imaginima

BlackSky Technology (NYSE:BKSY) is a geospatial intelligence company which uses both hardware and software analytics to provide solutions to its customers. Ideally, the business will have revenues from both government and commercial clients, though uptake on the commercial side until now has been somewhat underwhelming.

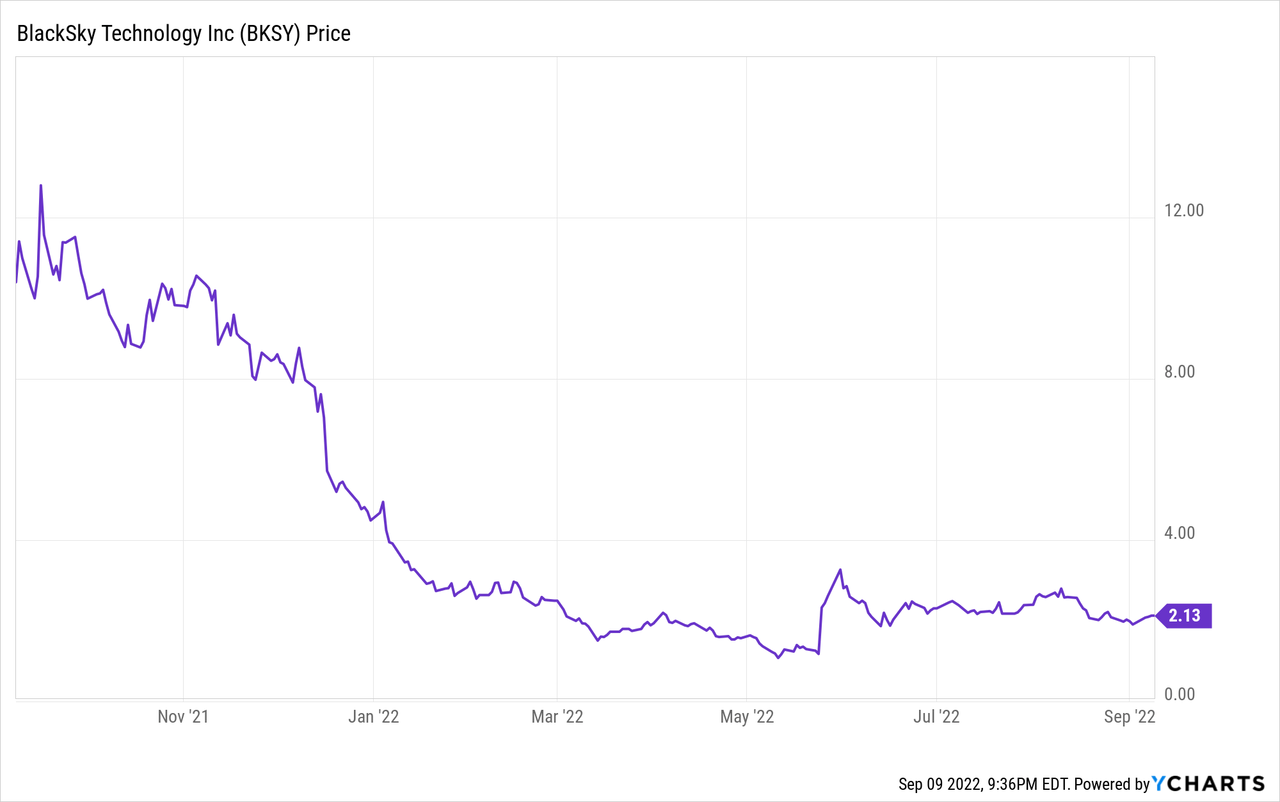

BKSY stock, like many SPACs, has quickly lost the majority of its value. Its downfall was linked to the company badly missing its initial guidance forecast, as I’ll detail below.

Shares have now slumped to the $2 range:

Even at this discounted price, I’m still cautious on the outlook for the company going forward.

