hapabapa/iStock Editorial via Getty Images

BioMarin Pharmaceutical (NASDAQ:BMRN) is one of the leaders in the development of innovative treatments for people with rare and ultra-rare diseases. The company’s product portfolio consists of many drugs such as Palynziq, Brineura, Voxzogo, and Naglazyme, which sell hundreds of millions of dollars a year. Strong year-on-year net income growth rates, and a rich pipeline of product candidates targeting diseases that have a significant unmet medical need, make BioMarin Pharmaceutical an attractive candidate for investors in a time of macroeconomic uncertainty.

BioMarin Pharmaceutical’s Financial Position

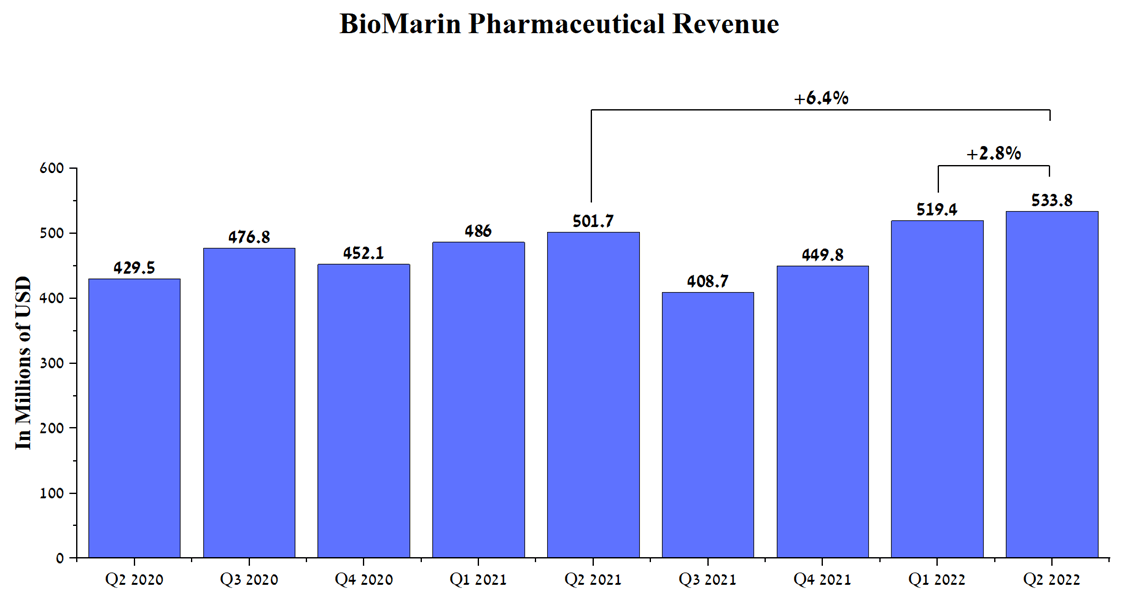

Under the management of Jean-Jacques Bienaime, BioMarin Pharmaceutical’s revenue was $533.8 million in Q2 2022, up 6.4% year-on-year. At the same time, the company’s revenue growth rate does not show a significant acceleration in the last two years, and as a result, BioMarin Pharmaceutical’s share price continues to drift sideways.

Source: Author’s elaboration, based on Seeking Alpha

Despite the temporary weakening of the euro against the dollar, 4 out of 7 medicines of the company showed their former agility in sales growth both year on year and quarterly.

