Block’s (SQ) Q4 earnings topped revenue and EPS expectations, while it was a strong quarter for Square’s Sellers ecosystem and Cash App. Square’s Sellers ecosystem is increasing its gross profits through value-added services for its merchants, which ultimately help merchants process more payments while helping them manage their business. Cash App continues to gain momentum as it drives active user engagement. I had a chance to attend Block’s earnings call and will demonstrate why this was a blowout year for Block. The company changed its name and acquired Afterpay, which will enable Block to offer consumers credit at the point-of-sale to attract more users to its consumer-facing ecosystem and help drive engagement with higher product adoption.

Block Shareholder Letter

Square Sellers

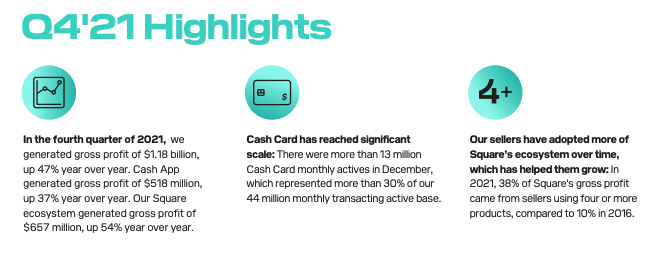

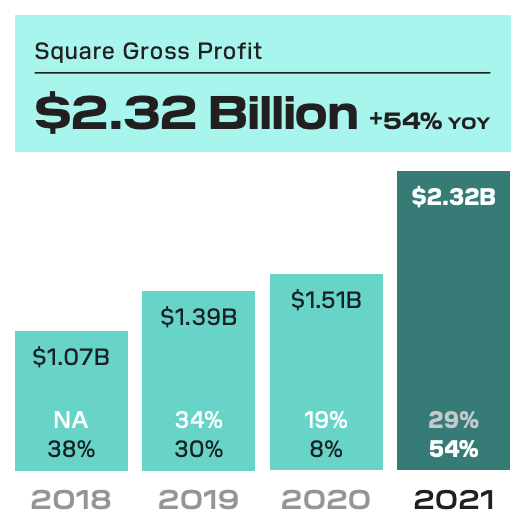

Block’s original ecosystem, Square, posted a strong quarter to wrap up the year for which Square’s gross profit increased 54% annually and by 29% over a 2-year CAGR. Square Sellers revenue for the year grew by 47% annually to $5.19B on easier comps due to the pandemic while its gross profit margin remains consistent at ~45% for this segment.

Block Shareholder Letter

In Q4, 80% of Square’s gross profits came from sellers using two or more Square Sellers products, while 38% came from merchants with four or more products. This is important to understand for Square as it relies on drawing in Sellers as a way to enable them to accept payments from their customers and Square will distribute its processing hardware for free in order to upsell its wide range of value-added services for merchants.

Sellers using four or more products generated more than 10x the gross profit on average in 2021, compared to sellers only using one of Square’s products.” – Block’s Shareholder Letter

As a Seller uses more value-added services provided by Square to increase their processing volume and better manage the back-end of their business, it also provides Square with an abundance of data to learn about each individual Seller and provide each of their merchant’s services, based on the demands of their businesses. For example, since Square processes its customers’ payments, it sees the transaction volume and when it hits the merchant’s books, while Square will make it easy for its merchants to access those funds in real-time or before they happen through a loan from Square Capital. The abundance of information Square has to offer Sellers is extremely valuable, while it enables Square to generate higher returns from Sellers using more than four or more Square products.

Square also continues to build omnichannel capabilities to create a more “cohesive experience” for Square Sellers to directly reach their customers whether in-store or online. There is also a significant opportunity to create a better experience for users to shop online or from a mobile app and receive better-targeted rewards, which will drive engagement for Afterpay and Cash App.