BlackSky: Results Are Way Off The Initial Trajectory

To put BlackSky’s issues into context, let’s turn back to their SPAC presentation. This isn’t ancient history, this was from just one year ago, September 2021, where BlackSky offered a rosy outlook for its business going forward:

BlackSky 2021 financial projections (Corporate presentation)

For 2021, the company was supposed to generate $40 million of revenues. It ended up pulling in $34 million. A miss, but not disastrous so far.

In 2022, however, things rapidly spun out of orbit. As of September 2021, BlackSky was projecting $114 million of revenues for 2022. However, it is now projecting just $64 million of midpoint revenues for this year. That’s a 44% decline versus last year’s outlook.

A 44% slash to a company’s revenue outlook sounds pretty terrible on its own. But wait, it gets worse.

Zoom in on the gross profit line of the financials above. Historically, BlackSky has struggled to generate much gross profit as it has had high costs to deliver images to consumers. Over time, gross profit was supposed to soar as the company added more data, software & analytics, and engineering & integration revenues with higher profitability into the mix.

Fast forward to today, however, and this hasn’t quite happened. Last quarter, for example, BlackSky netted just $1.8 million of engineering & integration revenue which would put it on pace for less than $8 million on an annualized basis. That’s way short of the company’s stated 2021 outlook of making $20 million from that revenue stream this year.

Add it all up, and BlackSky’s gross margin has ticked up to 35% as of last quarter. That’s an improvement from last year’s figure, but it’s lightyears away from the 62% gross margin it was supposed to achieve in 2022. Given the high levels of fixed costs and capital expenditures that go into this business, a 35% gross margin simply isn’t going to cut it.

Furthermore, BlackSky initially projected that it would become adjusted EBITDA breakeven in 2022. Instead, so far, it is running larger EBITDA losses in 2022 than 2021. That’s not a good sign.

Why isn’t BlackSky doing a better job of monetizing its existing satellite assets? There is a real question of market fit for the company’s products.

Has BlackSky Found The Right Business Model?

A key consideration is just how big the market may end up being for BlackSky’s technology. Satellite imagery is certainly interesting for some applications. Capturing military movements on camera. Tracking water levels at a reservoir. Monitoring the speed at which a real estate development is being built. The list goes on.

However, for arguably many more applications, satellites will just be a piece of a broader mosaic of data. A company like Palantir (PLTR) can’t run its business just off satellite data, for example. A broader AI solution that can attract big government and commercial contracts across a variety of fields likely needs to incorporate other data such as cell phone analytics, bank information, criminal records, publicly filed government documents and so on.

Bears can reasonably argue that the sort of satellite imagery that BlackSky can offer, in isolation, isn’t worth that much. It may need to be integrated into a broader package or suite of software and information to achieve larger purposes.

Suppose BlackSky can provide satellite data cheaper than its peers, as its proponents suggest. Is there a big market for that? My understanding is clients are more likely to select a provider based on what big picture problem it can solve, rather than just which offers the cheapest service. I’d also point out that image resolution isn’t everything. The commercial business is different from government purposes in that privacy restrictions often limit how highly defined imagery can be for commercial uses regardless of what it possible from a technical perspective.

None of this is to say BlackSky’s business model is inherently flawed or incomplete. However, the company’s low gross margins up-to-date suggest that the company needs to focus on adding more value in its sales process. Being able to launch satellites and provide technical information is a good starting point for a business. But it may not be enough, by itself, to get BlackSky to being a sustainable operation that can generate sizable profits and free cash flows.

What might the end product look like? Take a company like Descartes Labs, which uses a geospatial analytics platform to forecast agricultural production and prices. Descartes gives farm industry participants the following benefits, as per the company’s website:

- Generate consistent alpha through price prediction

- Forecast product supply and demand months ahead

- Monitor deforestation and carbon emissions in your supply chain

- Track crop health and agricultural practices that promote sustainability

Descartes got its start, in large part, thanks to an equity investment from agriculture giant Cargill. Cargill both bought services from Descartes and also led an early funding round for Descartes. This sort of solution-driven approach is likely to be more promising long-term than building the hardware first and then trying to monetize it later. I believe the eventual winners in this space will need to offer clear and achievable benchmarks that solve pain points for customers.

