pchoui

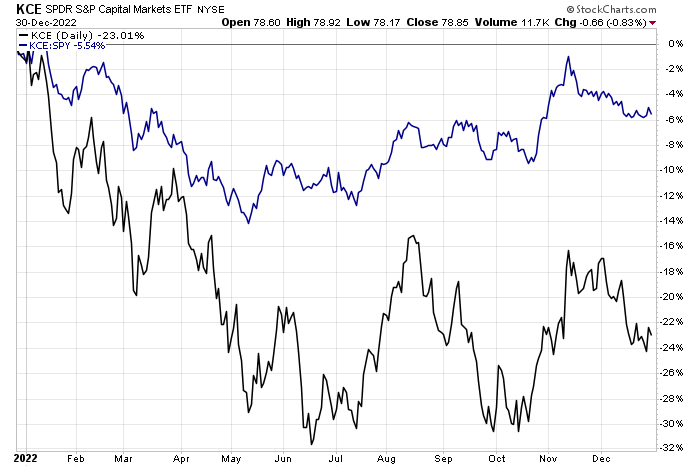

Capital markets stocks suffered in 2022 amid tightening liquidity and a much softer IPO market. Corporate lending could continue to find tough times during the first half of 2023, which could feature a mild recession, according to some economists. One domestic player in the space, though, features fast growth and a high yield. With a volatile stock price in the last several months, is now the time to add some OWL to your portfolio? Let’s take a look.

Capital Markets: Tough 2022

StockCharts.com

According to Bank of America Global Research, Blue Owl is a market leader in direct lending and capital solutions to the alternatives industry. Through the combination of Dyal Capital and Owl Rock, Blue Owl (NYSE:OWL) was formed to offer attractive financing and capital solutions to investment management firms and their portfolio companies. Blue Owl was listed on the NYSE in 2021 and is headquartered in New York.

The $14.8 billion market cap Capital Markets industry company within the Financials sector does not have positive trailing 12-month GAAP earnings and pays a high 4.5% dividend yield, according to The Wall Street Journal.

The company boasts big EPS growth in the upcoming years, with impressive and somewhat insulated margins. Moreover, BofA thinks the stock could be added to indexes over the coming quarters. Blue Owl reported a solid earnings beat back in November, and the stock jumped. Of course, higher competition in the debt markets could hurt the firm’s margins and its variable dividend payout structure is a risk for shareholders.

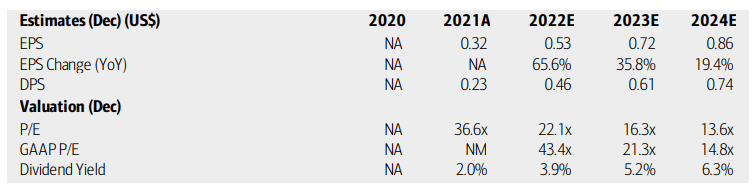

On valuation, analysts at BofA see earnings having risen sharply in 2022 – from $0.32 in 2021 to more than $0.50. Per-share profit growth is expected to persist in the coming quarters, with 36% bottom line growth this year, followed by up nearly +20% in 2024. Dividends are seen as rising from $0.46 in the last 12 months to more than $0.74 for all of 2024 – that’s impressive cash flow for shareholders. Meanwhile, both the operating and GAAP P/Es, while high now, should retreat to the mid-teens two years from now. While there’s uncertainty with that, a solid yield and high EPS growth warrant a premium valuation.

