Jetlinerimages/iStock Unreleased via Getty Images

While talks have been ongoing for months, investors who hold The Boeing Company (NYSE:BA) and Airbus SE (OTCPK:EADSY) stock have had to wait a long time for a confirmation of an order from Air India for over 500 aircraft. Finally, today on the 14th of February, Airbus and Boeing received some love from Air India, as the order was confirmed. I’ve been following the news flow for most of the day and one thing is clear, and that is while this is an order that usually gains a lot of attention from the markets, that was not so much the case today.

The reason was that a central stage for confirming the order was absent. During a virtual event in the morning with President Emmanuel Macron of France and Prime Minister Modi of India, the Airbus part of the deal was announced. Later during the day, the White House confirmed the order from Air India for Boeing aircraft. However, it took hours before Airbus and Boeing sent out press releases, taking away some of the momentum of the order announcements which had been saved up to be announced during the Aero India airshow. So, there was an attempt to draw a lot of attention to the order, attention which it deserves, but the execution was rather poor.

In this report, I take a more detailed look than what is available in media reports, looking beyond the list price value and into the market value of the orders, the impact it will have on market shares in the Air India fleet, and why this is order is of significance for Boeing and Airbus investors.

Boeing Order Win Includes 737 MAX, 787 and 777X

Boeing

In total, Boeing is set to win 220 orders. There are, however, three elements to keep in mind. The first thing is that this is a tentative order, which means that after months of negotiations the parties were not able to sign a firm agreement and the deal is pending finalization. This means that it is not at all certain that in Boeing’s February 2023 numbers we will be seeing the order from Air India reflected. Secondly, the tentative order includes a significant number of options that could push the order quantity even higher when firmed.

The last, but to me the most significant, element is that the order includes all key Boeing Commercial Airplanes programs, namely the Boeing 737 MAX, Boeing 787, and Boeing 777X. That is a big sign of confidence in Boeing’s entire product lineup. The deal includes an unspecified number of Boeing 737 MAX 10 jets for which the jet maker obtained a waiver in late 2022. The deal also includes Boeing widebodies, which have not been trouble-free, either. The Boeing 787 deliveries have started flowing since August 2022, when all paperwork and rework sequences were approved by the FAA, so also for that program the order for the Boeing 787 is another sign of confidence after the big boost it already received from United Airlines (UAL).

The passenger variant of the Boeing 777X has been lacking orders, but it seems that with the commitment for the Boeing 777-9 there will be an end to the order drought for another Boeing program that has been plagued by issues and runs years behind on the initial schedule.

|

Boeing Tentative Orders |

||

|

Airplane Model |

Quantity |

List price in $ millions |

|

Boeing 737 MAX 8 |

140 |

$ 17,024 |

|

Boeing 737 MAX 10 |

50 |

$ 6,745 |

|

Boeing 787-9 |

20 |

$ 5,850 |

|

Boeing 777-9 |

10 |

$ 4,422 |

|

Total Value |

220 |

$ 34,041 |

While Boeing did not specify the order mix for the Boeing 737 MAX, I have assumed a 140-50 mix, which brings the list price value to $34 billion. This value is in line with earlier indications found in the media.

It is not the case that list price values are completely meaningless, since once finalized the list price will dictate the down payment, which will be around $340 million. However, it is far more interesting to look at the market values using the evoX Aircraft Price Monitor, because that number is more reflective of the revenue potential. By doing the math, I found that the order is valued closer to $15 billion.

Options Are Also Part Of The Boeing News

Boeing

Besides the firm part of the tentative agreement, Air India has also obtained options to expand its order in the future. In total, the Indian airline has options for an additional 20 Boeing 787-9s and 50 Boeing 737 MAX aircraft, which could add another $5.7 billion to the order value if firmed.

Airbus Order Win Includes A320neo, A321neo and A350

Airbus

Like we saw with Boeing, the Airbus order is also tentative in nature, and it also includes single aisle jets as well as wide body jets, namely Airbus A320neo family aircraft as well as Airbus A350 aircraft. Regarding the Airbus A320neo family program, there really is no concern there from the demand side. Customers are loving the product, and we see Air India ordering more now. Issues only arise from the supply side.

