Alex Wong

As highlighted at the recent ‘CES Preview’ presentation and this month’s CES event, BMW (OTCPK:BAMXF) continues to defy the perception that it is lagging in the race to electrification. ‘Neue Klasse,’ BMW’s latest iteration of battery technology, promises some impressive targets, including a ~30% range improvement and, most impressively, a ~50% cost reduction. The strong battery performance is a bonus for a company traditionally viewed by investors as a ‘safe pair of hands’ with regard to execution. Beyond the near term, funding the capex requirement of an EV transition could weigh on the balance sheet, but given the strong cash generation from the core business, there should be ample room for shareholder returns (via dividends and the ongoing buyback program). At an undemanding 1-2x fwd EBITDA and ~20% FCF yield, BMW’s equity looks attractive relative to its cash generation ability and best-in-class execution.

Impressive Battery Breakthrough Alongside ‘Neue Klasse’ Architecture Debut

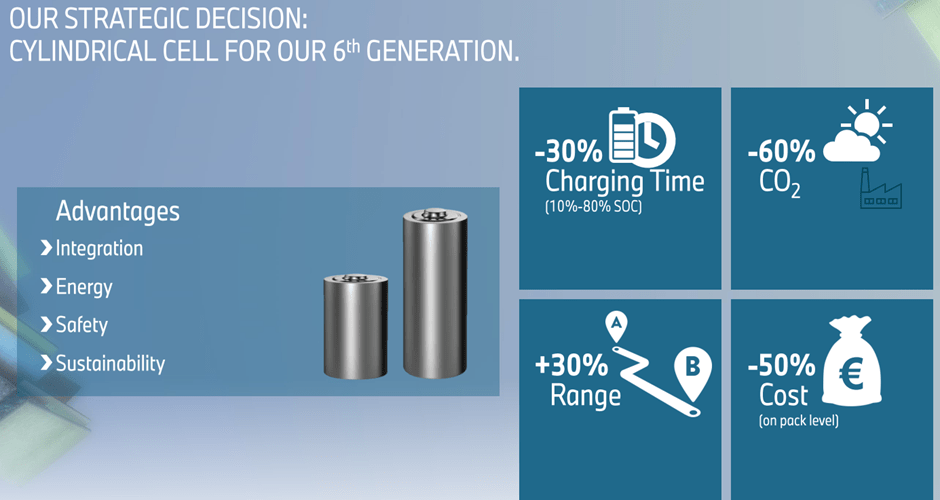

BMW gave investors good reason for optimism at its pre-CES presentation, outlining an EV-focused ‘Neue Klasse’ platform which will feature a new generation of battery technology. As the CES event showed, BMW is making some bold changes in the exterior and interior, highlighting its commitment to adapting to the times. The most impressive part of the presentation, though, was the material gains the company seems to have unlocked relative to its prior battery architecture – this covers not only areas like energy density (>20% improvement) and range (~30% improvement), but also on cost reductions (~50% lower). From here, BMW appears poised to ride the cost curve even lower, given these updated targets come on the heels of major battery tech investments via a new development site in Germany, as well as US-based production sites for EVs and battery assembly.

BMW

As impressive as the new battery projections are, it’s worth questioning the viability of a ~50% reduction in pack-level battery costs within a relatively short period and whether to fully underwrite these numbers. It remains too early to gauge if BMW’s ‘round cell concept’ can truly deliver the promised gains, in my view, but scale benefits should help. Given BMW’s ‘established models’ currently sell ~1m/year and its EV growth is guided at +70% YoY, transitioning these volumes to EVs should drive significant cost reductions over time. Beyond the battery cost gains, a shift toward a direct sales model, higher pricing, and efficiencies from the new platform will also boost the P&L. All in all, management’s target for gross margin parity (vs. ICE vehicles) with the 6th generation EVs, a key milestone on the long-term electrification path, could finally be within reach.