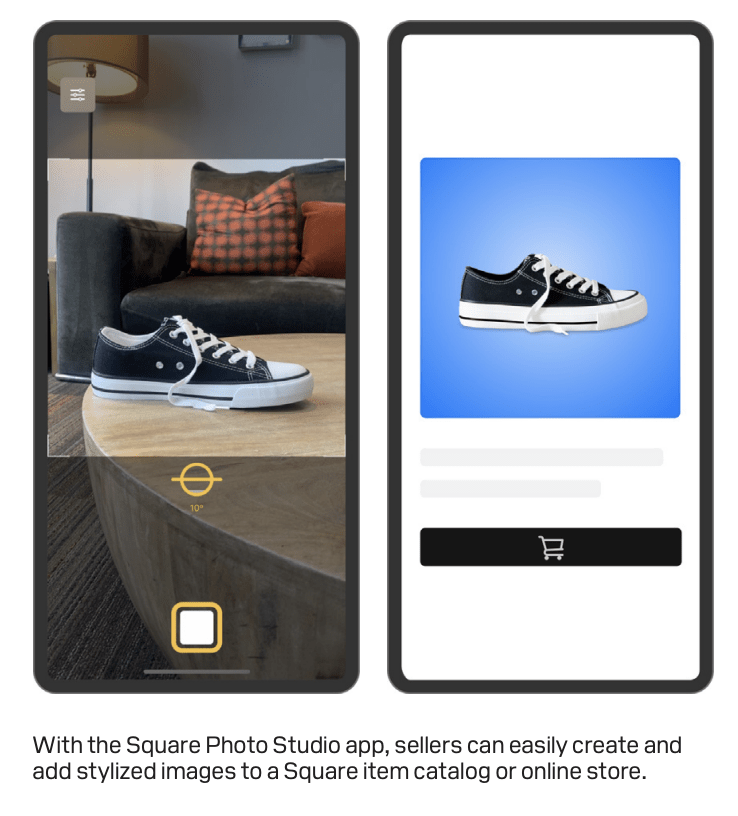

For example, we know that photos are crucial for selling successfully online, but many sellers struggle with the time and cost required. To address this, in the fourth quarter, we introduced the Square Photo Studio, mobile app, which makes it easy for sellers to take high-quality photos and directly sync them to the catalog or online store.” – Jack Dorsey

Block Shareholder Letter

94% of first orders for retailers on Square Online included an image of the product and this feature will make it easier for SMBs to distribute their products or SKUs more effectively. Square will use this feature to enable Square Sellers to better engage their customers and drive better reach, potentially through Afterpay and Cash App as well. In January, Block announced that Afterpay’s BNPL feature is now a payment option at Square’s Online checkout.

Block Shareholder Letter

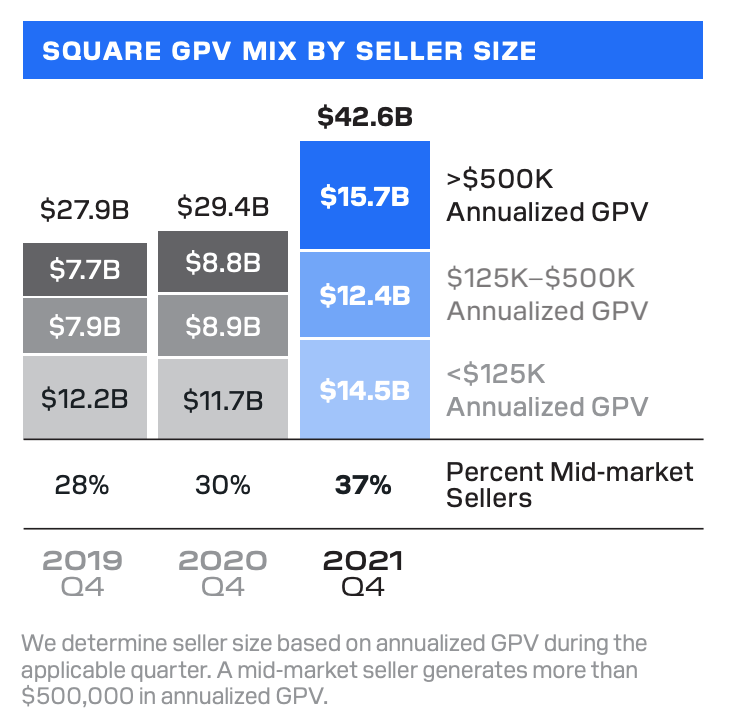

Other Square Sellers highlights for the quarter include a strong GPV mix indicating that Square is focused on moving upmarket. This should result in strong growth from the cohort added in 2021. Square continues to expand internationally as well and recently launched in Spain. Square also invested in marketing to promote its brand and ecosystem within the region. Square has a significant opportunity internationally, especially now with Afterpay on board, which is the BNPL market leader in Australia.

