Central Bank Watch Overview:

- There is still some room for BOE rate hike pricing to rise further in the near-term, though it should be noted that there are over three 25-bps rate hikes priced-in through the end of 2022.

- The Euro remains disadvantaged relative to its major counterparts as a result of the ECB’s ongoing recalcitrance towards high inflation figures.

- Retail trader positioning suggests both EUR/USD and GBP/USD rates have bullish trading biases in the near-term.

The End of Stimulus?

In this edition of Central Bank Watch, we’ll cover the two major central banks in Europe: the Bank of England and the European Central Bank.The final meetings of December brought a surprise and a shrug: the BOE delivered on a rate hike that half of market participants didn’t think would transpire; and the ECB continued to suggest that the rise in inflation is temporary, warranting further stimulus through 2022.

For more information on central banks, please visit the DailyFX Central Bank Release Calendar.

Tightening Arrives

Citing factors like “the labour market is tight and has continued to tighten, and there are some signs of greater persistence in domestic cost and price pressures,” the Bank of England surprised markets with a 15-bps rate hike in its final meeting of the year. Ahead of the meeting, rates markets were pricing in roughly a 50% chance of a hike, effectively leaving half of market participants wrong-footed – no matter what the outcome. But with UK inflation rates at 10-year highs and evidence that the labor market is healing more rapidly, markets think that more rate hikes may be ahead.

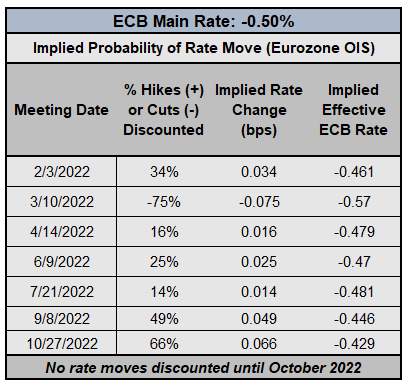

Bank of England Interest Rate Expectations (December 16, 2021) (Table 1)

Following the BOE’s surprise, rates markets are discounting February 2022 as the most likely period for when rates will rise next, with a 66% chance of a 25-bps rate hike. This would be the first BOE meeting of 2022, and when the Monetary Policy Committee will release the next iteration of the Quarterly Inflation Report (QIR). There is still some room for rate hike pricing to rise further in the near-term, though it should be noted that there are over three 25-bps rate hikes priced-in through the end of 2022.

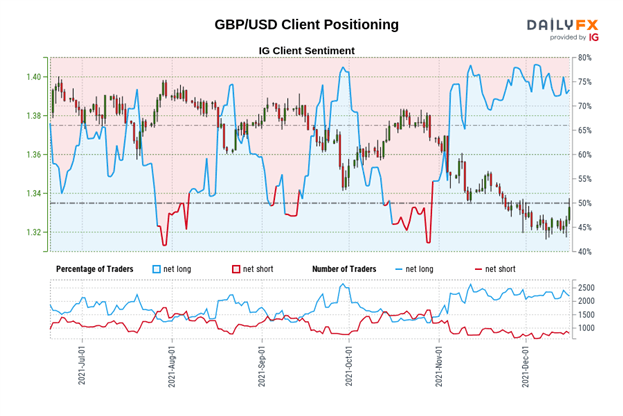

IG Client Sentiment Index: GBP/USD Rate Forecast (December 16, 2021) (Chart 1)

GBP/USD: Retail trader data shows 69.82% of traders are net-long with the ratio of traders long to short at 2.31 to 1. The number of traders net-long is 6.71% lower than yesterday and 12.11% lower from last week, while the number of traders net-short is 10.94% higher than yesterday and 6.16% higher from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-long suggests GBP/USD prices may continue to fall.

Yet traders are less net-long than yesterday and compared with last week. Recent changes in sentiment warn that the current GBP/USD price trend may soon reverse higher despite the fact traders remain net-long.

Market is Still Wrong

Unlike the BOE, the European Central Bank surprised absolutely no one at its final rate decision of 2022. Although the Governing Council announced that it would begin to winddown the Pandemic Emergency Purchase Programme (PEPP) over the next few months ahead of its termination in March 2022, the ECB likewise announced that it would begin increasing bond buying under the Asset Purchase Program (APP). Furthermore, the Governing Council determined that “but monetary accommodation is still needed for inflation to stabilise at the 2% inflation target over the medium term.” In other words, for the ECB, the inflation rise is still very much ‘transitory.’

EUROPEAN CENTRAL BANK INTEREST RATE EXPECTATIONS (December 16, 2021) (TABLE 2)

Insofar as the ECB continues to signal that it has no intention of raising rates or ceasing accommodative policy efforts anytime soon, market pricing around the projected path of ECB rates may still be too hawkish. Rates markets are now pricing in a 66% chance of the first ECB rate hike to arrive in October 2022, odds that may evaporate further over the coming months. The Euro remains disadvantaged relative to its major counterparts as a result of the ECB’s ongoing recalcitrance towards high inflation figures.

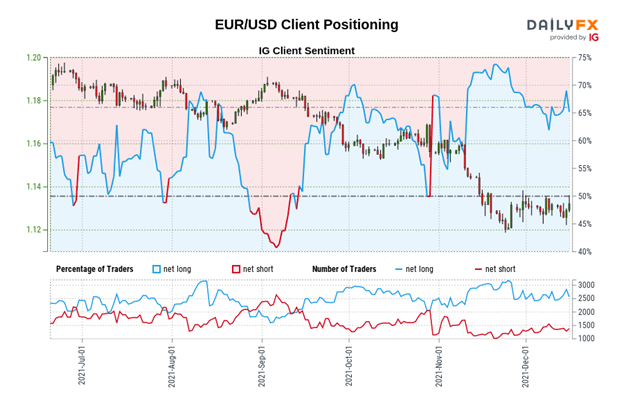

IG Client Sentiment Index: EUR/USD Rate Forecast (December 16, 2021) (Chart 2)

EUR/USD: Retail trader data shows 61.42% of traders are net-long with the ratio of traders long to short at 1.59 to 1. The number of traders net-long is 10.83% lower than yesterday and 10.37% lower from last week, while the number of traders net-short is 5.35% higher than yesterday and 3.43% higher from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-long suggests EUR/USD prices may continue to fall.

Yet traders are less net-long than yesterday and compared with last week. Recent changes in sentiment warn that the current EUR/USD price trend may soon reverse higher despite the fact traders remain net-long.

— Written by Christopher Vecchio, CFA, Senior Strategist

Be the first to comment