designer491

Description

I recommend waiting for the macro-environment to turn for the better (for SMBs) before investing in Bill.com (NYSE:BILL). Frankly, I believe BILL stock would work out well over the long-term given its strong value proposition, effective distribution strategy, and the large TAM it is operating in. All is good except we are facing a high possibility of a large recession over the next few months. BILL would definitely be impacted by this recession, causing valuation to fall further – which would give us a better risk/reward opportunity.

Company overview

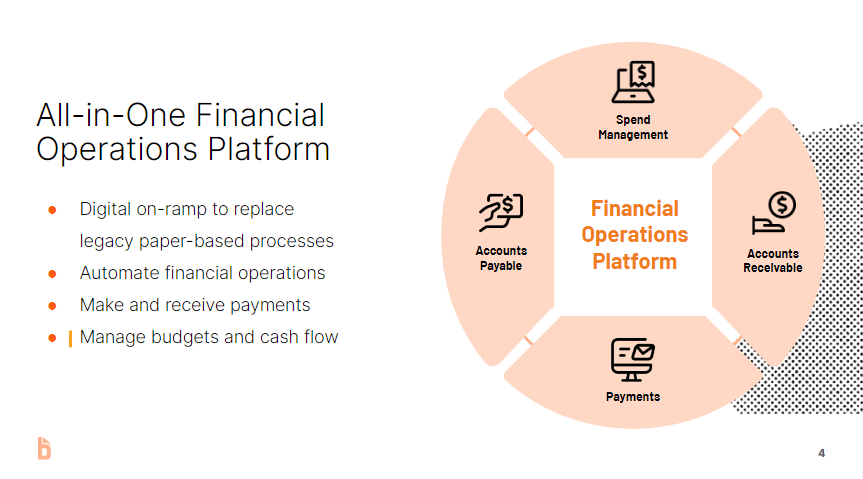

BILL is a suite of cloud-based applications for streamlining, digitizing, and automating small and medium-sized businesses [SMB] financial back-office processes.

Strong secular trends to support BILL long-term growth

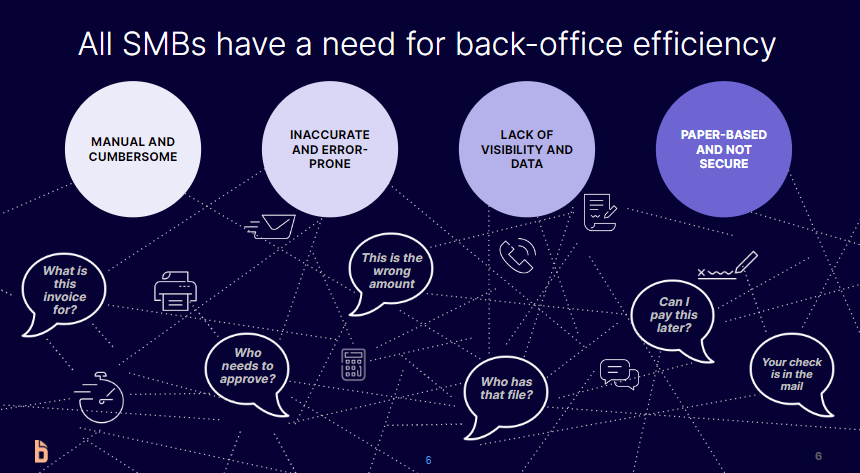

Companies of all sizes, across all sectors and regions, rely heavily on the payment transaction lifecycle. The transaction lifecycle begins with the creation and mailing of invoices and bills, continues through the approval and payment of those bills, and concludes with the recording and reconciliation of those transactions in an accounting system. Any successful enterprise must have the resources and organizational skills to effectively and efficiently manage this essential set of tasks. Yet most companies manage their cash flow in a way that is convoluted, inefficient, and frequently still relies on paper. In particular, this is a problem for SMBs. It has been decades since the typical small business has changed the way they handle their financial processes. A manual, error-prone, insecure, and insight-lacking back office is the result of not having a comprehensive financial software platform designed specifically for SMBs.

