from last week, while the number of traders net-short is 4.53% higher than yesterday and 8.89% lower from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-short suggests EUR/USD prices may continue to rise.

Positioning is more net-short than yesterday but less net-short from last week. The combination of current sentiment and recent changes gives us a further mixed EUR/USD trading bias.

— Written by Christopher Vecchio, CFA, Senior Currency Strategist

Be the first to comment