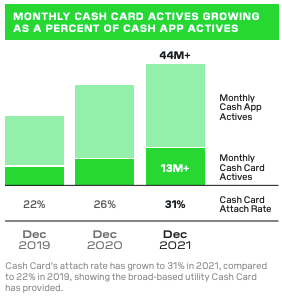

44M monthly transacting active users (grew 22% YoY)

Saw growing adoption of Cash Cards, which reached more than 13M Cash App Active Users (31% attach rate, up 22% 2019)

Spend-per active cash card users increased over time and generated ~$500M in gross profit in 2021, up ~2X compared to 2020.

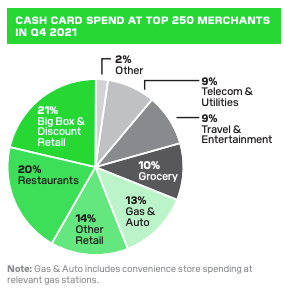

Specifically more active at fast-food restaurants, big-box retailers, gas stations, and more.

Block Shareholder Letter

Cash App saw strong engagement levels and inflows. Recurring paycheck deposits, as well as marketing and boosts, are incentives that Cash App uses as a “lever” to drive Cash App inflows.

In January, Block introduced the Cash App Taxes feature which enables Cash App users to file their taxes for free from a phone or computer and receive their tax refunds up to two days early if deposited through the app. This is an added utility for Cash App users and is an opportunity for Cash App to acquire new customers as well as drive engagement

Cash App Growth Strategy

Customer Acquisition – Historically, Cash App’s relied on its strong network effects to scale its userbase, which was efficient, but now that Cash App has reached a large scale with over 100 million downloads in the U.S., it is focused on growing active users. Cash App is now focused on investing in customers that will generate significant lifetime value.

“So first, customer acquisition; Cash App’s strong network effect has driven efficient acquisition historically. But even as we’ve scaled our investment in the past year with paid marketing to target new audiences that help us drive both brand awareness and engagement with higher product adoption and ultimately ARPU, even with that incremental marketing investment, we increased our CAC to only $10 to acquire a net new active customer in 2021 versus the historic $5, which frankly, you could argue is too efficient. We believe this is lower. That $10 is still lower than other neobanks and a fraction of what a traditional bank would spend to acquire a new customer, and that’s really supported by the efficiency of the model with peer-to-peer embedded within the app.” – Amrita Ahuja, Block CFO

Block Shareholder Letter

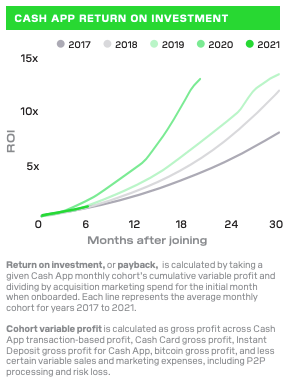

2. Measuring ROI → seeing growing ARPU over time

Generally, an ROI of more than 6x over three years for historical cohorts

In 2021, Block increased Cash App marketing spend by 3x and CAC by 2x, while end-users in this cohort are trending towards a payback period of less than a year

Block Shareholder Letter

3. Engagement – Cash Card still only has a ~30% attachment rate to total active Cash App users while Block reported that the card drives more inflows and engagement for Cash App. (meaningful for Cash App’s go-to-market strategy)

Gross profit per monthly active user of $47, a 13% increase from 2020

Block Shareholder Letter

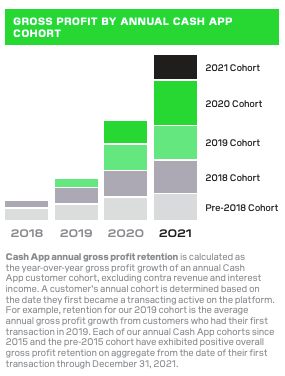

4. Retention – strong gross profit net retention rate of 125% YoY (25% more gross profit per year from an active user net of churn)