OWL: Earnings, Valuation, Dividend Forecasts

BofA Global Research

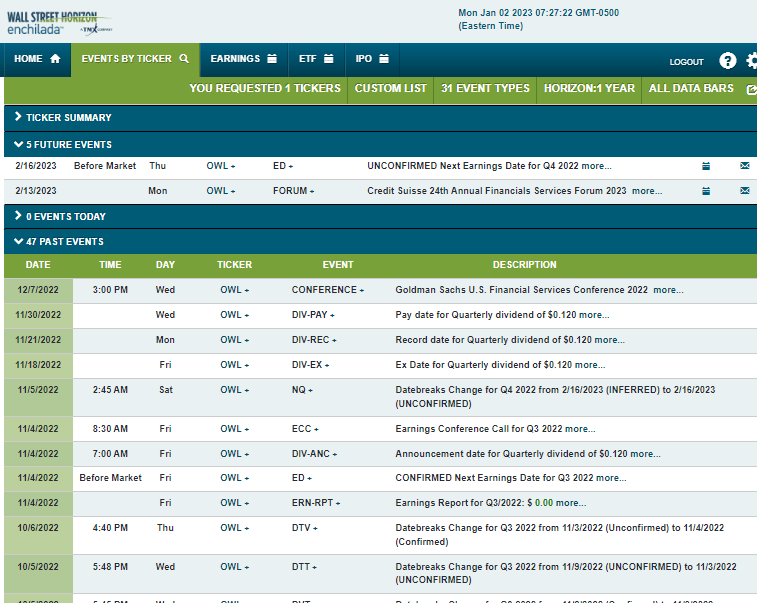

Looking ahead, data from corporate event company Wall Street Horizon show an unconfirmed Q4 2022 earnings date of Thursday, February 16 BMO. Before that, the management team is expected to present at the Credit Suisse 24th Annual Financial Services Forum 2023 starting on Monday, February 13.

Corporate Event Calendar

Wall Street Horizon

The Options Angle

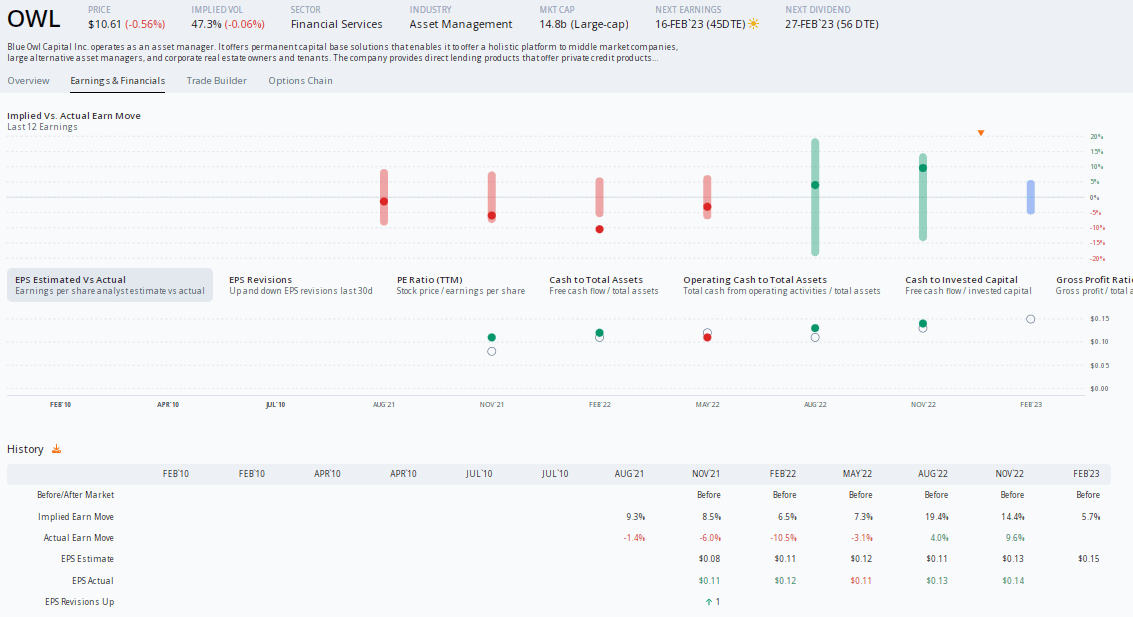

Digging into the upcoming earnings report, data from Option Research & Technology Services (ORATS) show a consensus Q4 EPS estimate of $0.15 which would be a modest increase from $0.12 of per-share profits earned in the same quarter a year ago. OWL has beaten its bottom line forecast in four of the past five quarters and has traded higher post-earnings in the last two reports. This time around, the options market sees a small 5.7% stock price swing after the February quarterly report using the closest expiring at-the-money straddle – that’s a cheap amount of premium compared to previous reports, so playing this one through long options could be a play.