Furthermore, I believe that SMBs are not receiving adequate support from current financial software solutions, despite being a significant part of the economy. Many software companies fail to recognize the importance of the SMB market and instead recommend solutions developed for consumers or enterprises. Consumer solutions are too basic, while solutions suitable for large organizations are often overly intricate and pricey. In addition, these products rarely integrate other systems, so SMBs must often purchase a variety of separate products at great expense to meet their requirements. Additionally, SMBs typically do not have enough resources to handle such software solutions, which makes it challenging to reach them through traditional marketing strategies.

Nov’22 deck

Enter BILL cloud-based solution

The cloud-based BILL platform was designed specifically with SMBs in mind. Through its comprehensive nature, the solution automates the administrative tasks of billing, receiving, paying, disbursing, and reconciling. Moreover, BILL offers a centralized and mobile platform for companies to receive payments from customers and pay off invoices. In essence, BILL acts as a hub that brings together buyers and sellers. Popular accounting software, banking institutions, and payment processors can all be accessed from within the platform, streamlining the process for customers. Customers benefit from BILL’s consolidated perspective because it allows them to spot inconsistencies and errors more readily and address them more efficiently. BILL’s integrations ensure that all customer-initiated changes are reflected across platforms without the need for users to manually create files for system updates or maintenance. In addition to saving SMBs a ton of money, BILL gives them access to the same advanced features found in enterprise-level systems.

Nov’22 deck

Effective go-to-market strategy to reach SMBs

BILL adopts a hybrid approach to reach SMBs – direct and indirect.

The direct-to-SMB strategy is complemented by effective inside sales capabilities and makes use of digital customer acquisition solutions. In addition, they promote themselves via word of mouth and face-to-face meetings at industry conventions.

The indirect approach, which is the one I favor, involves making use of accountants and banks. Having a reliable and trustworthy accountant is crucial for SMBs. Since its inception, BILL has been dedicated to equipping accounting firms with resources for superior client management and service. In my opinion, accounting firms can gain an edge in the market, provide better service to their SMB clients, and expand their client advisory services by using the BILL accountant-specific tools. To this day, BILL has partnered with more of a majority of the top accounting firms in the country, making it possible for them to provide increased value to their clients every day. Many of BILL’s customers are initially introduced to BILL by their accountants because of this compelling value proposition.

Instead of relying solely on accountants, SMBs are increasingly turning to financial institutions [FI] for comprehensive cash management solutions delivered via digital channels. In order to better serve their clientele, many of these FI have begun to utilize BILL. By collaborating with BILL, FI can offer their customers the same perks that BILL’s own customers enjoy. Several of the largest FI in the US are currently integrated with BILL. With the BILL platform embedded into the banks online banking solutions, BILL benefits as these partners can offer BILL products to their combined customer base of millions.

Plenty of high margin opportunities available in the tank

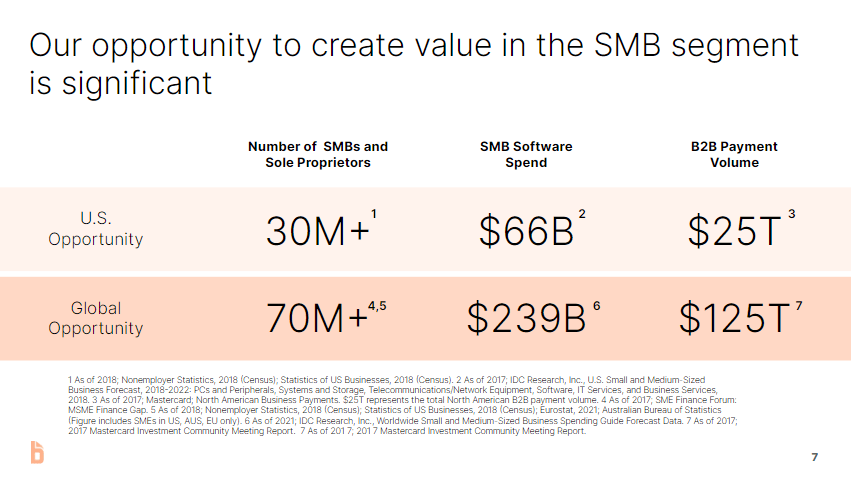

I believe that BILL has a lot of room to grow before it exhausts the $25 trillion B2B payment volume opportunity among US SMBs (1Q23 payment volume represented still represents a fraction of the overall TAM). Furthermore, I believe BILL has the potential to increase the uptake of higher-margin payment products like virtual and corporate cards among both new and existing customers. Specifically, I believe that the company’s corporate card business has significant potential after the acquisition of Divvy. By coordinating their two-sided networks with Divvy’s spend management corporate cards, the combined business will be able to capture high take rate volume and deepen its penetration into its addressable market. Furthermore, since many of BILL’s customers are located in countries other than the United States, I believe there is room for further international development, especially in light of the acquisition of Invoice2Go.

