Andres Victorero

I first wrote about the Vanguard Total Bond Market ETF (NASDAQ:BND) back in March last year, arguing that the Fed was unlikely to hike rates as aggressively as expected, which should be positive for bond ETFs. Since then, the weighted average yield to maturity on the BND’s holdings has risen from 3.0% to 4.6%. While I was clearly early at best with this call, the bullish case today is even more compelling today. Not only has the yield risen since then, but long-term inflation expectations have fallen sharply. As a result, the real yield on offer is now almost 2.4% versus zero in March 2022. The debt-laded U.S. economy is increasingly suffering under the weight of tight monetary conditions, and the BND should perform well as U.S. Treasury demand picks up in response to declining expectations of the Fed’s terminal interest rate.

The BND ETF

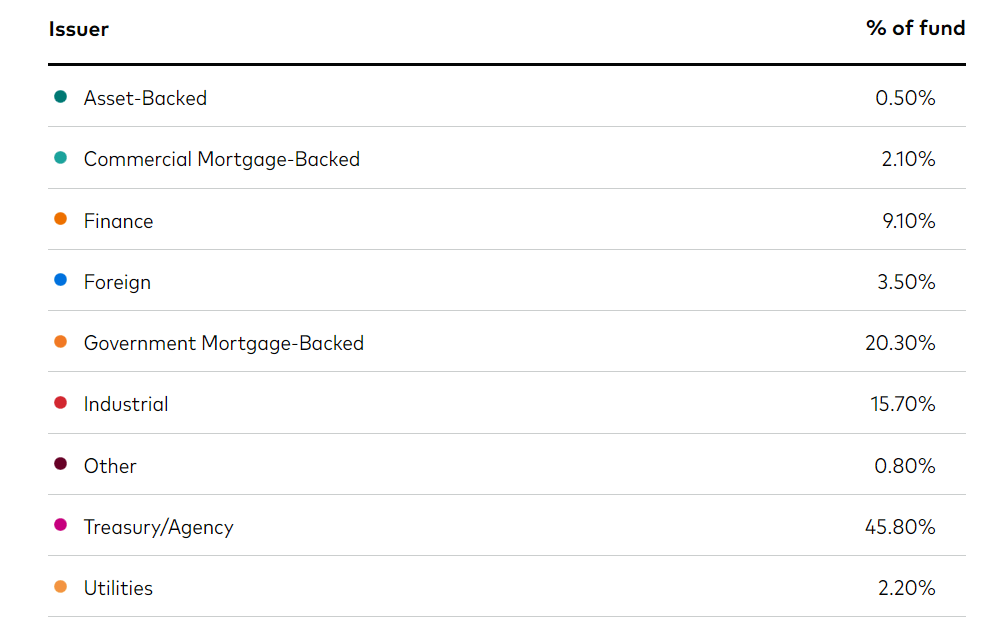

BND tracks the Bloomberg Aggregate Float-Adjusted Bond Index and charges a minimal expense fee of just 4bps per year. BND has an effective maturity of 8.9 years and maturity of 6.5 years. The current yield spread above equivalent maturity U.S. Treasuries is 52bps, which is on par with its long-term average, and reflects the fund’s holdings of corporate and securitized bonds which have higher default risk.