Source: Author’s elaboration, based on quarterly securities reports

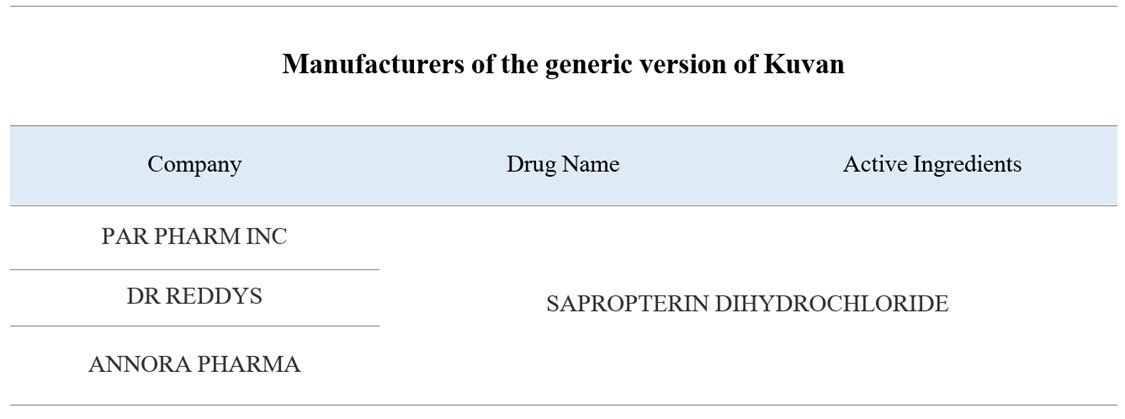

Kuvan (sapropterin dihydrochloride) is a medicine that lowers blood levels of phenylalanine in people with the genetic disorders phenylketonuria or tetrahydrobiopterin deficiency and whose sales represent 11% of the company’s total revenue. The main reason for the decline in sales of Kuvan is the emergence of generic versions of this drug, which have a significantly lower price and, according to the policy of many insurers, they have the preferred status in prescriptions. At the moment, the FDA has approved generic Kuvan from three pharmaceutical companies and I estimate that the number will continue to increase, which will put additional pressure on BioMarin Pharmaceutical.

Source: Author’s elaboration, based on FDA

However, the company’s flagship drug, Vimizim, which was approved for the treatment of people with mucopolysaccharidosis type IVA, partially offset the decline in sales of Naglazyme and Kuvan. I estimate that sales of Vimizim will continue to grow at a CAGR of 18% through 2025 due to continued high interest from physicians in Latin America and Europe and the lack of approved medicines for this therapeutic indication. While the company’s total revenue will reach $2.1 billion in 2022, showing an increase of 13.7% compared to the previous year, and by 2025 this figure will reach $2.79 billion due to increased demand for newly approved medicines.

