naphtalina/iStock via Getty Images

National Retail Properties (NYSE:NNN) and W. P. Carey (NYSE:WPC) are high yield triple net lease REITs with investment grade credit ratings. WPC places a greater focus on industrial real estate, Europe, and inflation-linked leases, whereas NNN pursues faster growth and a more conservative balance sheet. In this article, we compare them side by side and offer our take on which is a better buy right now

National Retail Properties Vs. W. P. Carey: Business Model

Both WPC and NNN are triple net lease REITs, which means that the vast majority of their properties are single tenant free-standing real estate. This has proven over time and across cycles to be a very low risk method for building wealth through real estate thanks to its generally stable performance and high occupancy rates regardless of macroeconomic conditions. The reason for this is simply that in the typical triple net lease, the tenant is solely responsible for paying the expenses associated with insuring, operating, and maintaining the property. On top of that, these leases are typically long-term and are difficult and costly for the tenant to break.

That similarity aside, NNN focuses more on retail real estate in the United States whereas WPC focuses more on industrial and warehouse real estate in both the United States and Europe. WPC also has meaningful office and personal storage real estate exposure as well.

NNN employs very conservative underwriting standards with rent coverage that generally fits in the 2-3x range while also prioritizing owning real estate in great locations and a high land value component as opposed to targeting investment grade tenants. NNN also owns 3,349 properties diversified across 48 states and over 380 national and regional retail tenants. This gives it a very stable cash flow profile, enabling it to steadily grow its cash flow per share and achieve Dividend Aristocrat status with 33 consecutive years of dividend growth. NNN’s excellent underwriting is evidenced by its 99.4% current occupancy rate and very stable performance in the face of major macro disruptions such as the Great Financial Crisis and COVID-19 outbreak and lockdowns.

WPC, meanwhile, owns 1,428 properties that are diversified across 391 different tenants and North America and Europe. Roughly one-third of its rent comes from investment grade tenants, and it takes great care to ensure that its properties are well-located and serve a mission-critical role for tenants. It also mostly owns recession and e-commerce resistant assets. Another key focus for WPC is that the majority of its ABR is CPI-linked, giving it some of the best inflation protection in its sector. On top of that, roughly half of its ABR comes from industrial and warehouse properties and only 16% of its ABR comes from retail real estate. It weathered the COVID-19 lockdowns better than perhaps any other triple net lease REIT and has increased its dividend per share every year since 1998, putting it on the cusp of Dividend Aristocrat distinction.

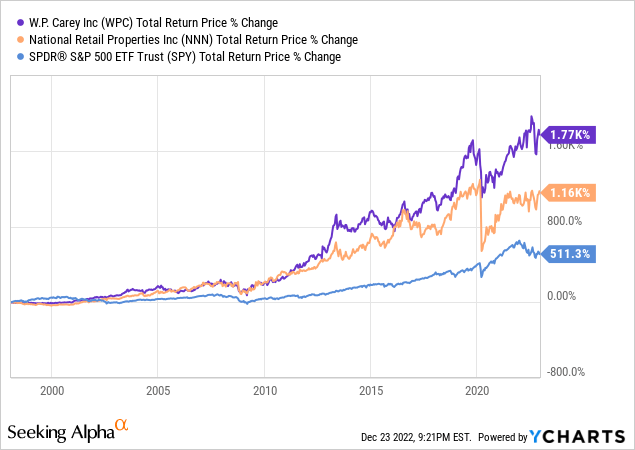

Both business models have proven highly lucrative for long-term investors as both REITs have significantly outperformed the market over time:

National Retail Properties Vs. W. P. Carey: Balance Sheet

NNN has one of the strongest balance sheets in the triple net lease sector as evidenced by its BBB+ credit rating, substantial liquidity, and well-laddered debt maturity schedule. As a result, it enjoys a reasonably attractive cost of capital that enables it to grow via acquisition accretively.

WPC slightly trails NNN in the credit rating department at BBB, but it has a positive outlook from S&P so it clearly is in solid financial shape. Like NNN, it has plenty of liquidity and a well-laddered debt maturity schedule, so it is at little risk of financial distress anytime soon. An added bonus for WPC is that its sizable presence in Europe gives it access to debt in a currency (Euros) that has lower interest rates, giving it greater flexibility in raising debt to finance new growth opportunities.

National Retail Properties Vs. W. P. Carey: Dividend Outlook

Moving forward, neither REIT has a robust growth outlook, as WPC is only expected to grow its AFFO per share at a 2.7% CAGR through 2025 and NNN is only expected to grow its AFFO per share at a 1.7% CAGR over that same span. Dividends per share growth at WPC is expected to be very anemic at just a 0.8% CAGR through 2025 and NNN’s dividend per share CAGR over that span is expected to be an unimpressive 2.7%. This is due to a combination of a high cost of capital at the moment due to higher interest rates, stubbornly low cap rates across the industry, and significant upcoming lease expirations for WPC.

National Retail Properties Vs. W. P. Carey: Valuation

When comparing these REITs side-by-side, we see that NNN is slightly cheaper than WPC, though WPC does offer a high dividend yield:

| Metric | P/AFFO | FWD Dividend Yield | EV/EBITDA | P/NAV |

| WPC | 14.99x | 5.4% | 17.32x | 1.10x |

| NNN | 14.09x | 4.9% | 16.45x | 1.05x |

Investor Takeaway

Overall, we think that WPC is a better pick for investors looking for industrial exposure, European exposure, and greater inflation protection. Meanwhile, NNN offers investors more predictable growth and greater concentration in U.S. single tenant free-standing retail. WPC also offers investors a 50 basis points higher forward dividend yield, while NNN trades at a slightly cheaper valuation.

At the moment, we favor WPC in our risk-averse Retirement Portfolio given its greater diversification across industries and geographies, its greater inflation protection, and its higher current dividend yield. In our more aggressively dispositioned Core Portfolio, we have other triple net lease REITs that we like more than both WPC and NNN from a total return perspective, so we hold neither there. We rate both NNN and WPC a Buy and think one or both could serve well as a component in a high yield and/or dividend growth portfolio.

Be the first to comment