adaask

Both Oaktree Specialty Lending (NASDAQ:OCSL) and Ares Capital (NASDAQ:ARCC) are high-yield business development companies (i.e., BDCs) with investment grade balance sheets. Both also have strong underwriting performance thanks to their backing by leading alternative asset managers in Ares Management (ARES) and Brookfield Asset Management’s (BAM)(BN) Oaktree Capital.

In this article, we will compare them side by side and offer our take on which one is a better buy at the moment.

Ares Capital Vs. Oaktree Specialty Lending – Balance Sheet

Both ARCC and OCSL have some of the stronger balance sheets in the BDC sector, enjoying investment grade credit ratings and plenty of access to capital at reasonable cost.

ARCC’s leverage ratio is not low but is still manageable at 1.27x. Meanwhile, it enjoys substantial liquidity of $4.5 billion (21% of its enterprise value).

OCSL’s debt-to-equity ratio is on the lower end of the spectrum for BDCs at 1.08x, and the company has sufficient liquidity of $524 million (20% of its enterprise value).

Overall, we give the edge to OCSL here as its leverage ratio is considerably lower than ARCC’s, giving it greater flexibility to leverage up opportunistically as well as a better cushion against a surge in non-accruals and defaults on loans.

Ares Capital Vs. Oaktree Specialty Lending – Business Models

OCSL has much greater exposure to first lien senior loans than ARCC does at 71% vs. 45%. It has 16% exposure to second lien senior secured loans compared to 18% exposure for ARCC. Overall, this gives OCSL a greater exposure to senior secured loans than ARCC with 87% exposure vs. just 63% exposure. As a result, OCSL is more conservatively positioned than ARCC is. Slightly more of OCSL’s loans are floating rate than ARCC’s are, but it is important to note that OCSL’s debt is significantly more exposed to rising interest rates than ARCC’s is, so overall ARCC is more positively exposed to rising interest rates.

Both companies also adopt a relatively defensive posture in regards to their sector selection. ARCC has 23% exposure to software and 10% exposure to healthcare as its top two industries. OCSL has 15.4% exposure to software and 13% exposure to healthcare as its top two industries.

It is also worth noting that OCSL has zero non-accruals in its portfolio whereas ARCC does have some (1.6% at cost).

Overall, we give OCSL the edge in terms of portfolio defensiveness in the current environment. While ARCC will benefit more if interest rates continue to rise, OCSL is better positioned to enjoy stable earnings if the Federal Reserve pivots to cutting interest rates.

Ares Capital Vs. Oaktree Specialty Lending – Dividend Outlook

Both businesses are booming at the moment and experiencing strong earnings per share growth thanks in large part to rising interest rates, which in turn is driving dividend growth.

Analysts expect ARCC to generate a 3.7% dividend per share CAGR supported by a 5.7% CAGR in earnings per share through 2024.

Meanwhile, OCSL is expected to grow its dividend per share at a whopping 7.7% CAGR through 2024, while earnings per share are expected to grow at a nearly equally impressive 7.3% CAGR over that same time span.

Given these projections, the balance sheet and portfolio strength, and positive exposure to rising interest rates at both BDCs, both dividends appear to have attractive outlooks moving forward, barring a deep recession that would cause defaults to soar and interest rates to plummet. Both management teams have discussed this on recent earnings calls.

For example, ARCC’s management recently said:

We elected to raise the regular quarterly dividend from $0.43 to $0.48 per share because the company is now experiencing a higher level of core earnings, primarily due to the substantial increase in base rates. This increase, the largest quarterly increase in our company’s history, is our third increase this year and results in a regular dividend that is 17% higher than our regular quarterly dividend level at the end of 2021.

The higher base dividend that we are paying also reflects our positive outlook on our ability to generate this level of core earnings under a variety of interest rate and economic scenarios for the foreseeable future.

On its latest earnings call, OCSL’s management announced:

we are well positioned for the year ahead as rising interest rates have bolstered the earnings power of our portfolio. 86% of our loans are floating rate, and we expect our interest income will continue to rise in tandem with increasing base rates.

Given the strength and consistency of our earnings as well as the potential for continued solid results, our Board increased our quarterly dividend by 6% to $0.18 per share. This was the tenth consecutive quarterly increase and represented a 16% increase from the distribution we announced a year earlier. Notably, our dividend is up nearly 90% from its pre-pandemic level at the close of fiscal 2019.

Our Board also declared a special distribution of $0.14 per share, primarily as a result of increased taxable income derived from our foreign exchange hedge positions as well as certain taxable equity gains.

While ARCC’s expected dividend growth rate is not as high as OCSL’s, investors should keep in mind that it has a longer track record of sustaining and growing its dividend over time and has also been more aggressive and consistent with paying out special dividends. That said, we still give OCSL a slight edge here.

Ares Capital Vs. Oaktree Specialty Lending – Valuation

Based on the numbers below, OCSL and ARCC are valued virtually identically with both stocks priced at the very same (very slight) premium to NAV and identical projected forward dividend yields.

| Valuation Metric | OCSL | ARCC |

| Price to NTM Normalized Earnings | 8.37x | 8.47x |

| NTM Dividend Yield | 10.6% | 10.6% |

| P/NAV | 1.01x | 1.01x |

Investor Takeaway

OCSL is probably the better buy right now thanks to its lower leverage, better growth outlook, stronger underwriting performance, and greater concentration in senior secured debt (especially first lien loans).

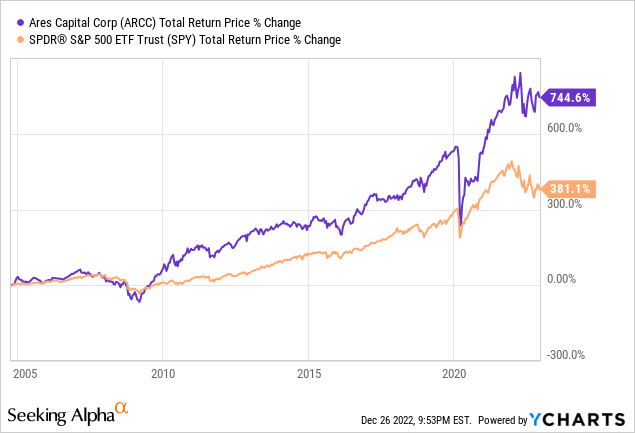

That said, we think both are solid investments at the moment with ARCC boasting a very impressive long-term track record across cycles giving it considerable appeal and its management a significant trust factor in the current environment:

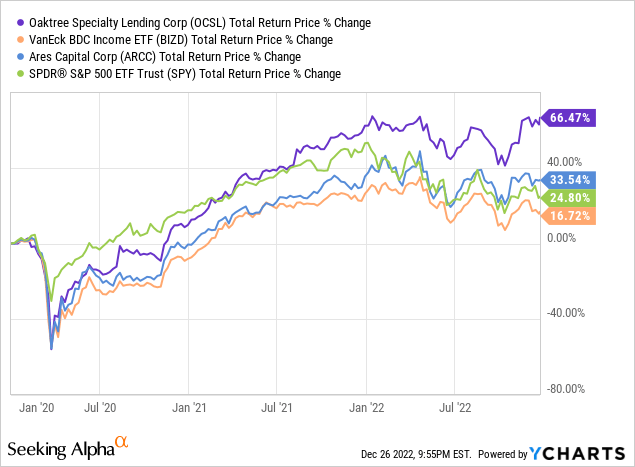

Still, OCSL has thrived under Oaktree management and its total return performance over the past three years (including the COVID-19 crash) has been phenomenal as management has successfully closed its discount to NAV while aggressively growing its dividend:

We rate both stocks as Holds at the moment and Buys on dips to discounts to NAV. You can read our full ARCC investment thesis here and our OCSL investment thesis here.

Be the first to comment