Source: Created by author

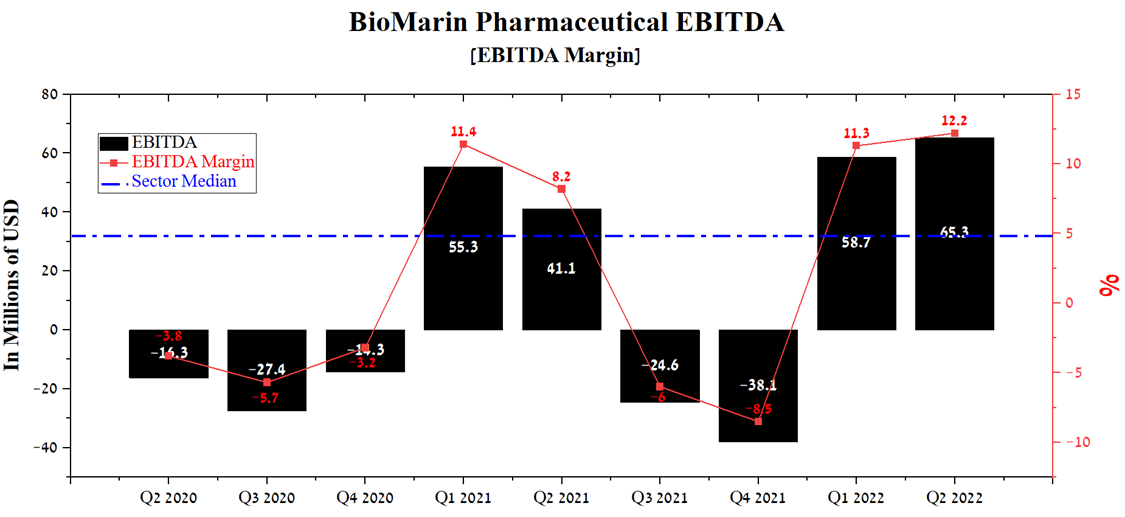

BioMarin Pharmaceutical’s EBITDA was $65.3 million in Q2 2022, up 58.9% year-on-year. Moreover, EBITDA margins continue to improve quarter on quarter, driven by lower production costs while increasing demand for the company’s high-margin products. Thus, this once again shows the ability of BioMarin Pharmaceutical’s management to effectively offset the impact of rising inflation, the weakening of the euro and the Brazilian real against the dollar by maintaining its leading position in the fast-growing orphan drug market.

Source: Author’s elaboration, based on Seeking Alpha

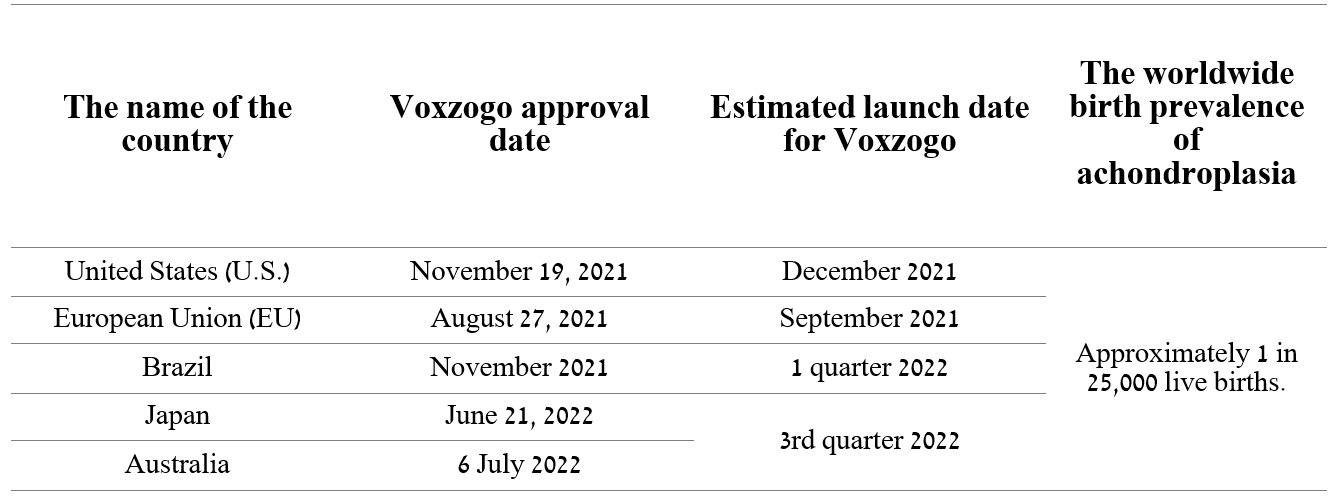

I believe the pace of improvement in this indicator will continue with Voxzogo, which is the first drug to increase linear growth in children with achondroplasia. The medicine was approved at the end of 2021 and the company continues to work actively to bring Voxzogo to new markets.