Cash App is moving away from its viral growth strategy to focus on driving active users that will become more valuable lifetime customers than compared to before. Cash App’s exponential growth in the last four years can be attributed to a pop-culture (it’s been mentioned in several rap songs massively popular rap songs) like following among the younger demographics, while it’s now focused on attracting more active users and driving product adoption. This is a strategic move for Cash App and now that it will offer a borrowing feature, Cash App Borrow was mentioned on the call, this will enable Cash App to target more users and fuel its two ecosystems of consumers and merchants to enable more commerce. This will be incredibly important for Cash App to develop its borrowing solution to drive better customer engagement as it looks to offer an everyday financial product.

Afterpay

This is a huge connection between our two largest ecosystems, Square and Cash App. On the Square side, this is something that our customers have been asking for, for quite some time. Both for themselves as sellers, but also for their customers. Their customers are driving some of this adoption. The interest thing about after pay is it gets us much closer to much, much larger retailers continuing to go down our omnichannel strategy, making sure that we are meeting our customers wherever they are, whatever size merchants that they want to shop in.

For Cash App, there’s a long roadmap ahead. We haven’t seen much of this. We’ll talk more about this during our Investor Day. But this is to me where a lot of the real excitement lies, is now we have an opportunity for a whole lot more discovery on the Cash App side and giving Cash App customers entirely new capabilities that haven’t had certainly a Cash App before, but I don’t think in any financial instruments.” – Jack Dorsey on the Afterpay acquisition

In regard to the Afterpay acquisition, we are extremely bullish on this opportunity for Block at Beating The Market, as consumer credit is the heart of the economy as it’s how banks or financial institutions lend money directly to individuals, essentially how money is created. If you’re interested in our thesis for what the Afterpay acquisition means for Block, check out the note below.

Afterpay’s Results

Afterpay’s 2021:

The second half of 2021:

GMV up 54% YoY, 84% 2-yr CAGR

Revenue and gross profit grew 53% YoY and 73% 2-Yr CAGR

More than 122,000 annual active merchants, up 64% YoY at the end of the year

More than 19M consumers, up 47% YoY

Losses on consumer receivables 1.17% GMV, an increase of 8 basis points from the first half of 2021 (driven by seasonality and a new mix of regions)

98% of installments were paid on time in the second half of 2021, consistent with the fur

AfterPay didn’t contribute to Block’s 4th quarter results and won’t contribute to Block’s month of January for 2022

For February and March, Block expects Afterpay’s GMV and revenue growth to be between 25% and 30% YoY

Afterpay’s growth in the second half of the year was weaker than expected, but overall, it was a strong year for the BNPL, while GMV was up 84% on a 2-yr basis. Afterpay’s second half of the year may have also been tamed as the acquisition was announced in August of 2021. For Afterpay’s revenue growth next quarter, I expect this is too conservative or that Block anticipates Afterpay drives significant revenue growth for its other two ecosystems. However, considering Afterpay just grew revenues at 71% for the year and 51% for the second half, it’s fair to assume at least 40-50% growth in Afterpay’s revenues as it will be a beneficiary of the ecosystems already in-place at Block.

Updated Valuation

Block’s gross profit for 2021 was $4.42B, up 62% YoY, 53% 2-yr CAGR. When including Afterpay’s, it would be ~$5.045B.

Square Sellers: $2.32B in gross profit,

Cash App: $2.07B in gross profit

Afterpay: ~$625M in gross profit

Forward 12-month revenue contribution of ~$1.3B, ~73% gross profit margins

For our model, we’ll project that Block’s forward 12-month gross profit is ~$6.94 billion, assuming 37.5% growth in the company’s overall gross profits and including Afterpay.

New Entity

Shares Outstanding Combined

New Market Cap ($115/share)

Fwd 12 Mo. Gross Profit

Fwd 12 Mo. Free Cash Flow (45% of gross profit)

Valuation (P/GP)

SQ + AFTPY

650M

$74.75B

$6.94B

$3.123B

10.77x

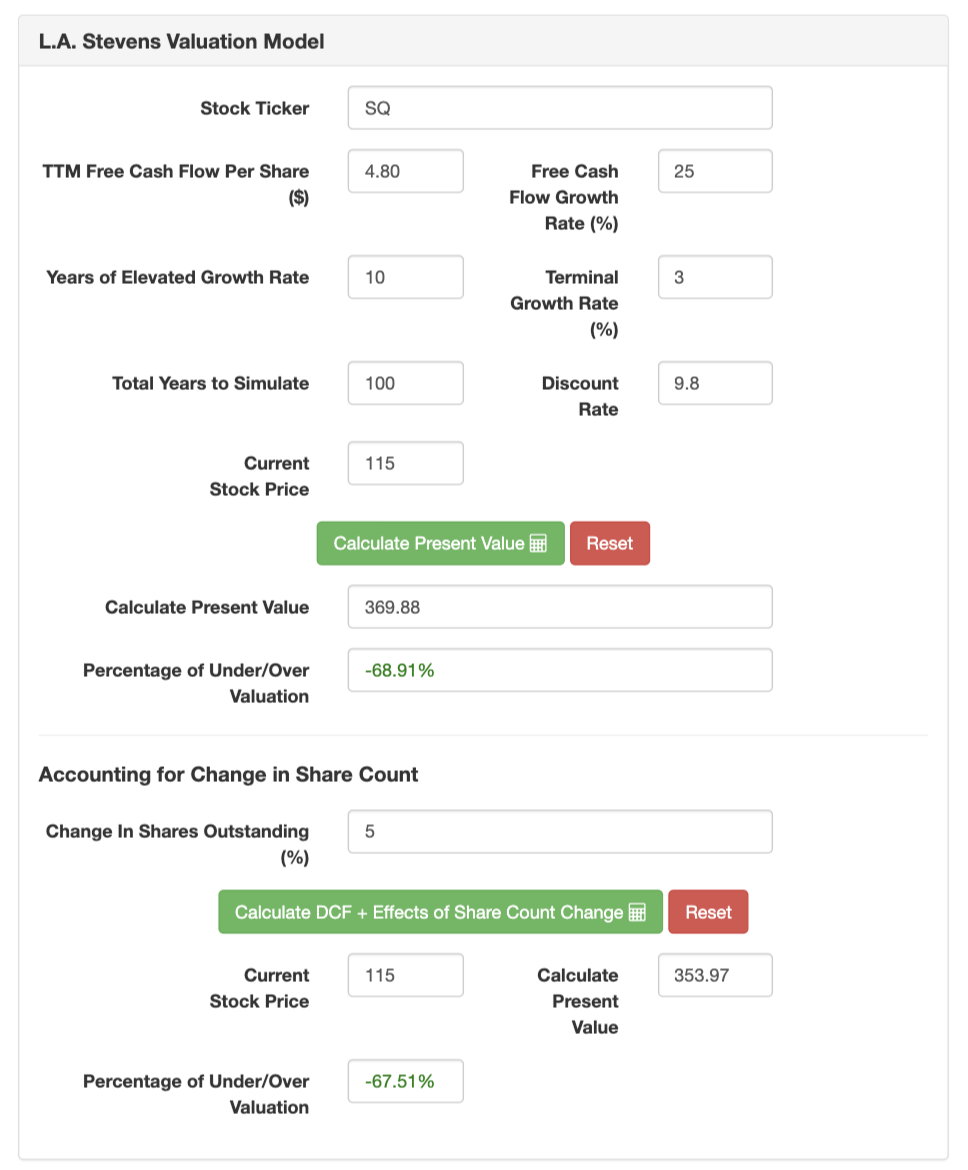

Now, let’s use the L.A. Stevens Valuation Model to determine what Square’s worth today. Here’s what it entails:

In step 1, we use a traditional DCF model with free cash flow discounted by our (shareholders) cost of capital.

In step 2, the model accounts for the effects of the change in shares outstanding (buybacks/dilutions).

In step 3, we normalize valuation for future growth prospects at the end of the ten years. Then, using today’s share price and the projected share price at the end of ten years, we arrive at a CAGR. If this beats the market by enough of a margin, we invest. If not, we wait for a better entry point.