More interesting is the inclusion of the Airbus A350 in the mix, as Airbus did not have an Airbus wide body in the Air India fleet since 2015, when Air India replaced its Airbus A330-200 aircraft with the Boeing 787. With the Airbus A350 being part of the order mix, Airbus is set to rebuild its market share in the Air India widebody fleet from zero. Even more telling, Airbus is capturing a market share on the entire Indian wide body fleet from zero. Furthermore, the Airbus A350 program suffered significant setbacks, and especially its largest variant the Airbus A350-1000 was a slow seller, but this type is also part of the mix. In fact, the bigger Airbus A350-1000 accounts for 85% of the Airbus wide bodies that will be ordered.

|

Airbus Tentative Orders |

||

|

Airplane Model |

Quantity |

List price in $ millions |

|

Airbus A320neo |

140 |

$ 16,701 |

|

Airbus A321neo |

70 |

$ 9,778 |

|

Airbus A350-900 |

6 |

$ 2,054 |

|

Airbus A350-1000 |

34 |

$ 13,440 |

|

Total Value |

250 |

$ 41,973 |

At list prices corrected for inflation towards 2021, the value of the order is $42 billion, but, of course, once again the market values provide a better indication of the value that will be rendered. At market value, the deal would be valued $18.1 billion.

What Is The Air India Deal Worth?

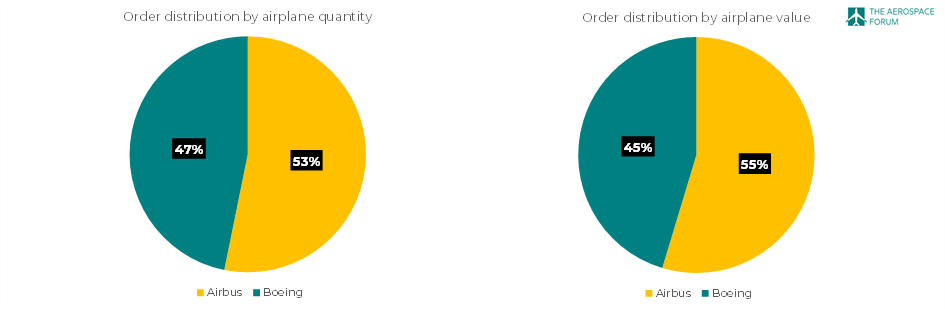

At list prices, the deal is valued around $76 billion plus another $15 billion in options bringing the total catalog value to $88.3 billion. The actual market value of the deal is $33.2 billion plus another $5.7 billion, bringing the market value to nearly $39 billion after discounts, breaking the record for the world’s largest commercial aircraft order in history both in terms of units as well as value.

Boeing vs Airbus: Who Won?

The Aerospace Forum

If we look at the firm part of the tentative order, then there is no doubt that Airbus won. The European jet maker picked up 250 orders compared to 220 orders for Boeing, and the deal that Airbus will be finalizing includes more wide body aircraft. Airbus will be getting 210 single aisle orders out of the 400 single aisle jets, leaving Boeing with 190 orders, while it will scoop an even bigger share of the wide body orders, as it will secure 40 out of the 70 aircraft that are part of the tentative agreement, giving it a 57% share in the wide body orders, leaving Boeing with 43%.

Also in terms of value, Airbus is clearly in the lead, as it is about to secure 55% of the order value measured by actual market values that are more reflective of aircraft sales prices. If you were to add the 70 options for Boeing, it would end up on top when looking at the ordered units as well as the value. The big question is, of course, why those aircraft are not part of the firm part of the agreement, because Airbus managed to sell more aircraft in both segments.

While I don’t want to speculate about the reason why Boeing did not end up making the options part of the agreement in a firm form, I do believe that with the recent big win from United Airlines, the airline is less inclined to be locking in all possible delivery slots, as it in some way also continues to keep hopes on a return of Chinese sales. Being familiar with the aircraft purchase contracts, the options can be firmed until a specified date, after which they expire. There are also purchase right which are also optional in nature, with more leeway for the manufacturer. These days, the term options includes purchase rights as well as the actual options. If Air India secured purchase rights, that would feather in with Boeing’s hopes to sell aircraft to China, and if they can’t, they can still let Air India exercise.

Good News For Boeing and Airbus

Airbus

From a production and inventory standpoint, the order is good news for Boeing as well as Airbus. Both manufacturers will be happy with the deal where Airbus will be winning more than Boeing. While there is no indication that Boeing has remarketed jets that were destined for China that could still be the case. One thing that seems to be certain is that the six Airbus A350-900s are remarketed jets that were initially built for Aeroflot but could not be delivered during sanctions.