Source: Author’s elaboration, based on quarterly securities reports

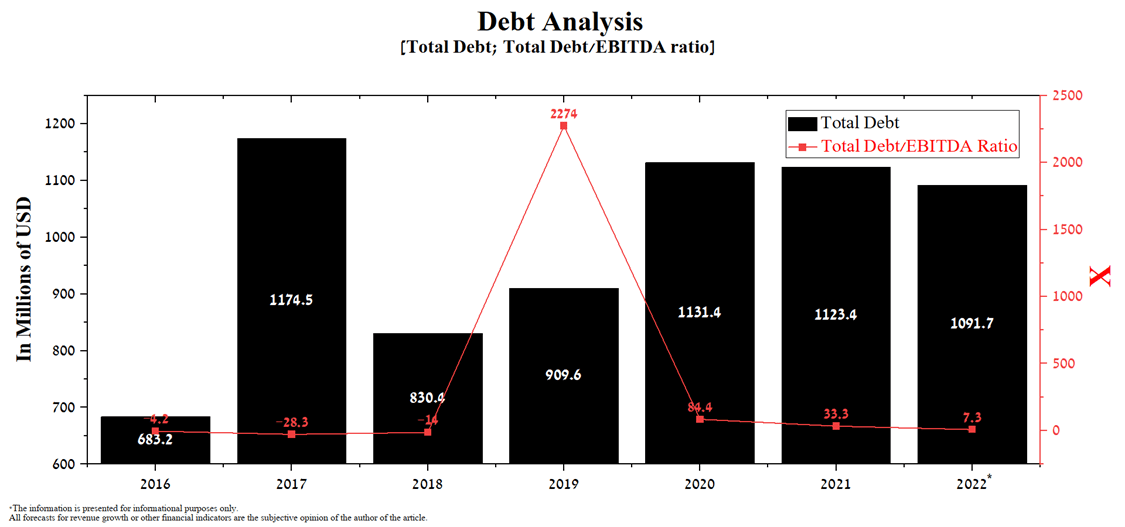

BioMarin Pharmaceutical Debt

At the end of July 2022, BioMarin Pharmaceutical’s total debt was $1,091.7 million, slightly less than in 2021. Despite the decrease in the company’s Total Debt/EBITDA ratio in recent years, it is still significantly more than 3x, which is considered by financiers as an acceptable value. On the face of it, this may indicate that BioMarin Pharmaceutical may face financial difficulties in the future, but the company’s debt consists of convertible notes that can be redeemed not only in cash but also by issuing shares. Thus, the only risk associated with the company’s debt is an increase in the number of shares of BioMarin Pharmaceutical outstanding.

Source: Author’s elaboration, based on Seeking Alpha

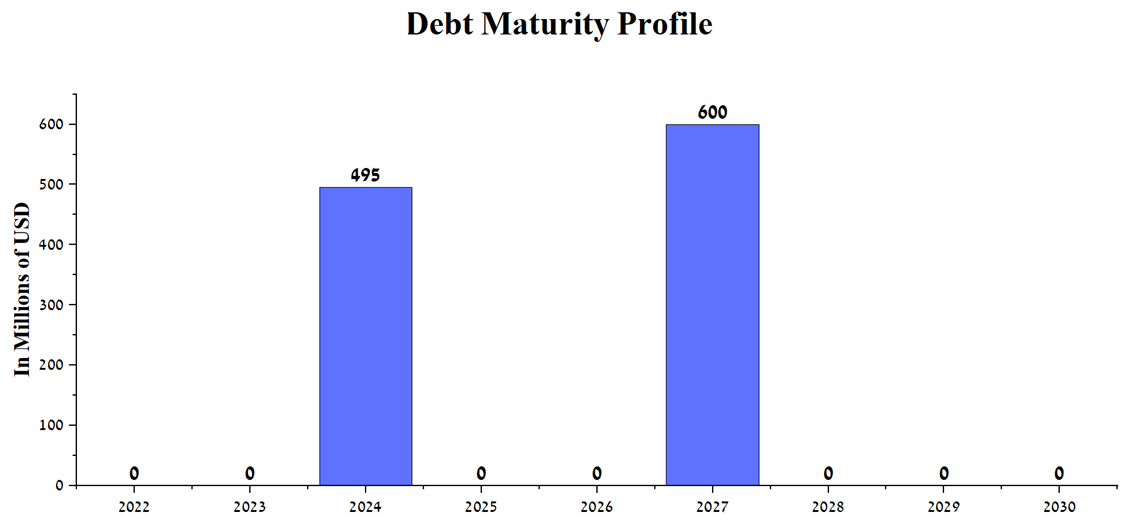

Redemptions of BioMarin Pharmaceutical convertible notes will take place in August 2024 and May 2027, as noted in the chart below.