BlackSky may have a sustainable competitive edge from cheaper pricing than peers, but I’m skeptical that pricing per pixel alone will be the defining characteristic that determines winners in this industry. BlackSky has done meaningful work in creating an analytic platform that can help integrate its product more effectively. However, it has seemingly struggled to turn this added analysis into a strong revenue driver. At this point, investors need to see more results before trusting that BlackSky’s commercialization model is working.

Balance Sheet & Valuation

As of June 30, 2022, BlackSky had $111 million of cash and short-term investments left on its balance sheet. That’s a chunky figure on its own.

However, the company is spending roughly $50 million per year annualized on capital expenditures. So $111 million would only keep the company going for a couple of years simply on a capital expenditures basis. Satellites aren’t an industry where you can slack off on new spending; if BlackSky doesn’t invest the necessary capital to keep up, its countless peers in the satellite space would surely gain a technical advantage.

And, of course, there’s more than CAPEX to worry about. The company has generated an operating loss of $48 million through the first six months of 2022. Given the weakness in profit margins and EBITDA generation, investors should expect sizable losses to continue for quite some time.

Long story short, between funding operating losses and investing in new hardware, BlackSky’s cash position is likely to be depleted relatively quickly. The company also already has $72 million of long-term debt, so it has already drawn down a substantial portion of its potential borrowing capacity.

Adding it all up, and it seems likely that BlackSky will have to dilute shareholders fairly significantly to keep the business going. The company had roughly 118 million shares of stock outstanding as of last quarter. To raise another $100 million of cash, which might keep the company running for an additional year, you could be looking at adding something like 50 million more shares outstanding. The dilution here could be rather dramatic.

People can point to the relatively low valuation, such as the company selling for just four times this year’s projected revenues. But, this isn’t a SaaS business. Launching satellites costs a lot of money. Also, BlackSky’s revenue model, so far, hasn’t much resembled a software business; margins are much too low by comparison.

BKSY Stock Verdict

There’s clearly some significant demand for satellite imagery. However, the exact amount remains to be seen. The government will pay any price to get the fastest and highest resolution satellite photos when responding to natural disasters or mounting counterterrorism strikes. This is a great business, but limited in scope.

For companies like BlackSky to reach long-term success, there needs to be far more momentum on the commercial side of things. Companies like oil drillers, agricultural giants, and forestry operators need to find a product offering that is much cheaper than is typically offered to the government, and which solves specific measurable problems.

Just throwing more satellites up into the sky doesn’t automatically ensure that a viable business will follow. Build it and the customers may not, in fact, arrive.

BlackSky has some very cool technology, and some real assets in terms of its already launched satellites and future development plans. However, the financial metrics simply don’t support an investment in the stock at this time. Unless the company can dramatically improve profitability in the near-term, BlackSky seems set for at least several years of ongoing cash burn before reaching a breakeven point. That, in turn, is likely to lead to more share dilution.

This is the sort of stock that goes on a long-term watchlist. BlackSky hasn’t yet proven the commercial viability of its business model. And there are a ton of competitors coming for the space.

The eventual winners are likely to make a small fortune in this space, but there’s a lot of time between now and when real profits will start flowing out of this industry. And there’s no guarantee that it will be BlackSky rather than Planet Labs (PL), Maxar (MAXR), Orbital Insights or even the likes of Blue Origin, Google (GOOGL), or SpaceX that end up being leaders in this field. Given the limited financial results and likely dilution to come in coming months and years, investors will likely be able to buy into BlackSky stock at a more compelling entry point in the future if and when the technology starts to show more tangible commercial results.

Be the first to comment