imaginima

Black Stone Minerals (NYSE:BSM) has seen its unit price go down by -18% since I looked at it in early November 2022. Around three-quarters of Black Stone’s production is natural gas, and natural gas strip prices for 2023 have gone down from around $5.10 in early November to $3.70 now. However, Black Stone also has around half of its projected 2023 natural gas production hedged at a bit over $5, so that reduces the impact of lower gas prices on its distributable cash flow for 2023.

Lower near-term natural gas prices should at least slightly help natural gas prices for 2024 and beyond, which is a period that Black Stone does not currently have any hedges for. Thus I believe that the drop in Black Stone’s unit price is a bit excessive and have moved back to a bullish outlook for its unit price after being neutral on it in early November.

I estimate Black Stone’s value at $18.00 to $18.50 per unit at long-term $70 WTI oil and $4 NYMEX gas now, and believe that it should be able to maintain its current $0.45 per unit quarterly distribution at those commodity prices.

2023 Outlook At Current Strip

I am now modeling Black Stone’s 2023 production at 39,000 BOEPD (approximately 76% natural gas). This is a 1,000 BOEPD reduction from what I modeled it at before, reflecting the probability of a slowdown in development activity (particularly for gassy plays) with the drop in 2023 strip prices.

At current strip ($74 WTI oil and $3.70 NYMEX gas) for 2023, Black Stone is now projected to generate $494 million in revenues before hedges.

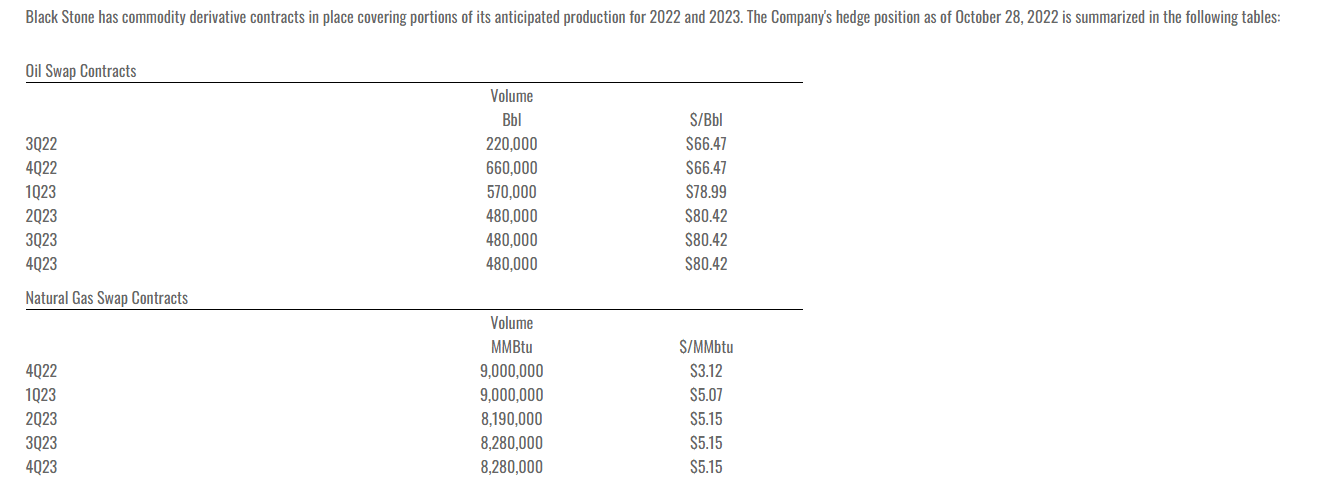

Black Stone has around 52% of its 2023 natural gas production hedged at an average swap price of $5.13. It also has around 60% of its 2023 oil production hedged at an average swap price of approximately $80.

Black Stone’s Hedges (blackstoneminerals.com)

These hedges may have around $60 million in positive value at current 2023 strip prices.

|

Type |

Barrels/Mcf |

Realized $ Per Barrel/Mcf |

Revenue ($ Million) |

|

Oil (Barrels) |

3,376,250 |

$73.00 |

$246 |

|

Natural Gas [MCF] |

65,152,500 |

$3.70 |

$241 |

|

Lease Bonus and Other Income |

$7 |

||

|

Hedge Value |

$60 |

||

|

Total |

$554 |

At current strip, Black Stone is now projected to generate distributable cash flow of $432 million ($2.06 per unit) in 2023. This is around $52 million ($0.25 per unit) lower than what I modeled it at before in early November.

|

$ Million |

|

|

Lease Operating Expense |

$12 |

|

Production Costs And Ad Valorem Taxes |

$50 |

|

Cash G&A |

$37 |

|

Cash Interest |

$2 |

|

Preferred Distributions |

$21 |

|

Total Expenses |

$122 |

Projected Distribution

Black Stone’s current distribution is $0.45 per unit. Given the drop in commodity prices (particularly for natural gas), I believe there is a higher chance that Black Stone maintains its distribution at $0.45 per unit for now rather than increasing it.

With that $0.45 per unit quarterly distribution, it would have 1.14x distribution coverage in 2023 at current strip and should also be able to pay off its credit facility debt by around the end of 2023.

Black Stone is unhedged for 2024, so its distributable cash flow may drop a bit compared to 2023 based on my long-term commodity price expectations of $70 WTI oil and $4.00 NYMEX gas. At 39,000 BOEPD in average production though, it would still have just over 1.0x distribution coverage with a $0.45 per unit quarterly distribution.

Notes On Valuation

My projection of Black Stone’s distributable cash flow in 2023 has gone down by -11% since early November, but its unit price has gone down by -18%. Aside from that, lower strip prices for 2023 should generally support improved prices for 2024 as production growth is trimmed.

I now estimate Black Stone’s value at around $18.00 to $18.50 per unit in a scenario involving long-term (after 2023) $70 WTI oil and $4 NYMEX gas. This is reduced by $0.50 from my previous estimate of its value due to the reduction in projected 2023 distributable cash flow plus slightly lower production expectations entering 2024.

Current strip prices for 2024 and 2025 are near that level, at around $70 WTI oil and $4.10 NYMEX gas over that two-year period.

Conclusion

Black Stone Minerals appears to be a decent value at $15.47 per unit. I estimate its value at $18.00 to $18.50 per unit at long-term $70 WTI oil and $4 NYMEX gas and also believe that it could support its current $0.45 per unit quarterly distribution at those commodity prices.

I did trim my estimate of Black Stone’s value by approximately 3% in response to the decline in commodity price expectations for 2023. However, Black Stone’s unit price has gone down by 18% since early November, so it looks like a better value to me now.

Be the first to comment