Higher EV-Driven Capex Requirement, but BMW has the Balance Sheet to Match

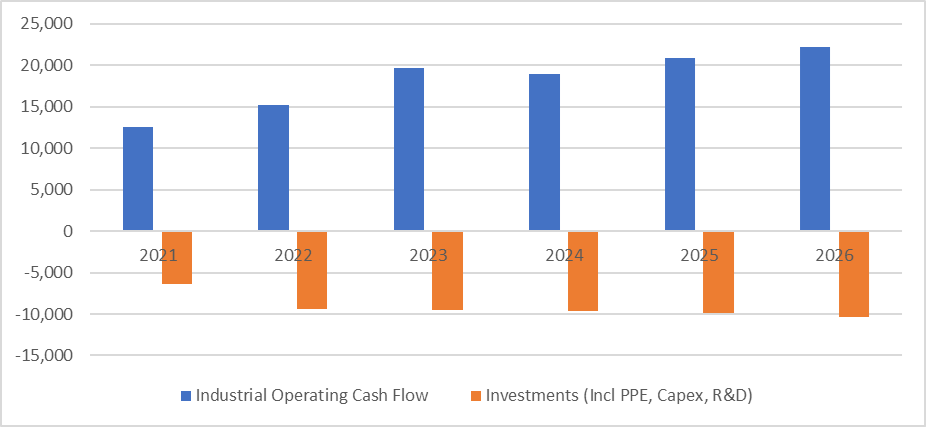

The flip side of BMW’s deepened battery expertise is significantly higher investment levels in the coming years. Recall that management had already guided for higher R&D spending and capex in H2 despite a weaker volume outlook – a stark reminder that BMW is still playing catch-up on EV infrastructure and technology to pure-play EV players like Tesla (TSLA). So, while management deserves credit for its efforts to develop a best-in-class dedicated EV platform, it will need to balance ambition with available funding. Based on the ambitious plans outlined at the ‘Neue Klasse’ presentation, I think it’s safe to assume the capex run rate matching (or even outpacing) revenue growth through FY25.

JP Research

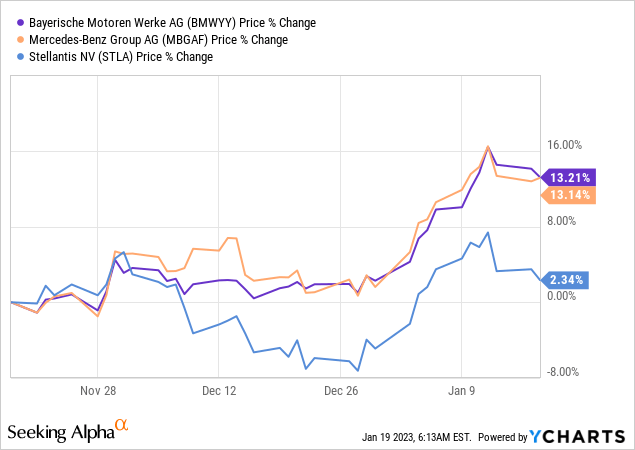

Still, BMW has a big balance sheet to match its spending needs – even assuming a ramp-up to >EUR9bn/year of capex in FY23 and beyond, the >EUR14bn operating cash flow generation from the automotive business should ensure sufficient capacity for capital returns. Given the current valuation at 1-2x fwd EBITDA, BMW management has rightly opted to deploy a large chunk of its excess cash above a EUR20bn gross liquidity floor (including cash and marketable securities) via buybacks. The current program, pegged at ~10% of BMW’s total share capital within five years, has already yielded some promising results – the company’s stock price has outperformed its European peers (Mercedes-Benz Group AG (OTCPK:MBGAF) and Stellantis N.V. (STLA)) despite negative earnings revisions in recent months. With capex dollars increasingly reallocated away from legacy ICE development and as the EV capex cycle winds down in the coming years, BMW should have even more shareholder return capacity, supporting further equity upside ahead.