Assumptions:

Forward 12-Month Gross Profit [A] (a conservative estimate)

$3.123 B

Average fully-diluted shares outstanding [B]

~650 million

Free cash flow per share [ C = A / B ]

$4.80

Free cash flow per share growth rate (conservative estimate)

30%

Terminal growth rate

3%

Years of elevated growth

10

Total years to stimulate

100

Discount Rate (Our “Next Best Alternative”)

9.8%

Results:

L.A. Stevens Valuation Model

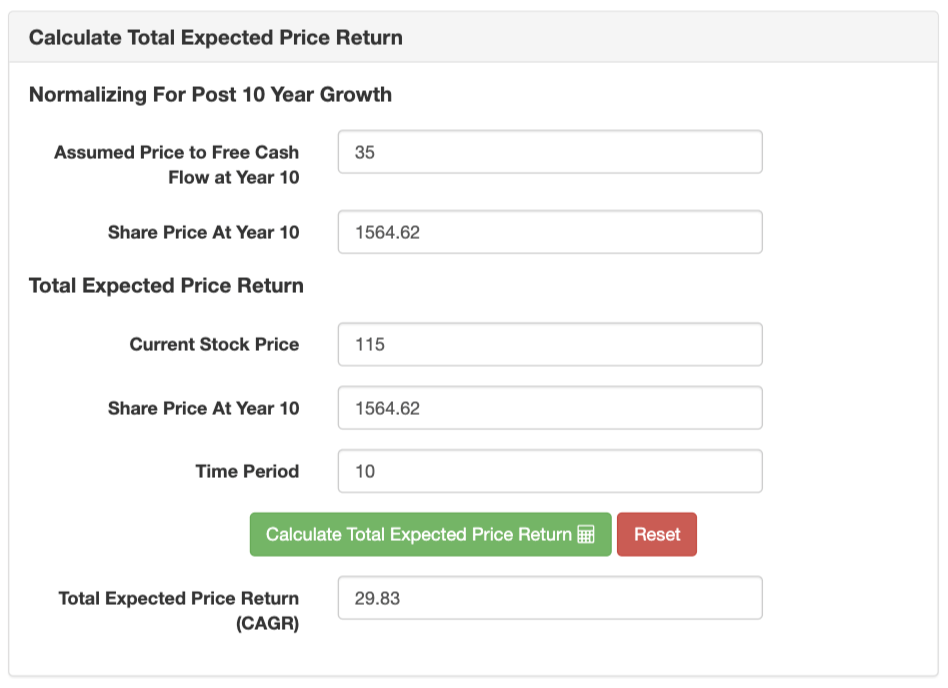

As can be seen above, Block is worth ~$354 per share today, hence it’s undervalued trading closer at $115. In order to determine Block’s projected return, we simply grow the above free cash flow per share at our conservative growth rate, then assign a conservative multiple, (i.e., 35x) to it for year-10. Thereby, we create a conservative intrinsic value projection by which we determine when and where to deploy our capital.

L.A. Stevens Valuation Model

Block is expected to generate a 29% CAGR over the next 10 years and its share price could be more than 10x from where it trades today. I rate Block a buy, for the opportunity it has to create a two-sided network that reorientates the way in which people transfer currency.

Conclusion

At less than an 11X P/GP, Block is trading at a discount compared to its average historical multiple of 17X P/GP, when it was growing at ~50% annually. However, given the opportunity for long-term revenue and gross profit growth of between 35-45% annually, Block’s undervalued and could easily see be deserving of a ~15X P/GP, hence under 11X P/GP.

This was a positive quarter for Block and encouraging to hear that management has a strategic approach to attract active users to Cash App. The acquisition of Afterpay will be crucial for engaging users and connecting Block’s two ecosystems. Block is also generating strong gross profit growth from its Square Sellers ecosystem which continues to add more value-added services to enable merchants to thrive in the economy while helping them process more volume. Block is still in its early days, and I am looking forward to the investor day in May, which I will surely be covering, and expect more information on how Block integrates Afterpay.

Thanks for reading and happy investing! I rate Square a buy under $120.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment