Joey Ingelhart

The roll-off of low-priced hedges into more attractive hedges this year and next year bode well for Black Stone Minerals (NYSE:BSM). Meanwhile, development deals in its core Shelby Trough should drive production growth, while its Austin Chaulk acreage provides optionality. As a royalty interest company, BSM is also not directly exposed to the same inflationary pressures as E&P companies.

Company Profile

As a mineral interest holder, BSM owns the commodities under tracts of land that it leases to producers in exchange for a royalty interest. E&Ps drill the land and take out the oil and natural gas to sell, while BSM gets a percentage of the production or revenue from the production, typically 20-25%. Unlike E&Ps, it does not have to pay any operating and transport costs, nor does it have to pay F&D costs (finding and development). The company will also often get upfront cash payments when it leases new land called lease bonuses.

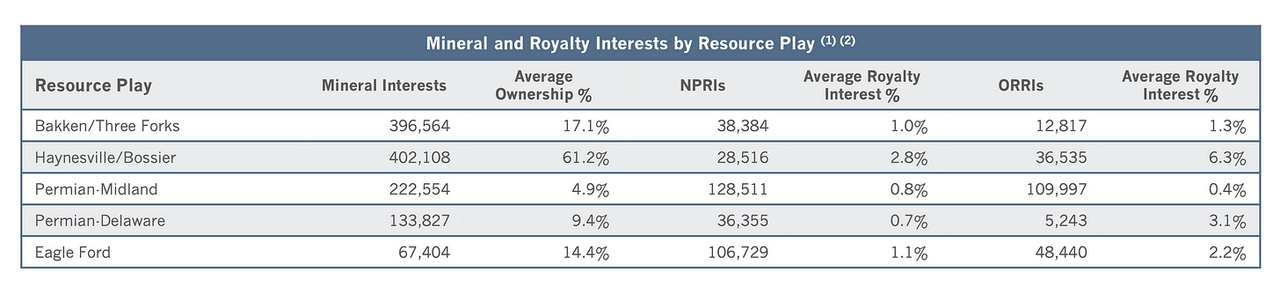

BSM has several types of royalty interests, including nonparticipating royalty interests (NPRIs) and overriding royalty interests (ORRIs). If you want to dig into the nitty-gritty of mineral interests, I’d check out this article.

BSM also has some non-operated working interests, mostly in the Haynesville. With non-operated working interests, it is required to pay its portion of the costs associated with drilling and operating these wells.

The company also has a few farmout agreements where third parties fund the development of wells drilled by its partner Aethon. BSM has two development agreements with Aethon in the Shelby Trough that calls for increasing well counts annually for exclusive access to its acreage and preferred royalty rates.

In the first year, Aethon was required to drill 15 wells. The required number of cumulative wells went up to 25 in September 2022, and will go up to 27 wells next program year. The Shelby Trough is in the southern extent of the Haynesville and Bossier play in East Texas and is BSM’s largest producing area.

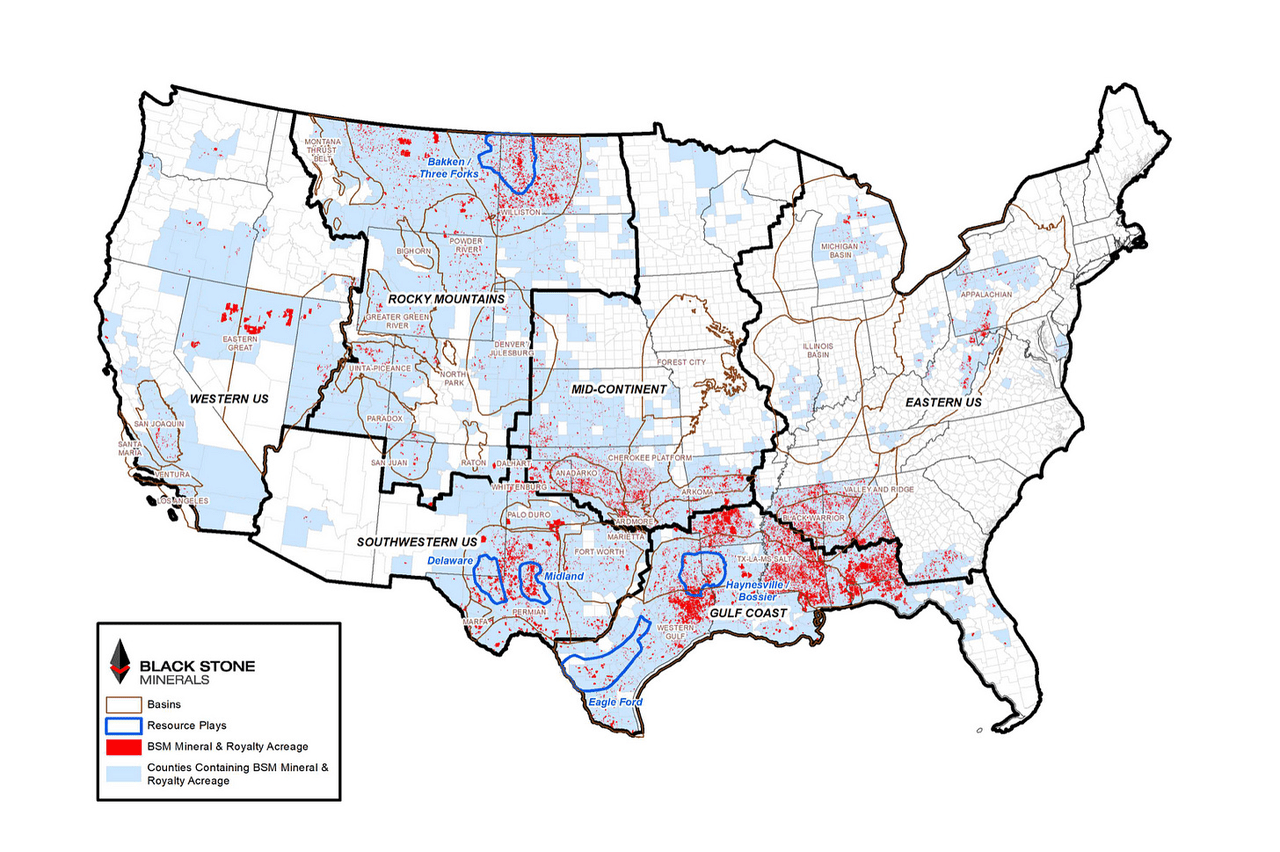

BSM has 20 million gross acres (7.4 million net). Approximately 25% of it is leased, while 75% remains unleased.

Company Presentation

Over 70% of production on BSM’s assets are natural gas. Nearly half comes from the Haynesville/Bossier and Shelby Tough plays in East Texas. It typically hedges 70% of its production 1-year out and 50% 2 years out.

Company Presentation

Opportunities

BSM’s biggest tailwind is that a large percentage of its low-priced natural gas hedges will roll off at the end of the year and will be replaced by hedges that are on average priced 62.5% higher in Q1 2023. The average weighted price on its nat gas swaps will go from $3.12 in Q4 to $5.07 in Q1 2023 and then up to $5.15 for the rest of the year.

The company will also see an increase in price on its oil hedges. Its swap contracts are currently locked in at $66.47 for Q4, and will rise to $78.99 in Q1. The contracts will move to $80.42 for the rest of the year.

The next biggest opportunity for BSM is with its Shelby Trough acreage.

The company should see solid growth in the Shelby Trough given its development deals with Aethon, which it gave royalty relief back in 2020 in exchange for increased drilling.

Back in 2018, the Shelby Trough represented about a third of BSM’s total production, and when COVID hit and natural gas prices fell, operators BP (BP) and XTO, a subsidiary of Exxon Mobil (XOM), stopped drilling the acreage. That led to big volumes declines into 2021.