A year ago, the demand profile for wide body jets was rather soft, but we now have seen wide body demand tick up, which allowed Airbus to remarket the six jets that it had already built for Aeroflot to Air India. Deliveries of the first of these jets will start in late 2023, which, given the lead times for wide body jet production, is almost certainly enabled by the airframes that were not delivered to Aeroflot.

For production, the orders provide a solid building block for further rate increases from current levels. Particularly the Boeing 777X and Airbus A350, which have not been the fastest sellers are seeing a new customer diversifying the customer pool. With Airbus’ dependency on Qatar Airways and the impact the fall out between those two parties had on the Airbus A350 program, adding a new customer to the pool is of significant value for the stability of the program. Something similar can be said about the Boeing 777X, which is a niche aircraft selected by airlines from the Middle East but not all airlines will be taking the aircraft they ordered. Etihad Airways is an example of that and Emirates has been converting some Boeing 777X orders to orders for the Dreamliner.

Boeing Share In Air India Fleet To Rise

What is also important is to take a look at how the Air India fleet might transform. It is important to consider that Vistara will be integrated into Air India, while Air Asia India (now AIX Connect) will be integrated into the express subsidiary of Air India. So, we need to look at the combined fleet of those carriers and include some near-term deliveries that are not part of this order.

|

Air India Group Fleet |

|

|

Airbus Single Aisle |

152 |

|

Airbus A319ceo |

18 |

|

Airbus A320ceo |

32 |

|

Airbus A320neo |

76 |

|

Airbus A321ceo |

14 |

|

Airbus A321neo |

12 |

|

Boeing Single Aisle |

29 |

|

Boeing 737-800 |

29 |

|

Boeing Wide Body |

54 |

|

Boeing 777-200LR |

7 |

|

Boeing 777-300ER |

13 |

|

Boeing 787-8 |

27 |

|

Boeing 787-9 |

7 |

|

Airbus Total |

152 |

|

Boeing Total |

83 |

|

Total |

235 |

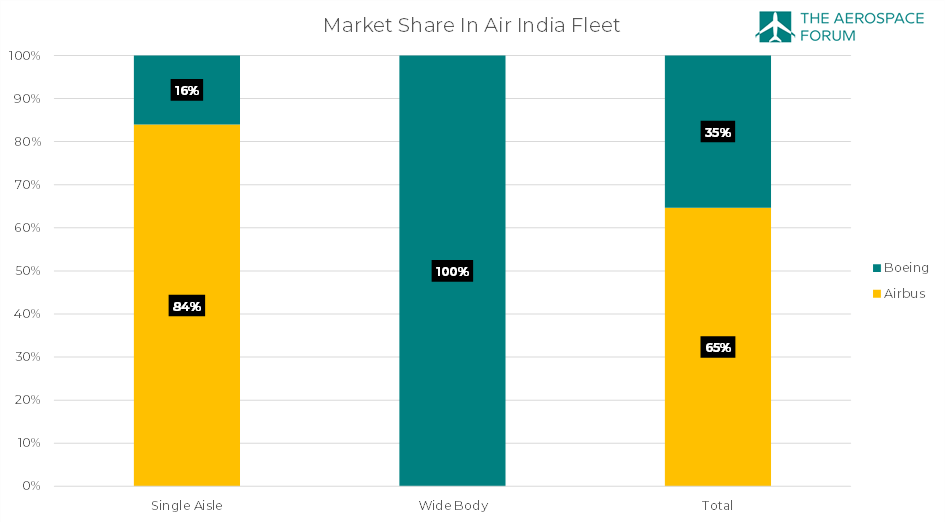

Including its subsidiary Air India Express and airlines that will be integrated, the Air India Group, excluding its regional airline, is a fleet of 235 aircraft comprising of 64 Airbus A320ceo and 88 Airbus A320neo family airplanes and 29 Boeing 737 airplanes, for a total of 181 single aisle jets. The wide body fleet is comprised of 20 Boeing 777 airplanes and 34 Boeing 787 airplanes for a total of 54 wide body aircraft. The fleet consists for 23% of wide body jets and 77% of single aisle jets.