Vanguard.com

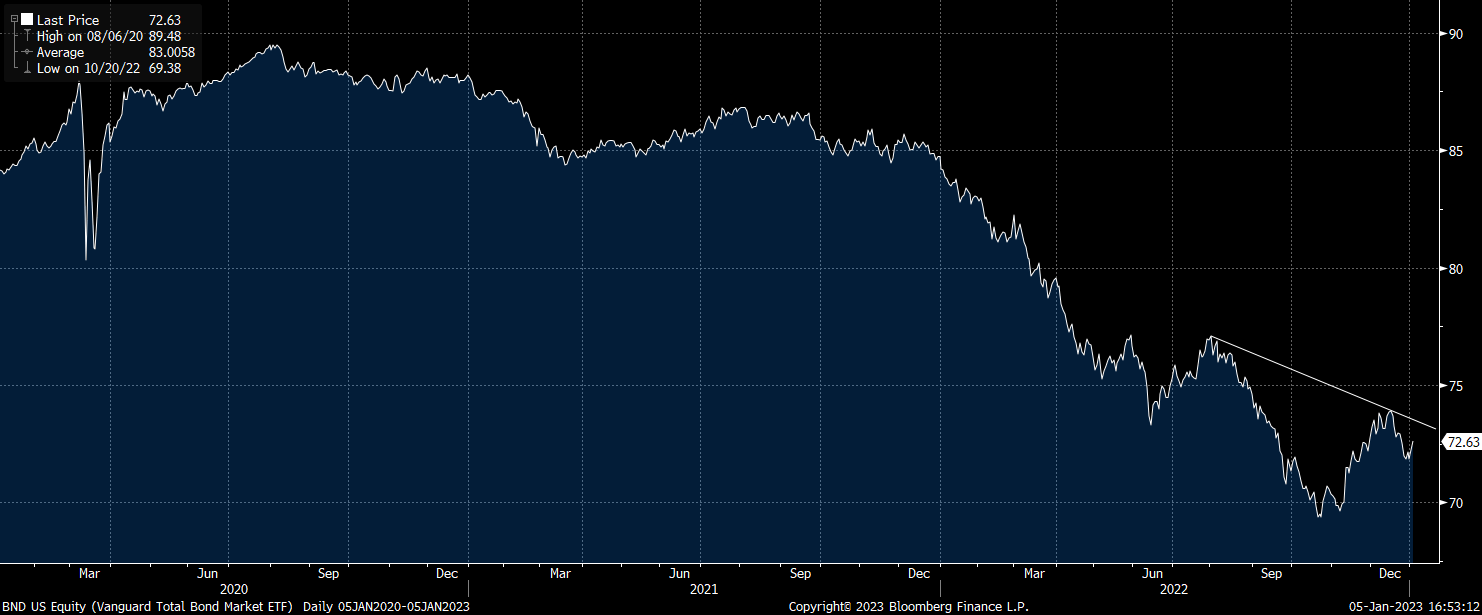

This exposure to credit risk has come at a cost of underperformance during times of credit stress experienced during economic downturns. However, BND has still proven to perform well during such periods as strength in its UST holdings, which comprise almost 50% of the portfolio, has outweighed weakness in its corporate holdings. After holding above its October lows, the BND maybe forming a right shoulder to potentially trigger an inverse head and shoulders reversal pattern.

BND Share Price (Bloomberg)

The Economy Is Faltering Under Collapsing Liquidity

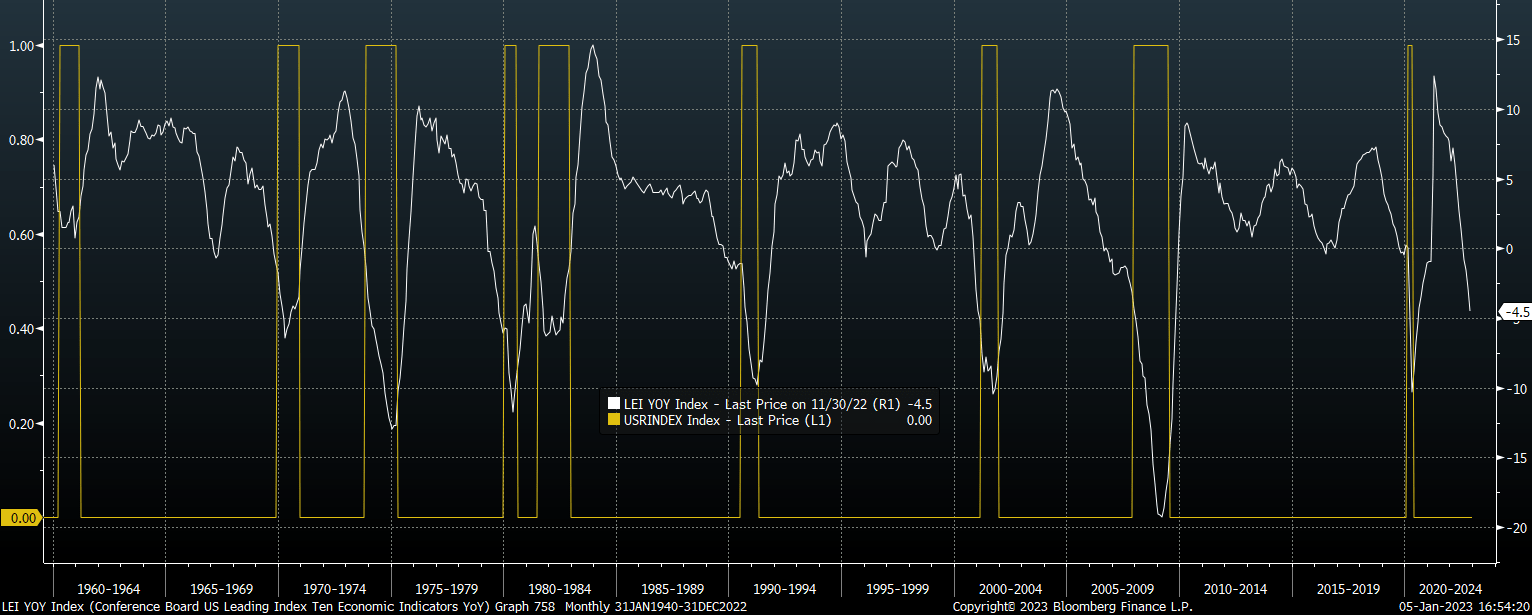

Leading economic indicators are screaming an imminent recession. The Conference Board’s Leading Indicator Index is at -4.5%, a level rarely seen outside of an officially declared recession. A recession is increasingly becoming a baseline view for many economists, but the consensus is overwhelmingly in favor of a mild one.

