David Gyung

Blackstone Mortgage Trust, Inc. (NYSE:BXMT) has seen some stock price weakness lately and I am an aggressive buyer of the trust’s stock.

Blackstone Mortgage Trust covered its dividend with distributable earnings in the fourth quarter, as expected, suggesting that the current stock price weakness is undeserved.

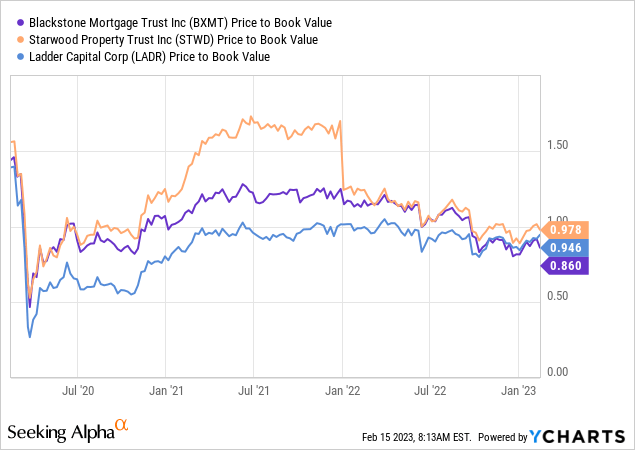

BXMT has re-piqued my interest because its stock is now trading at a discount to book value, despite the fact that the portfolio is performing well and Blackstone Mortgage Trust collected 100% of its scheduled interest in the fourth quarter.

I don’t see anything wrong with chasing BXMT’s 11% dividend yield right now, with the dividend being covered and the portfolio quality being excellent.

High-Quality, Senior Loan Investment Portfolio With Great Credit Quality

Blackstone Mortgage Trust, along with Starwood Property Trust, Inc. (STWD) and Ladder Capital Corp (LADR), is one of the most well-known and largest mortgage real estate investment trusts in the industry.

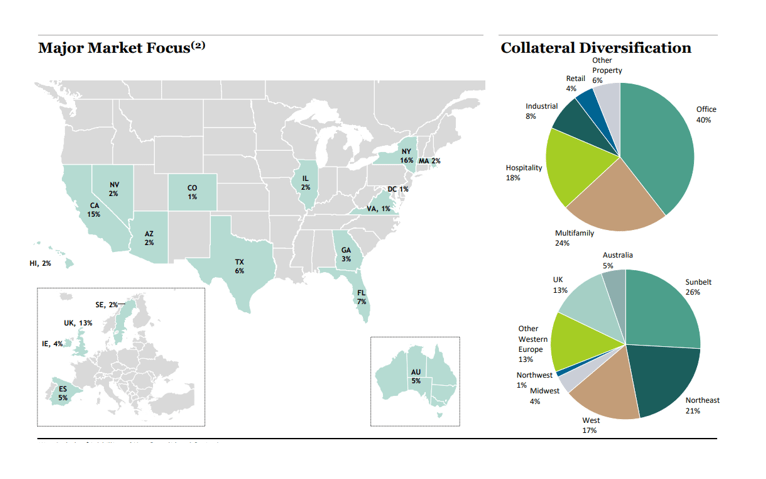

At the end of 2022, the mortgage trust managed a $26.8 billion senior loan portfolio, with office property investments accounting for 40% of the portfolio.

The trust’s primary investment focus is in the United States, but it also has real estate/mortgage investments in Western Europe, particularly the United Kingdom, and in Australia.

Major Market Focus (Blackstone Mortgage Trust)

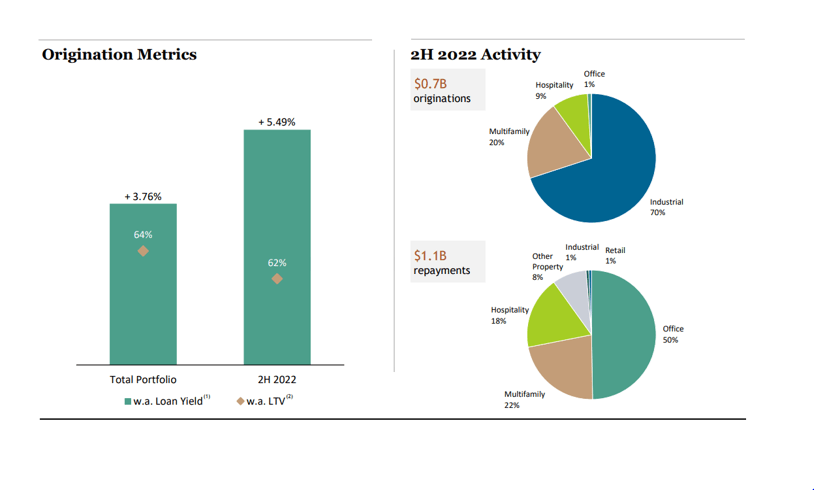

The lending environment changed in the second half of 2022, as capital became more expensive as a result of the central bank’s hawkish approach to interest rate containment. As a result, the company has seen a decrease in new originations while increasing repayments.

