David Gyung

Over the course of last month, the stock yield of Blackstone Mortgage Trust, Inc. (NYSE:BXMT) has risen about 1.5 percentage points to now 11%. I think the pullback in the real estate investment trust (“REIT”), which I believe is completely undeserved, is providing passive income investors with an exceptional buying opportunity that can generate high dividend income for years to come.

However, Blackstone Mortgage Trust provides more than just a high dividend yield; the trust also has appealing senior loan floating rate exposure, which is expected to result in higher distributable earnings in a rising-rate environment.

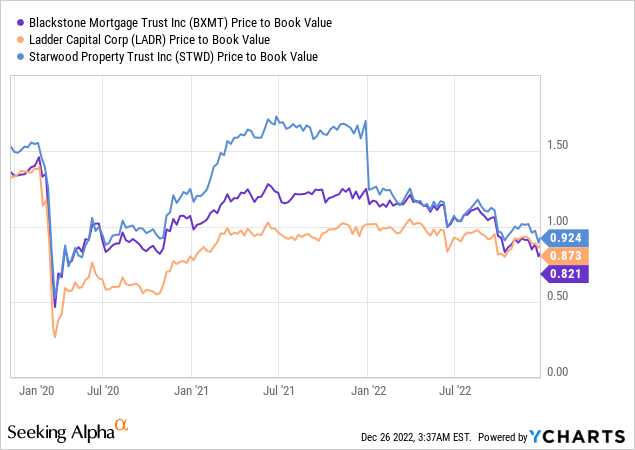

Because of the December pullback, Blackstone Mortgage Trust’s stock is now trading at an even greater discount to book value.

High Quality Senior Loan Portfolio

Blackstone Mortgage Trust invests in high-quality (secured) senior loans in the real estate sector, with a global investment scope that includes the United States, the United Kingdom, Western Europe, and Australia.

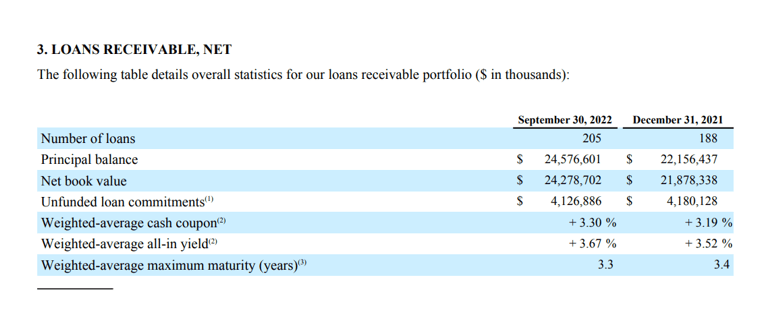

As of September 30, 2022, the trust’s portfolio included 205 senior loans with a principal value of $24.6 billion, representing an 11% increase since the end of the fiscal year in 2021. Blackstone Mortgage Trust’s portfolio is of very high quality, with 99% of its loans performing.

Senior Loan Portfolio (Blackstone Mortgage Trust Inc)

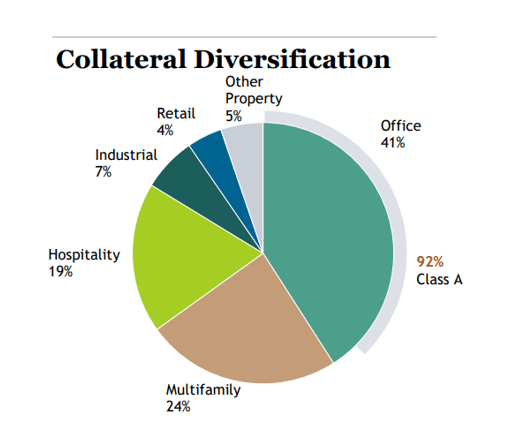

Blackstone Mortgage Trust has developed a primary focus on Class A office real estate and multi-family real estate, which account for 65% of the company’s underlying collateral.

Collateral Diversification (Blackstone Mortgage Trust Inc)

Floating Rate Exposure

One important feature of Blackstone Mortgage Trust’s senior loan portfolio is its sensitivity to floating interest rates, which has clearly been a defining investment theme in 2022. (and will likely be in 2023 also).

The central bank raised interest rates by 50 basis points, bringing current rates to a new range of 4.25% to 4.50%. Interest rates are expected to rise further next year, possibly exceeding 5.0% in the first quarter of 2023, assuming the central bank maintains a strong case for rate hikes in the face of soaring inflation.

Assuming that inflation remains above its long-term average, mortgage trusts with floating rate asset bases may be appealing to passive income investors.

In a rising-rate environment, Blackstone Mortgage Trust’s investment portfolio is 100% floating rate, consisting of high-quality senior loans that will generate higher net interest income and earnings per share.

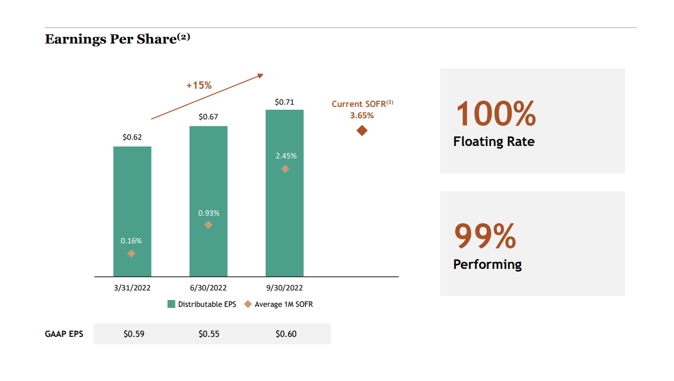

Higher interest rates have already contributed to Blackstone Mortgage Trust’s earnings per share this year, and they have the potential to do even more for the trust’s shareholders. Another 100-basis-point increase is expected to result in a 0.06 per share increase in quarterly distributable earnings.

Earnings Per Share (Blackstone Mortgage Trust Inc)

The floating rate exposure of Blackstone Mortgage Trust may also improve dividend coverage. As I have previously stated, Blackstone Mortgage Trust easily covered its $0.62 per share per quarter dividend with distributable earnings and had an 89% pay-out ratio in the previous twelve months.

Discount Valuation Translates Into High Margin Of Safety

Blackstone Mortgage Trust’s stock price, in my opinion, implies a high margin of safety. The trust’s stock is currently trading at an 18% discount to book value. Other mortgage trusts are trading at discount valuations as well, which could indicate that the market has embedded too much negativity in these valuations.

Where Blackstone Mortgage Trust Has Risk Exposure

The senior loan portfolio of Blackstone Mortgage Trust is performing well, but the mortgage trust has exposure to the commercial real estate market, which has historically been much more volatile and unpredictable than the residential market.

A decline in originations, construction project delays due to a lack of investment capital, and the end of the current interest rate cycle are all potential sources of risk that passive income investors should consider before purchasing BXMT.

My Conclusion

Blackstone Mortgage Trust, in my opinion, is a well-managed mortgage REIT that offers a compelling value proposition in terms of valuation (discount to book value), dividend coverage, and floating rate exposure provided by the trust’s large senior loan portfolio.

I believe the pullback in Blackstone Mortgage Trust, Inc. provides an excellent Christmas present for passive income investors, and the valuation implies a very high margin of safety.

Given that the trust has delivered a consistent dividend for years and that the yield has risen to 11%, Blackstone Mortgage Trust is a must-own stock in my opinion for income investors.

Be the first to comment