Leading Indicator Index Vs NBER Defined Recessions (Bloomberg, Conference Board, Bloomberg)

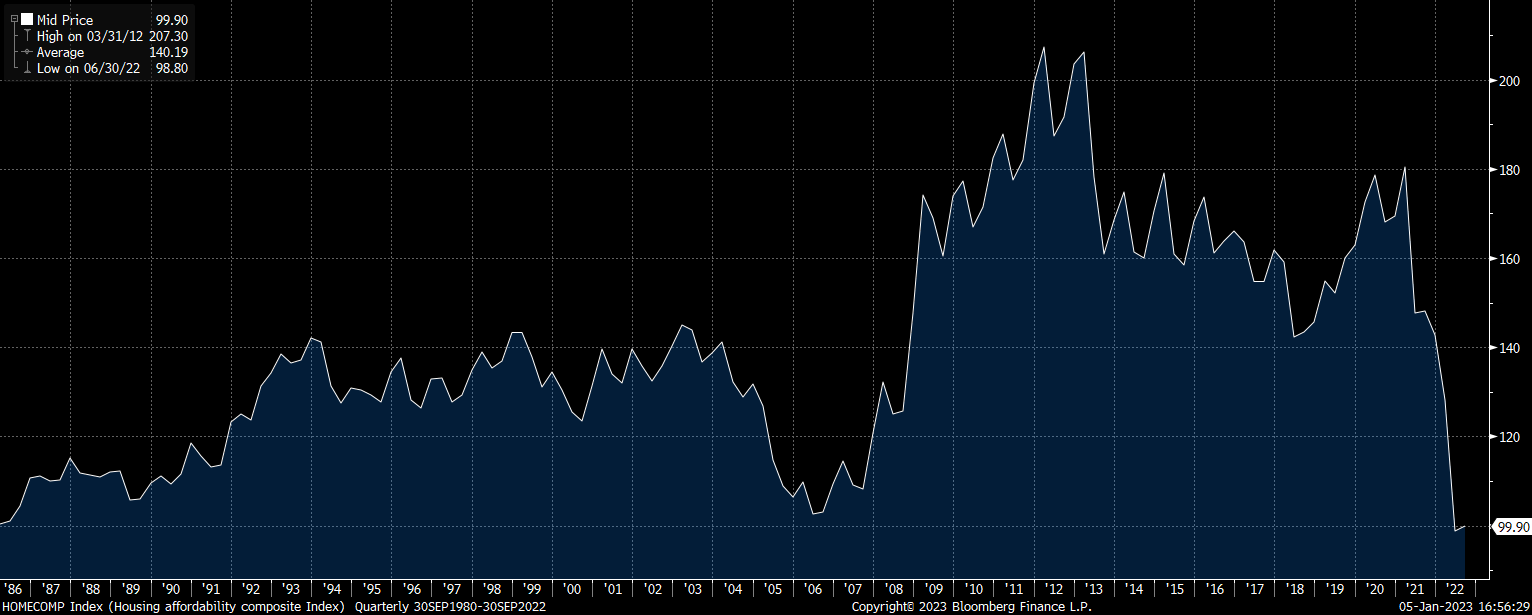

However, when we consider the extreme levels of debt in the economy and the pace at which monetary conditions have tightened, a severe recession looks likely. Housing affordability is a great example of just how much of a problem rising interest rates have become. As the chart below shows, still-high prices and surging mortgage rates have sent affordability to record lows. House prices have already started to decline, and more downside looks likely.

Housing Affordability Index (NAR, Bloomberg)

Not only has the Fed made money more costly by raising interest rates, it has also contributed to the dramatic end of money supply growth due to quantitative tightening. In 62 years of data, M2 money supply has never seen a peak-to-trough decline of more than 0.6% until the past few months. The actual decline since the March 22 peak has been 1.8%, and the decline has not ended yet. The contraction of the Fed’s balance sheet is having a direct drag on the money supply, as private sector credit creation has also slowed.

Against this backdrop of draining liquidity, the risk of a credit crunch is heightened. Should we see further declines in asset prices, this could set in motion a self-feeding scramble for safe assets such as Treasuries, which would in turn further erode scarce liquidity in the economy. In previous severe credit crunches as seen in 2008 and 2020, the BND has experienced initial weakness due to collapsing corporate bond prices but recovered sharply to post new highs over the following months as credit spreads narrowed, and Treasury yields remained low. Risk averse bond investors may wish to stick with USTs to avoid the risk associated with a potential credit crunch, but the BND essentially offers an additional half a percent for the risk that one does not occur.

Summary

The 4.6% yield on the BND is particularly attractive in the context of low long-term inflation expectations, meaning investors should expect to receive 2.4% per year over the next decade or after inflation. Collapsing liquidity is raising the risk of a credit crunch, which would be highly beneficial for U.S. Treasuries. While the substantial weighting of corporate bonds in the BND leaves the ETF at risk of some downside volatility, any weakness should be short lived.

Be the first to comment