Since interest rates rose dramatically in the second half of 2022, Blackstone Mortgage Trust’s new originations could be completed at a higher spread while simultaneously lowering the trust’s loan-to-value ratio on new originations by 2 percentage points. In other words, BXMT originated fewer new loans in the second half of 2022, but the ones it did originate could be locked in at higher rates and with lower portfolio risk.

Originations (Blackstone Mortgage Trust)

Dividend Coverage Remains Absolutely Solid

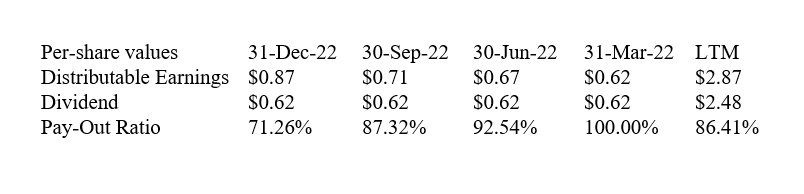

Blackstone Mortgage Trust had distributable earnings of $0.87 per share in the fourth quarter, compared to a dividend payout of $0.62 per share, implying a dividend pay-out ratio of 71.3%.

The dividend payout ratio over the last twelve months was 86.4%, indicating that the dividend is very much sustainable, according to my calculations shown below.

As I will discuss later in the article, Blackstone Mortgage Trust is trading at a discount to book value, which I find astonishing given that the mortgage trust will easily cover its dividend with distributable earnings in 2022.

Dividend (Author Created Table Using Trust Information)

Strong Balance Sheet Supports Opportunistic Growth Potential

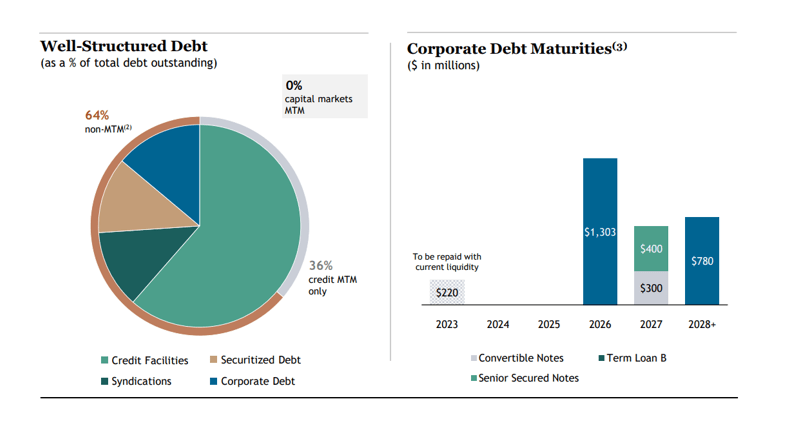

Trusts, in my opinion, should increase their liquidity during times of falling and stagnant origination volumes in order to capitalize on a potential downturn in the economy and real estate sector.

The balance sheet of Blackstone Mortgage Trust supports this opportunistic approach to real estate investing because the trust has no near-term debt maturities and significant liquidity, allowing it to make aggressive investments in a potentially opportunity-rich environment.

With $1.6 billion in liquidity, Blackstone Mortgage Trust has the firepower to double down on real estate/mortgage investments if the opportunity arises.

Debt Maturities (Blackstone Mortgage Trust)

Now Available At A Discount To Book Value

The book value of a mortgage trust is a good indicator of its intrinsic value. It is not a perfect benchmark because portfolios of real estate assets must be written down when asset values fall, but the book value of a senior loan-focused mortgage company is a very good yardstick for estimating a trust’s underlying value. As a result, I believe Blackstone Mortgage Trust currently provides exceptional dividend value to passive income investors, as the company’s assets are trading at a 14% discount.

A trust like BXMT, which has consistently demonstrated strong dividend coverage, should not trade at such a high discount to book value, in my opinion. The fact that other mortgage trusts trade at a discount suggests to me that the entire sector is currently undervalued.

Why BXMT Could See A Lower Valuation

For commercial mortgage trusts, interest rates are both a risk and an opportunity. They are an opportunity in the sense that companies like Blackstone Mortgage Trust have built up significant floating rate exposure (100% of the trust’s loans are floating rate) over time, creating potential for portfolio income growth.

Higher interest rates, on the other hand, make it more likely that some borrowers will be unable to handle a rate reset to the upside.

However, Blackstone Mortgage Trust collected 100% of its interest in Q4 2022 and the entire fiscal year, indicating that credit quality is not an issue for BXMT at this time.

My Conclusion

In 2022, Blackstone Mortgage Trust, Inc. received 100% of its scheduled interest payments, and the mortgage trust once again covered its dividend pay-out of $0.62 per share with distributable earnings.

Given this information, I believe Blackstone Mortgage Trust, Inc. does not deserve to trade at a discount to book value, especially not at such a large discount as we are currently seeing.

The portfolio is fully operational and has excellent credit quality. Blackstone Mortgage Trust, Inc. stock is currently paying an 11% dividend to passive income investors, and I am loading up the truck to profit from the stock price decline.

Be the first to comment