However, in 2020 BSM remarketed BP’s acreage and signed an agreement with Aethon to develop the acreage with increasing ramps in yearly wells in exchange for lower royalty rates. In 2021, BSM and XTO partitioned some of their acreage, which led to a second development program with Aethon to develop this acreage as well. XTO even returned to the acreage and drilled some wells this year.

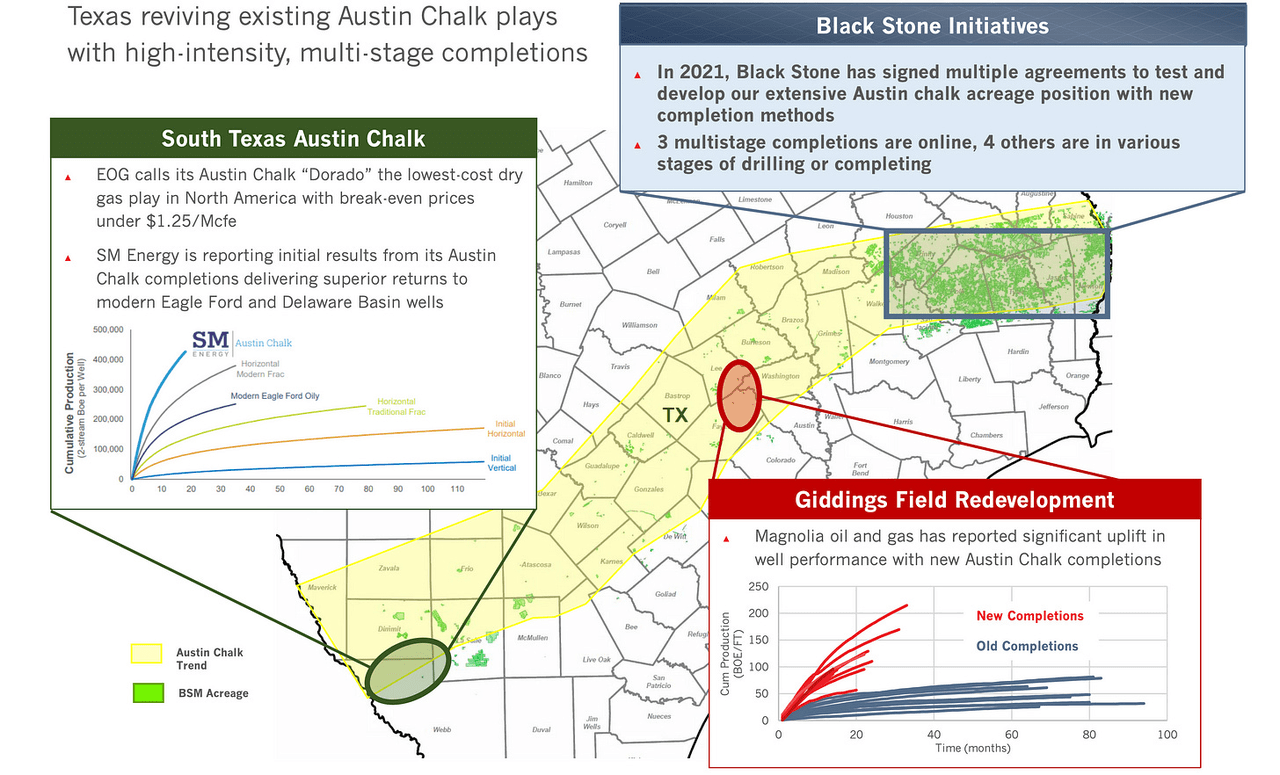

Finally, the Austin Chalk is another area of opportunity for BSM. High-intensity completions have started to show strong results in the basin, and BSM has a strong position in the play. The company has been heavily marketing the basin and has signed multiple agreements with E&Ps to test and develop its acreage.