The Aerospace Forum

Looking at the market share for Boeing and Airbus in each segment, we see that Airbus dominates the single aisle segment with a share of 84%, while Boeing exclusively provides the wide body capacity of Air India. Overall, Airbus dominates with a 65% market share in the fleet due its strong value proposition for both generations of the Airbus A320 family. What also becomes clear is that with the current order composition, Airbus cannot maintain its share in the single aisle segment, and Boeing cannot maintain its share in the wide body segment.

One can expect that the older generation aircraft – meaning the Boeing 737-800 and Airbus A320ceo family aircraft – will be replaced over time by the Airbus A320neo and Boeing 737 MAX, while the Airbus A350-900 seems a fitting replacement for the Boeing 777-200LRs and the Airbus A350-1000 or even the Boeing 777-9 provide a desirable replacement for the Boeing 777-300ER.

The Aerospace Forum

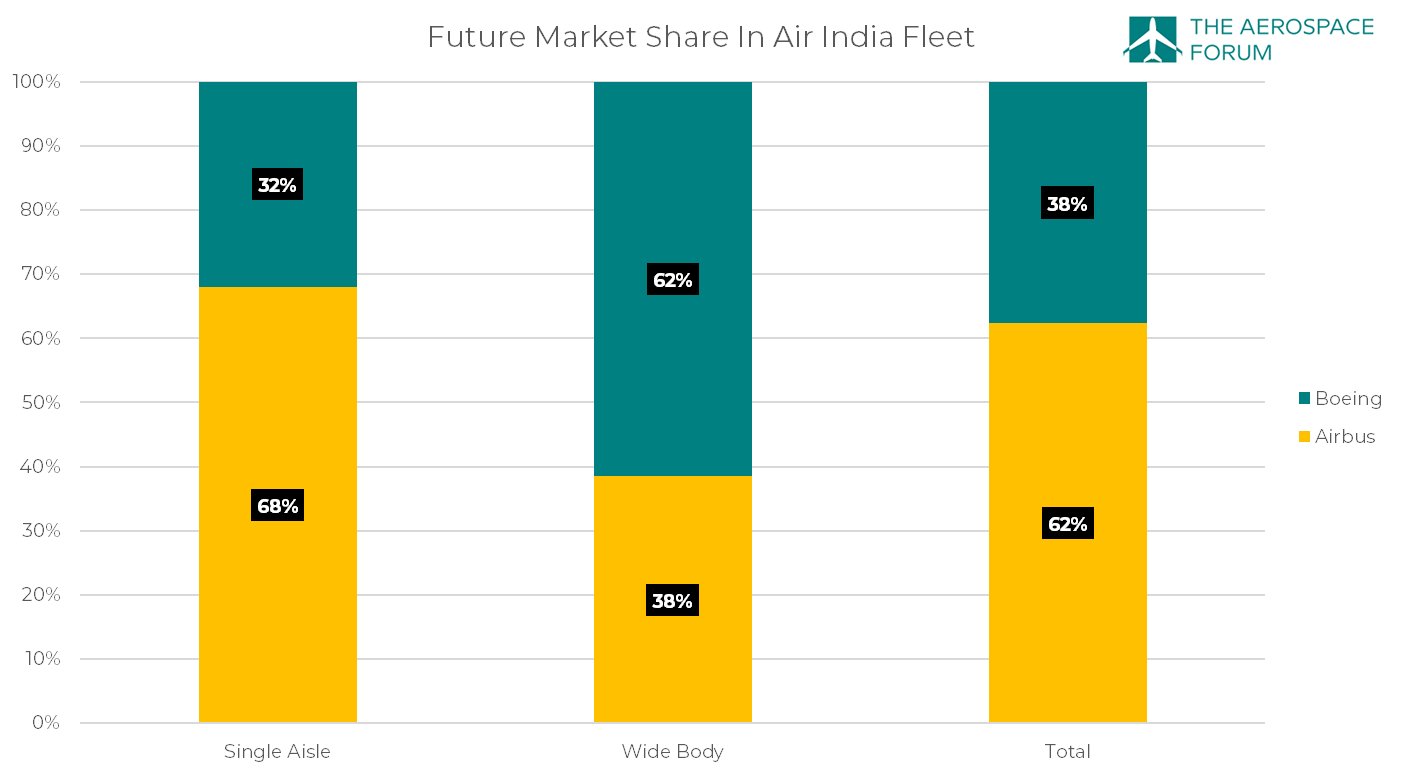

If we look at how the share in the future fleet will shift, we see that Boeing will double its share in the single aisle fleet to 32%, while it will lose 38% in the wide body fleet. In total, that will bring the market share of Boeing in the Air India fleet to 38%, up from 35%. You could, of course, say “well, is it worth it to lose the exclusivity in the wide body segment” for a 3 percentage point gain in market share. I will leave that up to the reader to debate.

The single aisle fleet has a lot of growth potential due to the domestic market in India, which keeps growing, so getting orders in that segment is a big plus. I don’t believe that Airbus will be too bothered by the Boeing orders in the single aisle segment because, in some ways, the U.S. jet maker is just recouping some ground that it lost on the Indian aircraft market earlier.

On the wide body side, Airbus booked a big win. There is really doubt about that. In a previous report where I countered the argument that the Indian market could be replacing missed sales to China for Boeing, I already pointed out that Boeing would be losing market share in the Indian wide body segment, and it had fallen behind in recent years on the Indian single aisle market:

It is not immediately clear, but on the wide body market, Boeing has a 100% market share in India. So, any widebody sale, like the one of which Faury and Modi had a scale model on the table, that Airbus is going to make it will help them gain market share. So, why do I say that Boeing is fighting its own battle in India? There are two reasons for that. The first one is that obviously with an ideal duopoly, the share should be closer to 50% and as can be seen it is nowhere near those levels. Secondly, when analyzing the market share 5 years ago, it became clear that Boeing had a 67% share on the single aisle market. So, over the past five years, Boeing has lost market share in India.

I think, overall, Boeing would have loved to be able to sell at least 20 Boeing 777-9 airplanes and 20 Dreamliners to Air India.

Will Airbus and Boeing Stock Price Rise?

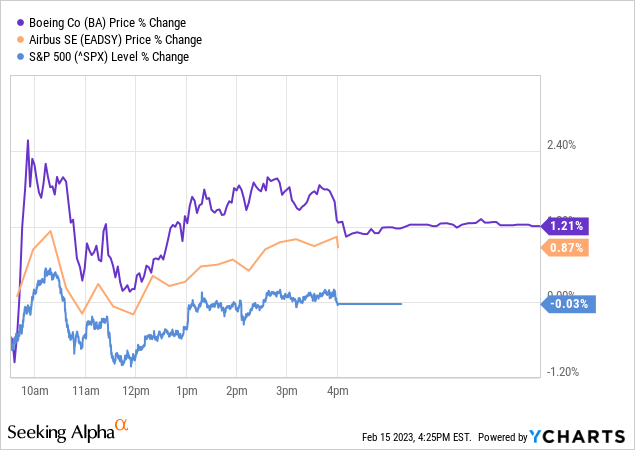

Generally, I believe that aircraft orders should not affect share prices, because at the time of announcement, and even more so in this case since this is a tentative agreement, no value is rendered and rendering the value happens over multiple years. The reality is that shares prices did rise. While the broader markets had a choppy trading session ending more or less flat due to disappointing CPI readings sparking concerns that the Fed might continue to raise hikes, shares of Boeing rose and so did the ADS of Airbus.

Generally, the sentiment here is that Airbus is the winner because it gained more tentative orders and it is making inroads on the wide body market share of Boeing in India. However, one thing that is omitted by everyone is that the other way around Boeing is significantly gaining market share in a market that could grow significantly in the years to come. I think the share price reflects just that, you are not losing with either company as an investment.

Conclusion: Boeing and Airbus Stock Remain A Buy

While there often is a strong sentiment or preference for either Boeing or Airbus, the reality is that over the longer term you are unlikely to lose holding either name. If you are too conflicted by certain sentiments, you capture only half of the market, while if you are invested in both names, just like I am you are taking 100% of the success home for a growing market segment.

What we have been seeing for a while now is upward pressure on production rates from the demand side, and the Air India order validates that upward pressure not only for single aisle aircraft but also for wide body aircraft. Boeing expects to significantly increase Boeing 787 production rates to 10 aircraft per month by the middle of this decade, while Airbus is also aiming to increase production rates for its Airbus A330 and Airbus A350 programs.

The order from Air India shows the continued appeal of both product lineups, with Boeing gaining share in the single aisle market in India while Airbus gains share in the wide body market. As said, if you are a shareholder in both names, these are good times, as we see wide body demand ticking up and single aisle demand remaining strong. The Air India order reflects just that: a rewarding buy for Boeing and Airbus.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment