Central Bank Watch Overview:

- The December RBA meeting provided a lift to the Australian Dollar, while the December BOC meeting – and its more cautious tone, thanks to the omicron variant – proved to be a letdown for the Canadian Dollar.

- All three central banks covered in this report are expected to hike their main rates in the first half of 2022.

- Retail trader positioning suggests that the near-term outlook is mostly bullish for the trio of major commodity currencies.

Omicron Variant a Cause for Concern?

In this edition of Central Bank Watch, we’re examining the rates markets around the Bank of Canada, Reserve Bank of Australia, and Reserve Bank of New Zealand. The emergence of the omicron variant is provoking some cause for concern, but evidently not enough for rates markets to diminish the possibility that all three central banks covered in this report will raise their main rates in the first half of 2022.

For more information on central banks, please visit the DailyFX Central Bank Release Calendar.

BOC Affirms Forward Guidance

The Bank of Canada surprised few at its December policy meeting, suggesting that forward guidance remained in place that hinted at tightening in early-2022. However, in spite of overheating inflation figures and a surprisingly resilient Canadian labor market, the central bank still issued caution with respect to the end of low rates in light of the emergence of the omicron variant and flooding in British Columbia, which threatens to create more supply chain disruptions. From this strategist’s perspective, omicron won’t cause much trouble, and the strength of the Canadian economy will put the BOC in place to raise rates in 1Q’22.

Bank of Canada Interest Rate Expectations (December 8, 2021) (Table 1)

Following the December BOC rate decision, markets have backed off from their more aggressive expectations regarding how quickly the BOC will tighten policy in 2022. In mid-November, Canada overnight index swaps were pricing in a 100% chance of a 25-bps rate hike in March 2022 with a 31% chance of a 50-bps rate hike; after the December BOC meeting, rates markets are still discounting a 100% chance of a 25-bps rate hike in March, but with a reduced 13% chance of a 50-bps hike.

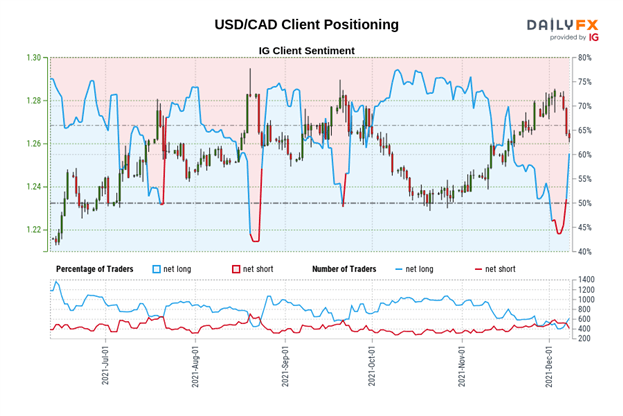

IG Client Sentiment Index: USD/CAD Rate Forecast (December 8, 2021) (Chart 1)

USD/CAD: Retail trader data shows 59.77% of traders are net-long with the ratio of traders long to short at 1.49 to 1. The number of traders net-long is 14.63% higher than yesterday and 9.23% higher from last week, while the number of traders net-short is 11.90% lower than yesterday and 14.05% lower from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-long suggests USD/CAD prices may continue to fall.

Traders are further net-long than yesterday and last week, and the combination of current sentiment and recent changes gives us a stronger USD/CAD-bearish contrarian trading bias.

RBA Continues to Preach Patience

The RBA has preached “patience” with respect to its approach towards normalizing policy, abandoning its yield curve control efforts while at the same time continuing its A$4 billion per week pace of asset purchases. No change in the main rate was met by the RBA abandoning its promise to keep rates on hold until 2024, effectively allowing rates markets to begin pulling forward rate hike expectations in 2022. In turn, this may mean that it’s all but guaranteed that the RBA will cease asset purchases at its first policy meeting next year in February.

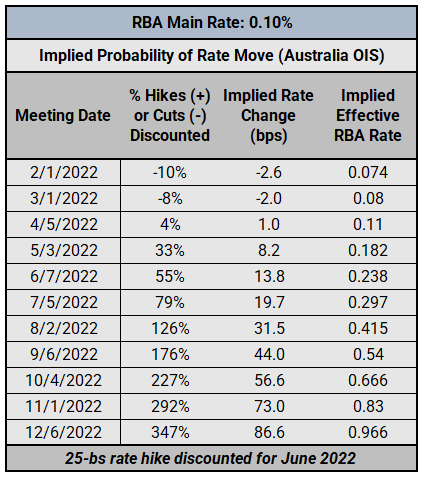

RESERVE BANK OF AUSTRALIA INTEREST RATE EXPECTATIONS (December 8, 2021) (TABLE 2)

As the Australian economy has begun to emerge from lockdowns, and with the RBA signaling that stimulus will soon end, rates markets have slowly started to become more aggressive with respect to the timing of the first RBA rate hike. In our prior update, Australia overnight index swaps were discounting July 2022 as the most likely period for the first rate hike (68% chance). After the final RBA meeting of this year, rates markets are now discounting June 2022 as the most likely period for the first hike (55% chance).

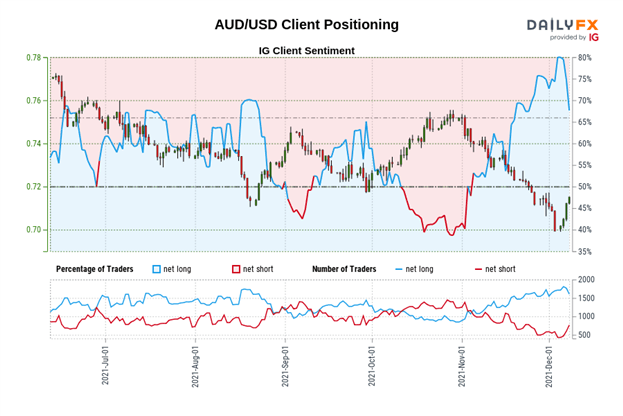

IG Client Sentiment Index: AUD/USD Rate Forecast (DECEMBER 8, 2021) (Chart 2)

AUD/USD: Retail trader data shows 68.97% of traders are net-long with the ratio of traders long to short at 2.22 to 1. The number of traders net-long is 1.26% higher than yesterday and 2.35% higher from last week, while the number of traders net-short is 6.34% lower than yesterday and 9.20% higher from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-long suggests AUD/USD prices may continue to fall.

Positioning is more net-long than yesterday but less net-long from last week. The combination of current sentiment and recent changes gives us a further mixed AUD/USD trading bias.

RBNZ Still Burdens Kiwi

Ahead of the November Reserve Bank of New Zealand rate decision, markets were nearly pricing in a 50-bps rate hike. Of course, the RBNZ only delivered a 25-bps hike at the November meeting, proving to be a letdown for the New Zealand Dollar. But the RBNZ continues to offer hawkish forward guidance, suggesting that a series of interest rate hikes are on the horizon once policymakers meet at the start of 2022.

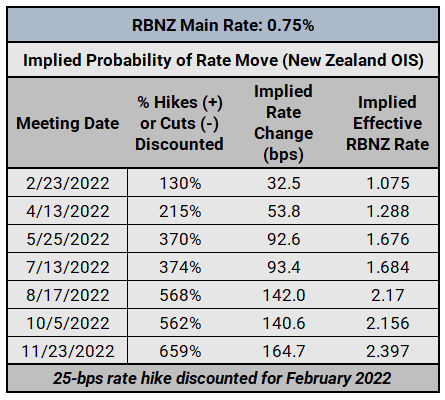

RESERVE BANK OF NEW ZEALAND INTEREST RATE EXPECTATIONS (DECEMBER 8, 2021) (Table 3)

Rates markets are currently discounting a 100% chance of a 25-bps rate hike at the February 2022 RBNZ meeting, with a 30% chance of a 50-bps hike. Should rates only rise 25-bps in February 2022, rates markets are anticipating an immediate step higher in April. Our point of view remains that “it may be the case that RBNZ rate hike pricing is an albatross around the Kiwi’s neck for the foreseeable future” given how aggressive rates markets are already priced; the market is currently forecasting the most aggressive rate hike cycle by any major central bank in the post-Global Financial Crisis era.

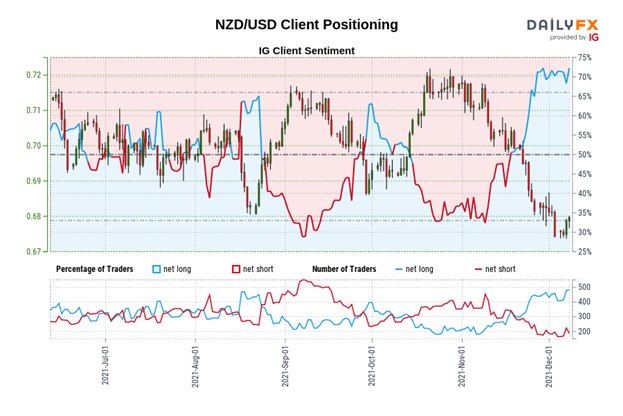

IG Client Sentiment Index: NZD/USD Rate Forecast (DECEMBER 8, 2021) (Chart 3)

NZD/USD: Retail trader data shows 68.26% of traders are net-long with the ratio of traders long to short at 2.15 to 1. The number of traders net-long is 4.61% higher than yesterday and 8.48% higher from last week, while the number of traders net-short is 13.17% higher than yesterday and 17.77% higher from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-long suggests NZD/USD prices may continue to fall.

Yet traders are less net-long than yesterday and compared with last week. Recent changes in sentiment warn that the current NZD/USD price trend may soon reverse higher despite the fact traders remain net-long.

— Written by Christopher Vecchio, CFA, Senior Strategist

Be the first to comment