Three lessees took part in a test program in 2020, and it has brought on 4 additional operators in 2022. Over 20 wells have been drilled and 5 are under development. The company expects about 30 wells to be drilled on its acreage in the next 12 months.

Discussing the Austin Chalk at a conference last week, SM Energy (SM) CFO A. Pursell said: “The theme of this slide together for some for some of us that are old enough to remember the legacy Austin Chalk, which was not so good back in the ’90s and the early 2000s, the Austin Chalk always let you down. You’d have a great well, then you have a bad well, a great well, bad well, great well, turned bad. So just very variable performance, okay? …

“Those are our Austin Chalk wells so far and they look nothing like those old Austin Chalk wells, but they look very much like our Permian wells. …. So very resource play-like, very predictable, great asset, high returns.”

At a conference in June, meanwhile, EOG Resources (EOG) CEO Ezra Yacob said: “And what we did is we were able to find and determine some specific pay criteria, some specific characteristics of Austin Chalk that, for the most part, had been unidentified before. And we mapped that up. We mapped it up all across the Austin Chalk deposition, and we leased areas that had these favorable rock qualities. And what we found was Dorado. It was in the dry gas window. But most importantly, it competed on the returns basis. At $2.50 natural gas price that we use for premium and now double-premium, Dorado competed with that very favorably. And that’s really the outgrowth of.”

Company Presentation

Risks

BSM’s acreage is largely natural gas, and thus natural gas prices can play a big role in its customers’ drilling plans. The company is largely hedged on its production, but it also benefits from prices on the unhedged portion of its production. Thus, natural gas prices are its biggest risk. Prices are down -30% year to date already.

The company also has a lot of basin exposure to the Shelby Trough. At current natural gas prices, this is solid acreage and its development agreement with Aethon adds visibility. However, when COVID hit and nat gas prices dipped, operators stopped drilling here, so there is basin risk

In addition, while the Austin Chalk is a big opportunity, there is also the risk that the play doesn’t emerge for BSM. While the company has seen some nice well results on its acreage, it’s early and not every well has been a winner in the delineation process. The basin has a history of unpredictability, and the more established success from the likes of SM, EOG, and Magnolia has been on acreage southwest of where the bulk of BSM’s acreage is.

Meanwhile, in August Apache (APA) decided to defer most of its drilling and completions in the play due to mixed results. Its acreage is in Brazos Country, which is west of where most of BSM’s acreage is. The company’s first drilled well was outstanding, but when it was delineating the acreage, it saw a lot more variability than it anticipated.

At this point, the Austin Chalk is more potential upside since it hasn’t been drilled, but it would be a negative if the acreage doesn’t turn out to be solid.