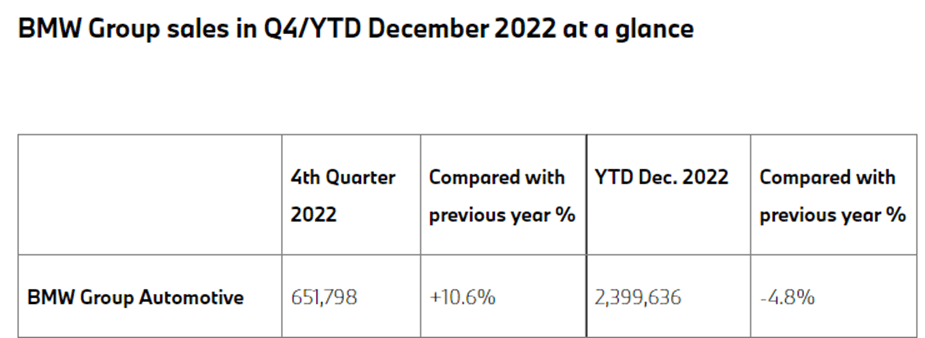

FY22 Deliveries End Slightly Down, But Near-Term Optimism Intact

Despite the long-term promise, BMW still needs to navigate the near-term headwinds. Last week’s deliveries miss at ~2.4m units sold for FY22, for instance, doesn’t bode well for the upcoming Q4 earnings report in March – the implied ~5% decline is short of guidance for a “slight decrease” for the year. The silver lining, however, is that Q4 deliveries of ~652k units are up ~11% YoY, reflecting easing supply constraints through the back half of the year and potentially even a volume upturn in FY23.

BMW

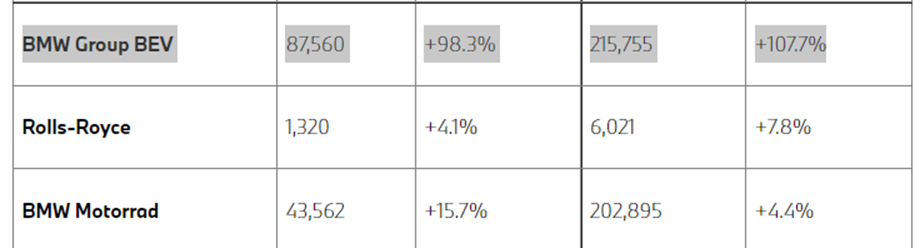

Also, the EV side of the business has been tracking well on penetration rates and volumes relative to its European peers at +108% for the full year. Thus, management’s upbeat commentary (“optimistic about the year ahead”) is perhaps warranted, particularly with the company entering the start of a new product cycle. Among the new EV models coming out of the pipeline include the i7 (launched in November) and the BMW i5, as well as the electrified version of the Rolls-Royce Spectre later this year.

BMW

Making Headway Into the EV Transition with ‘Neue Klasse’

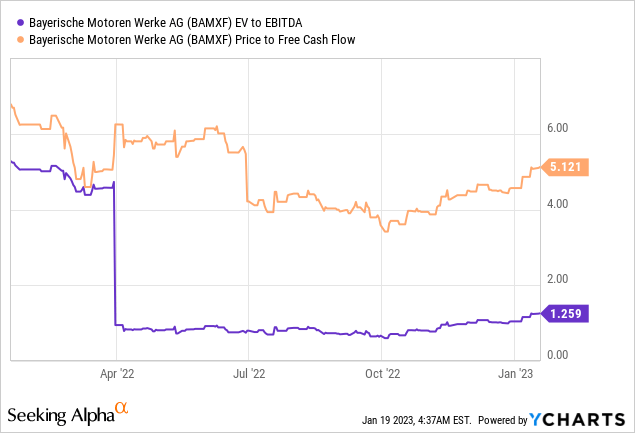

The pre-CES ‘Neue Klasse’ presentation reinforced the notion of BMW as a ‘safe pair of hands’ to ride out the coming changes in the automotive landscape. Alongside the projected battery improvements and solid execution, the company is well-funded by a highly cash-generative ICE business and a fortress balance sheet ahead of the long-term transition into electrification. Relative to its German premium peers, BMW also continues to track well on EV sales, and with an exciting new product cycle in FY23 complementing the existing iX/i4/i3 EV lineup, expect its leadership to extend into the coming year as well. Relative to the best-in-class fundamentals, BMW’s equity is priced at an undemanding 1-2x fwd EV/EBITDA, leaving ample room to re-rate alongside a ramp-up in shareholder returns over time.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment