olaser

Enterprise Products Partners (NYSE:EPD) and Magellan Midstream Partners (NYSE:MMP) are two high yield midstream businesses that boast sector-leading credit ratings.

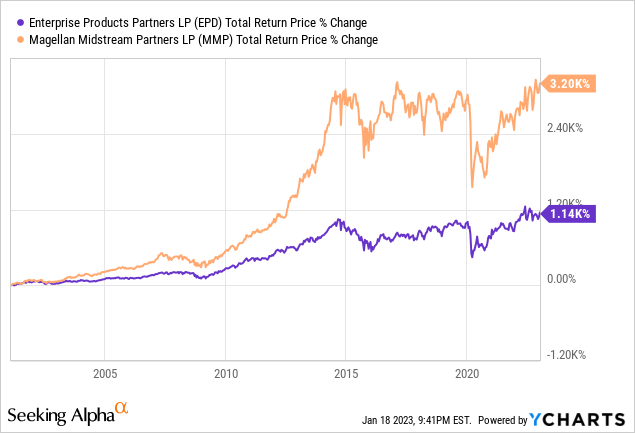

While MMP has a much better long-term track record:

EPD trades at a significant valuation multiple discount to MMP at the moment.

In this article, we will compare them side by side and offer our take on which one is a better buy.

Magellan Midstream Partners Vs. Enterprise Products Partners: Business Model

MMP is known for its top-tier refined products midstream assets that have been built and managed expertly under MMP’s stewardship. As a result, it is unsurprising that the business has generated sector-leading average annualized returns on invested capital of 16% over a 15-year period.

MMP’s long-term contracts and 85% cash flow exposure to commodity price resistant fee-based contracts gives it a very stable cash flow profile through nearly all market cycles and energy industry conditions.

Meanwhile, EPD’s asset portfolio is much more diversified than MMP’s and is in fact arguably one of the very best positioned in the entire midstream sector. Its merits include:

- Its network is connected to every major shale basin and every ethylene cracker in the United States as well as to 90% of the refineries located east of the Rockies.

- It also owns strategically located Gulf Coast export facilities.

- Its NGL network is comprehensive in its scope and provides significant access to Mont Belvieu.

- It has a vaunted petrochemical business.

- Its natural gas pipeline network flows through Louisiana, Texas, and New Mexico and connects to major demand centers while also providing significant net gas processing capacity.

- Its crude pipeline network flows through New Mexico, Texas, and Oklahoma and connects numerous major export hubs.

- It operates a highly successful marketing business that enhances EPD’s returns on its pipeline network.

Like MMP, EPD enjoys a very stable cash flow outlook with 15+ year contracts attached to many of its key assets and a low percentage of its cash flows stemming from commodity price sensitive assets.

Overall, we give a very slight edge to EPD here merely due to its superior scale and diversification. That said, it is hard to argue against the high level of profitability and long-term track record of MMP’s assets.

Magellan Midstream Partners Vs. Enterprise Products Partners: Balance Sheet

With industry-leading BBB+ credit ratings, both EPD and MMP clearly have sound balance sheets.

MMP employs a very conservative approach to capital allocation by maintaining modest leverage, plenty of liquidity, and recently has sold several non-core assets and used the proceeds to reduce debt and buy back common equity at opportunistic prices. Furthermore, its debt maturity schedule is very advantageous with none of its long-term debt maturing prior to 2025. Perhaps most impressive is the fact that a whopping 83% of its total net long-term debt matures in 2030s or later with the significant majority of it not maturing until 2042 or later. As a result, it has locked in low interest rates for many years to come and will suffer little to no negative impacts from the current rising interest rate environment.

EPD’s balance sheet is every bit just as strong, and in fact, we would argue it is even stronger. First and foremost, it boasts a 3.1x leverage ratio that is well below its already conservative target range of 3.25x – 3.75x. Furthermore, it has plenty of liquidity at $3.3 billion alongside a weighted average debt term to maturity of 20 years.

Magellan Midstream Partners Vs. Enterprise Products Partners: Distribution Outlook

Both businesses have very impressive distribution track records. EPD is on the verge of hitting 25 consecutive years of distribution per unit growth whereas MMP has 22 consecutive years of distribution per unit growth. Both are expected to grow their distributions/dividends at a low to mid-single digit annualized rate in the years to come. EPD’s distribution per unit is expected by the Wall Street analyst consensus to grow by 4.5% in 2023 and 4% in 2024. MMP’s distribution per unit is expected by the Wall Street analyst consensus to grow by 1.3% in 2023 and 1.2% in 2024.

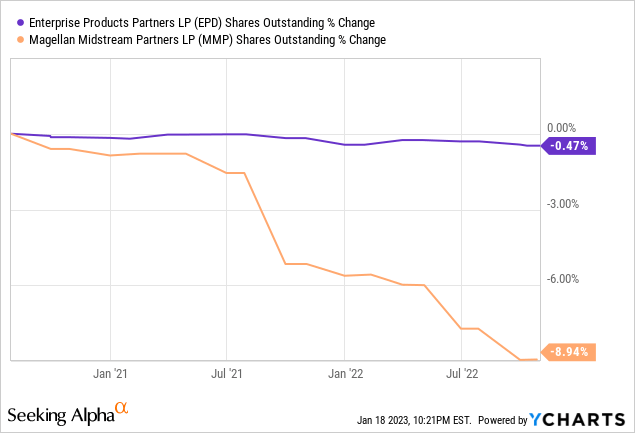

While EPD’s distribution growth rate is expected to surpass MMP’s in the coming years, it is important to note that MMP is also pursuing a more aggressive unit repurchase program than EPD is. This is evidenced in the following graph showing the change in units outstanding over the past two and a half years:

Magellan Midstream Partners Vs. Enterprise Products Partners – Distribution Safety

MMP’s coverage ratio is currently 1.37x given that it is expected to pay out a $4.22 annualized distribution and is expected to generate $5.79 in distributable cash flow in 2023.

Meanwhile, EPD’s coverage ratio is currently 1.75x given that it is expected to pay out a $1.99 annualized distribution and is expected to generate $3.48 in distributable cash flow in 2023.

Given that we view EPD’s balance sheet as being stronger than MMP’s, we view EPD’s distribution as the safer of the two. However, both distributions appear to be very safe for the foreseeable future, so there is little concern with either distribution.

Magellan Midstream Partners Vs. Enterprise Products Partners – Catalysts And Risks

EPD and MMP are both heavily tied to the performance of the crude oil and refined products sectors. As a result, if the energy transition accelerates faster than expected, it could negatively impact the intrinsic value of EPD and MMP.

On the other hand, EPD is well diversified across other midstream subsectors while MMP’s assets are among the very best and are positioned in geographies (i.e., the midwestern U.S.) that are deemed to be more resistant to the energy transition.

Magellan Midstream Partners Vs. Enterprise Products Partners: Valuation

On a valuation basis, EPD appears to be the clear winner with significantly cheaper EV/EBITDA and P/DCF multiples. That said, both look quite undervalued relative to their respective histories on an EV/EBITDA basis and MMP does offer a slightly higher distribution yield, so we think both are attractive buys at current prices.

|

MMP’s Metrics |

Current | 5-Yr. Average |

| EV/EBITDA | 10.7x | 11.8x |

| P/2023E DCF | 9.0x | NA |

| Distribution Yield | 8.0% | 7.9% |

| EPD’s Metrics | Current | 5-Yr. Average |

| EV/EBITDA | 9.4x | 10.5x |

| P/2023E DCF | 7.3x | NA |

| Distribution Yield | 7.7% | 7.6% |

Investor Takeaway

This is definitely a case where buying both could be considered the most reasonable option, especially if you do not mind dealing with K-1s (both issue them).

MMP is a simpler investment thesis, with management running a very lean capital expenditure budget and allocating virtually all distributable cash flow to distributions and unit repurchases. Furthermore, the asset portfolio has been pruned in recent years to focus only on its most core and highest returning businesses, resulting in a very stable cash flow profile and a business that should remain very profitable for many years to come.

EPD is pursuing a more aggressive growth capital expenditure course given its superior opportunities across its diversified business model. As a result, it will be putting lesser emphasis on unit repurchases relative to MMP’s for the foreseeable future. That said, the valuation is cheaper here, the leverage ratio is lower, and the distribution growth prospects are a little better here. It also does not hurt that insiders own about one-third of the partnership, making them very vested in the common equity’s success.

We rate both businesses a Buy at the moment, but favor EPD between the two for inclusion in our Retirement Portfolio at High Yield Investor.

High Yield Investor Portfolio

Be the first to comment