Given BILL’s value proposition, I expect these high margin volumes to eventually account for the majority of its payment volume.

Nov’22 deck

Recent results were good but investors fear the slowdown in the SMB space

BILL’s organic core revenue grew 83% and Divvy’s grew 113%, resulting in 1Q23 revenue of $229.9 million, which was higher than the consensus estimate of $210.5 million. Adjusted operating income of $9.15 million, or 4% operating margin, surpassed expectations of $8.1 million, or 2% operating margin, thanks to the strong top-line beat and higher adjusted gross margins (relative to consensus).

The outcomes were positive, but the market obviously does not share my enthusiasm. Since the earnings report, the stock price has continued to decline. When combined with the slowdown BILL noted last quarter among its mid-market customers, I think this somewhat overshadowed BILL’s very solid beat and raise on the quarter. While concerns about a slowdown in the SMBs market were warranted in advance of earnings, I was heartened to see that BILL was able to beat estimates and increase its dividend in spite of these macro headwinds. This speaks to the power of its value proposition and the organic momentum in its business.

In addition, I think it’s encouraging that they’ve been able to deepen their relationships with some existing partners while also adding new FI partnerships, which bodes well for the expansion of their distribution channels in general. Although the macro outlook is cloudy, BILL is continuing to grow at the highest rate in its industry, maintain positive EBITDA margins, and lead the way in the enormous TAM for B2B payments. The company’s premium valuation and the story of continued optimism are both supported, in my opinion, by the company’s strong organic growth profile.

Valuation

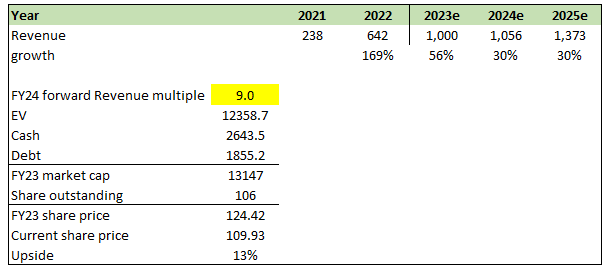

In FY24, I believe BILL could be worth USD124.24, which translates to 13% upside. My model is based on management’s FY23 guidance, and BILL’s ability to continue growing at a high rate (similar to consensus estimates) in this very large TAM. Aside from the large TAM, I believe BILL has several cross/up-selling opportunities that can support this high growth rate.

That said, I think the concern about a near-term slowdown in SMB spending is a real risk that investors should take into account. While BILL managed to outperform despite this risk (as evident by 1Q23 earnings), I believe the near-term share price performance is likely to be pressured until things turn for the better.

Own estimates

Key risks

Competitive AP space

BILL competes in the AP sector of the B2B market, which, in my opinion, is more cutthroat than the AR sector. Competitors with deep pockets include similar platforms, payment processors, banks, and other newcomers to the B2B payment space. When compared to other payment systems, BILL still faces stiff competition from people who are unwilling to abandon their reliance on manual processes and legacy point solutions. In addition to the aforementioned, one could argue that SMB software is the simplest to recreate because there are fewer integrations to deal with.

Exposure to the SMB space

Given that not all bills paid are periodic or maintenance in nature, BILL is vulnerable to the business activity of its buyer and supplier clients thanks to its volume-based revenue model. The inherent cyclicality of BILL is higher because it primarily serves SMBs.

Summary

I would wait for the macro environment to improve (for SMEs) before putting money into BILL. A major economic downturn is a real possibility over the next few months. A further drop in BILL’s valuation due to the recession could present us with an attractive risk/reward scenario.

Be the first to comment