Source: Author’s elaboration, based on 10-Q

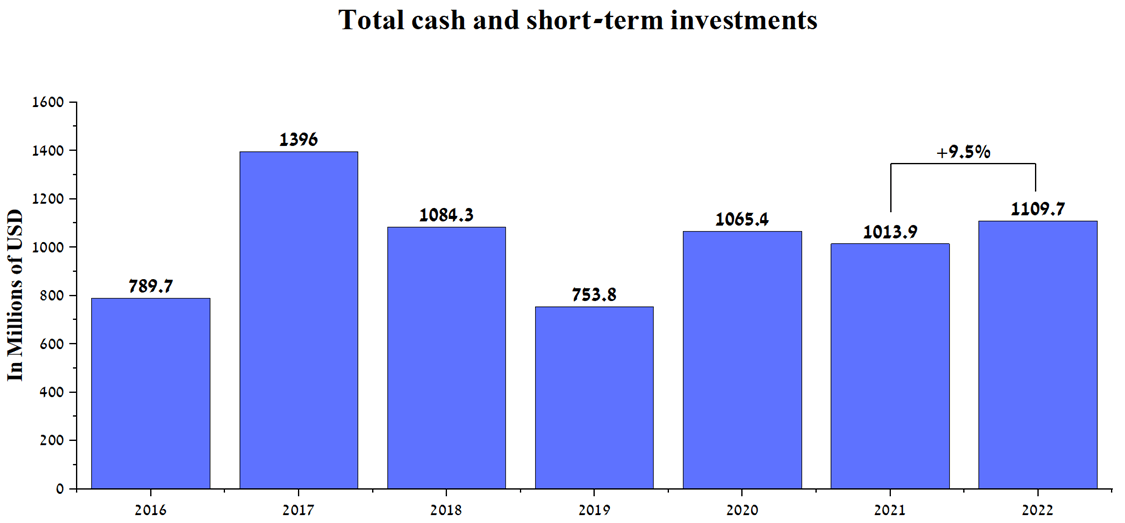

Given the growth in EBITDA and the high level of cash, I estimate that the company will be able to pay off the debt with cash and, as a result, will not have to resort to bond refinancing or equity dilution.

Source: Author’s elaboration, based on Seeking Alpha

Risks

In addition to the significant strengthening of the dollar and high inflation, which threaten macroeconomic stability in the world, in my opinion, there is a risk associated with Roctavian, which will put pressure on the price of BioMarin Pharmaceutical shares in the medium term.