Valuation

Filings and FinBox

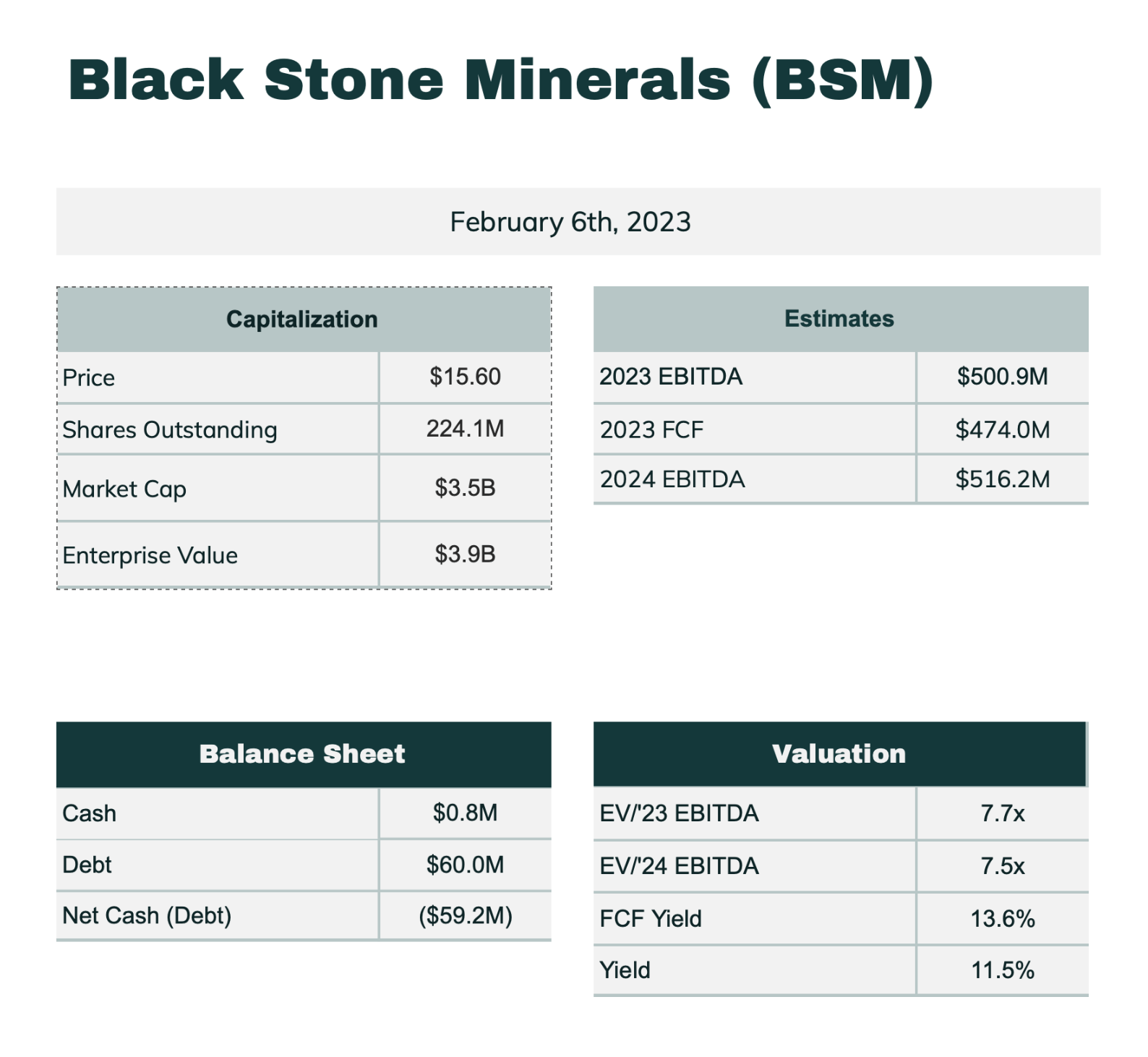

BSM currently trades at about 7.7x the 2023 EBITDA consensus of $500.9 million. Its 2024 EV/EBITDA multiple is similar given that the EBITDA consensus for that year is $516.2 million.

The stock currently has a free cash flow (FCF) yield of about 13.6%, as most of its EBITDA converts into FCF given its lack of CapEx.

The stock pays out a 45-cent quarterly distribution, good for a 11.5% yield.

Conclusion

BSM is attractively valued with a long runway of acreage available for lease and virtually no leverage (0.15x). The roll-off of low-priced hedges will significantly boost its results in 2023 despite recent weakness in natural gas prices, while its deal with Aethon should lead to solid volume growth as well.

Its core acreage position in the Haynesville and Shelby Trough is near LNG export infrastructure, which bodes well longer term as this market continues to grow. Meanwhile, I’d view the Austin Chalk as having nice optionality at this point.

BSM’s robust 2023 FCF yield of over 13.5% is attractive, which it can use to increase its distribution or buyback shares.

Natural gas prices are down -30% year to date already. However, if prices can get a bit of a bounce, I see upside in the stock to $20, while at the same time investors can grab an 11% and growing yield.

Be the first to comment