Positive YoY EPS Expected

ORATS

The Technical Take

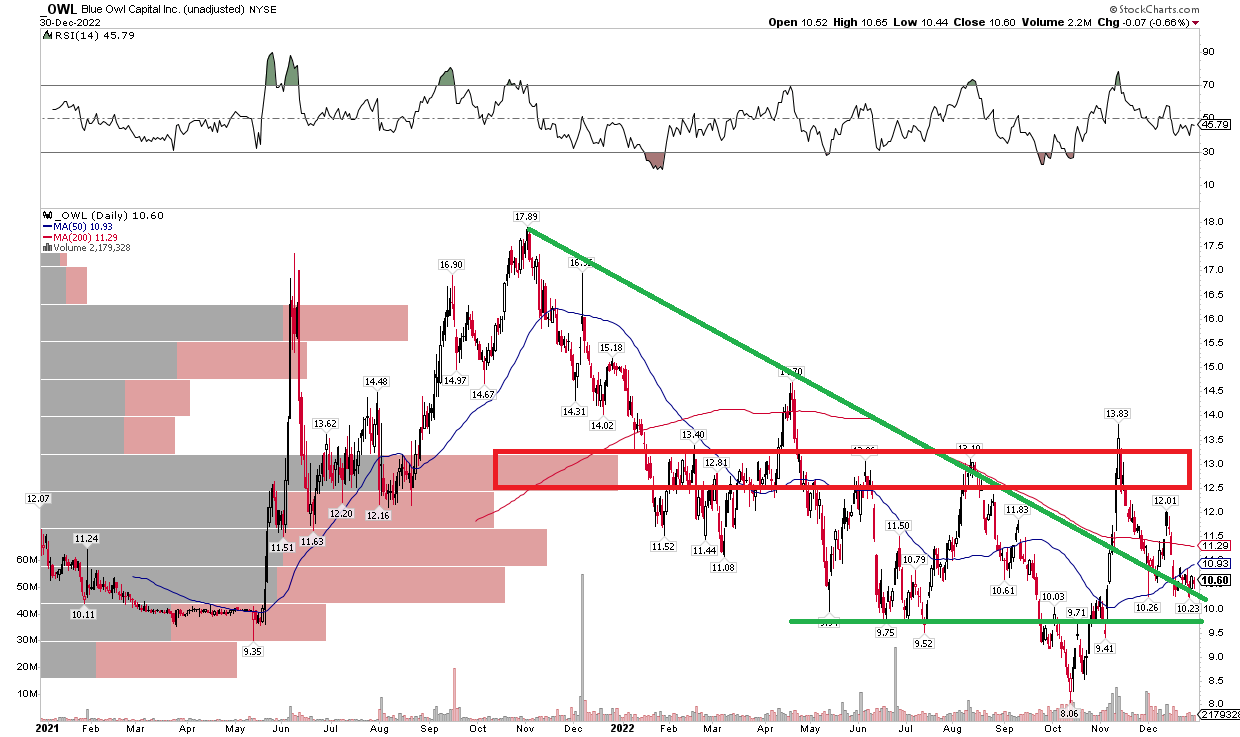

OWL has a somewhat messy chart after going public just a few years ago. Notice in the graph below that shares dipped under important support, to $8, back in October. The stock then rose big to a spike high of $13.83 in November. But that’s where OWL flew into significant overhead supply as measured by the volume-by-price indicator on the left panel of the chart. Still, the stock appears to have broken its downtrend resistance line off the November 2021 peak. Long here with a stop under $9.40 could be a favorable risk/reward play.

OWL: Shares Above A Downtrend Line, Resistance $13 to $14.

StockCharts.com

The Bottom Line

I like the growth prospects on OWL, and I think now is a decent time on the chart to be long ahead of earnings in February. Still, it is a volatile stock, so keep this one as a small speculative piece of your portfolio.

Be the first to comment