Risks associated with Roctavian

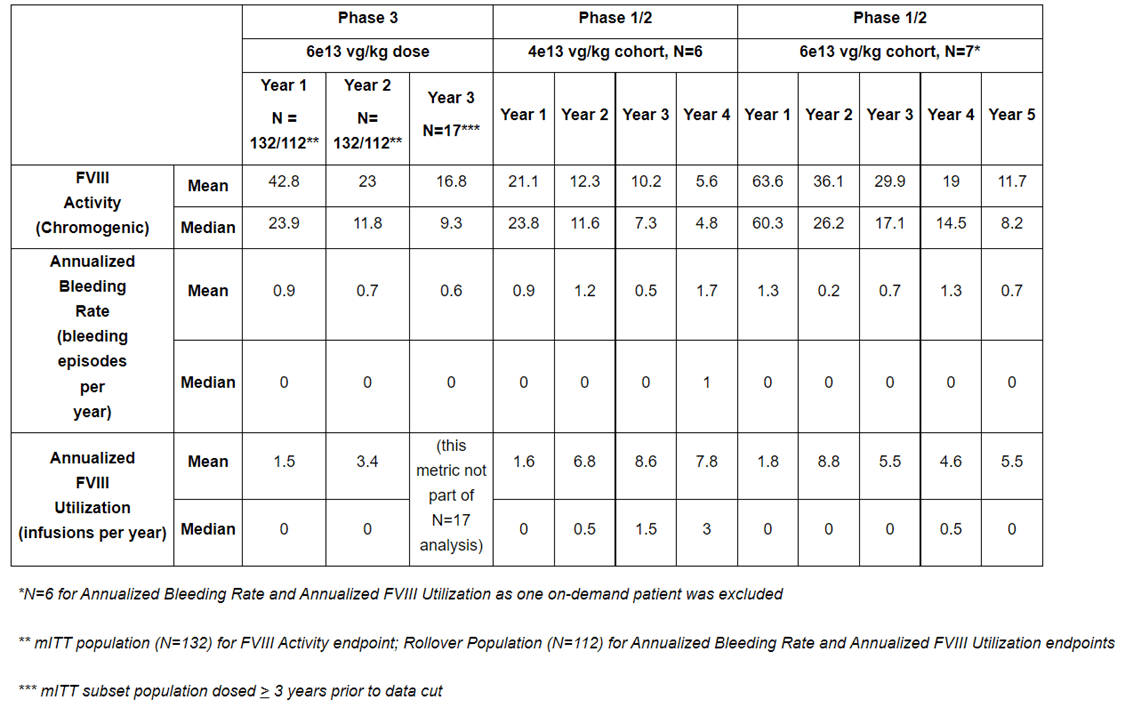

Roctavian (valoctocogene roxaparvovec) is the first gene therapy to be approved by the EMA for the treatment of severe hemophilia A at the end of August 2022. Outside the European Union, the company tried to get approval in the US but was denied by the FDA, resulting in a significant drop in the share price in August 2020. The reason for the refusal was the FDA’s desire to obtain additional data that would confirm the effectiveness of Roctavian in reducing the annual bleeding rate (ABR). In addition, concerns remain about the longevity of this gene therapy due to the continued decline in levels of factor VIII, a blood clotting factor. The normal range for factor VIII is 50-150 IU/dL, and if the level of factor VIII is below 50 IU/dL, then the risk of bleeding increases, and, as a result, the risk to human health increases. In 2022, the company published the results of an ongoing phase 3 clinical trial that at first glance showed that Roctavian controlled bleeding. On the other hand, they disappointed investors and lowered the likelihood of approval due to a 50% reduction in mean factor VIII activity after two years of treatment relative to the first year.

Source: Author’s elaboration, based on BioMarin Pharmaceutical press release

Despite the risk of obtaining a second CRL, on September 29, 2022, BioMarin Pharmaceutical resubmitted the BLA to the FDA. Failure to approve Roctavian in the US would negatively impact the company’s investment case due to a lack of product candidates in Phase 3 clinical trials. But even if the company’s gene therapy gets the green light, it will have to compete with long-acting medicines, namely, Roche Holding’s (RHHBY) (RHHBF) Hemlibra and Sanofi’s (SNY) efanesoctocog alfa showed high efficacy in a pivotal trial.

Conclusion

BioMarin Pharmaceutical is one of the leading pharmaceutical companies in developing innovative treatments for people with rare diseases. Rapidly growing sales of medicines contribute to strengthening the leading position in the orphan drug market and improving the quality of life of people. The company’s price/sales ratio is higher than the average for the healthcare sector, which can be explained by Wall Street’s faith in BioMarin Pharmaceutical’s prospects. BioMarin Pharmaceutical’s revenue growth in subsequent years will reduce this financial ratio and thus increase interest from more conservative investors. However, in my estimation, the existing risks will lead to a short-term correction in the company’s share price to $78 per share. Increasing EBITDA growth rates year on year and the availability of promising product candidates targeting diseases with significant unmet medical need make BioMarin Pharmaceutical an excellent candidate for long-term investors.

Be the first to comment