Elena Bionysheva-Abramova/iStock via Getty Images

Introduction

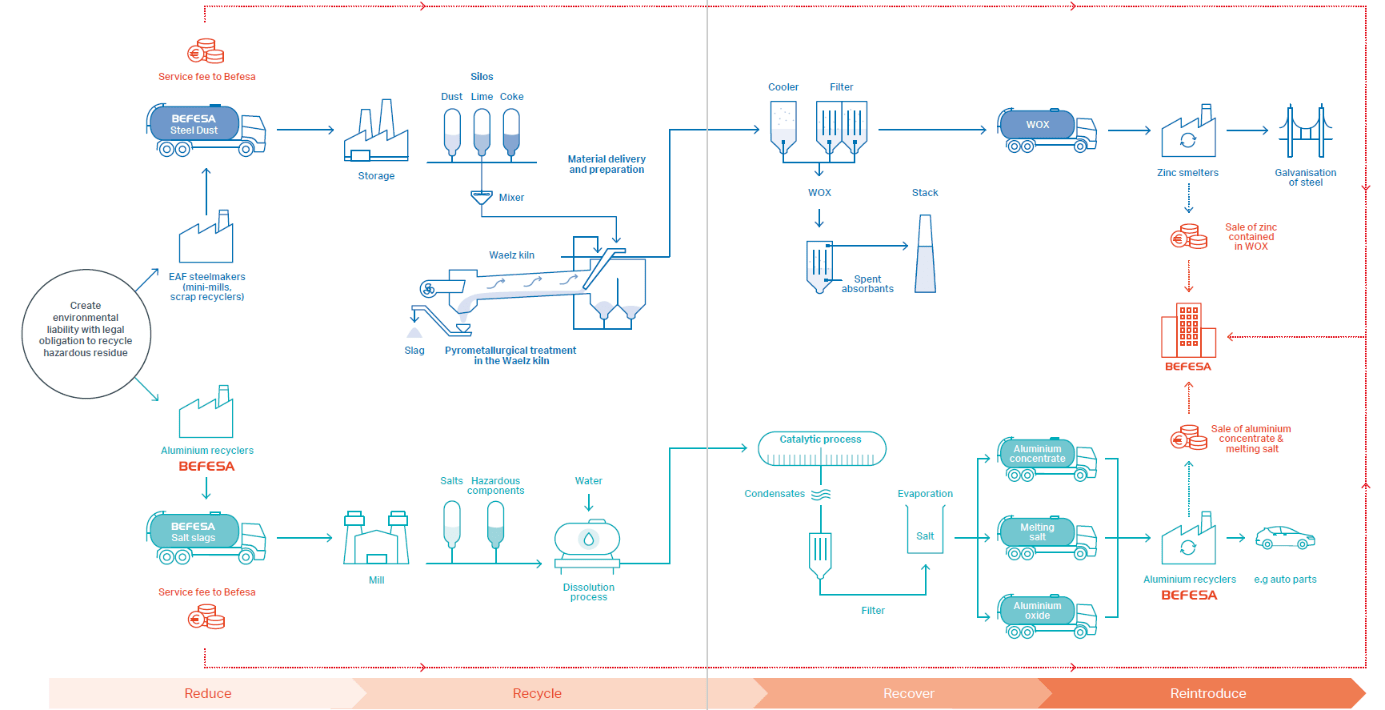

Befesa (OTCPK:BFSAF) is one of the most important companies offering recycling services to the aluminum and steel industries in the USA and certain European countries as it is active in Spain, France, Germany and Sweden. It also has exposure to China, South Korea and Turkey and its total annual capacity is approximately 2.5 million tonnes of EAF steel dust, salt slags and secondary aluminum. It operates 23 recycling plants where the hazardous dust and waste is processed. The company receives a fee for its recycling services and is able to recover and sell zinc as a by-product credit.

Befesa Investor Relations

During 2021, the company processed only about 1.6 million tonnes of residue yet its utilization rate was about 83% as the US-based capacity was only added during 2021 (and contributed for just 4.5 months to the financial result) and it took some time to ramp up operations and utilisation rates should increase. Unfortunately, it looks like 2022 may be a bit of a ‘lost year’ as especially in China the zero covid policy had an impact on the activities. On top of that, in Europe, the higher energy prices obviously also had a noticeable impact.

Yahoo Finance

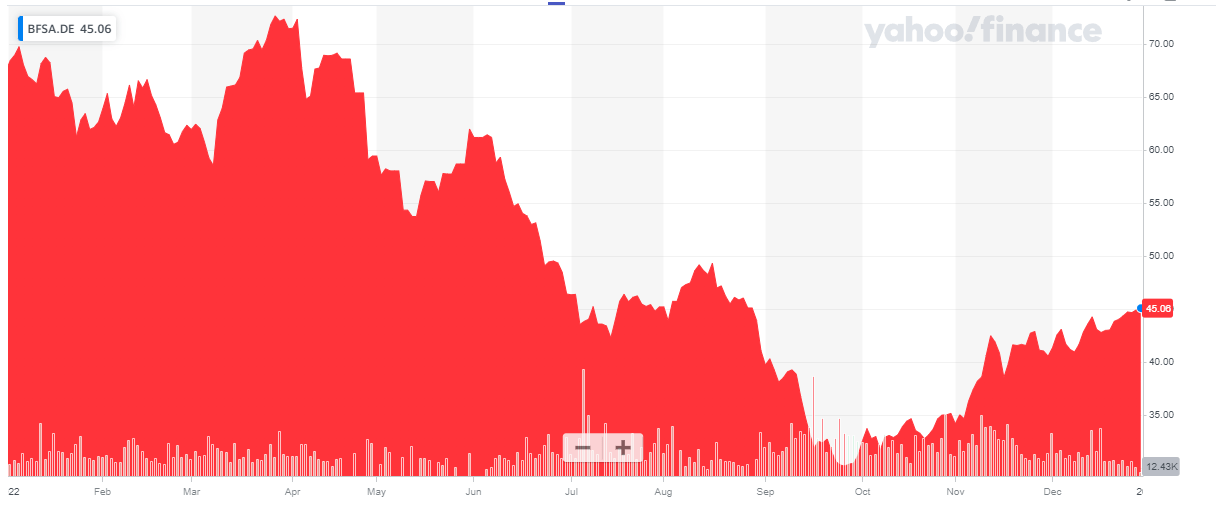

Although Befesa has its main listing in Germany on the Deutsche Boerse, keep in mind the company is actually Luxembourg-based and as such, dividends are subject to the standard 15% Luxembourg dividend withholding tax. There are 40M shares outstanding, resulting in a current market capitalization of approximately 1.8B EUR. The company’s most liquid listing is in Germany where it is trading with BFSA as its ticker symbol. The average daily volume exceeds 80,000 shares, resulting in a total monetary value of approximately 3.5M EUR per day. I will use the EUR as base currency throughout this article.

The 9M 2022 results were interesting, and provide a clear path for further growth

As mentioned in the introduction, I had high hopes for volumes and utilisation rates to pick up in 2022 but this may be a transitional year. Nonetheless, the EBITDA and operating cash flow will remain strong and this should enable Befesa to complete its expansion plans.

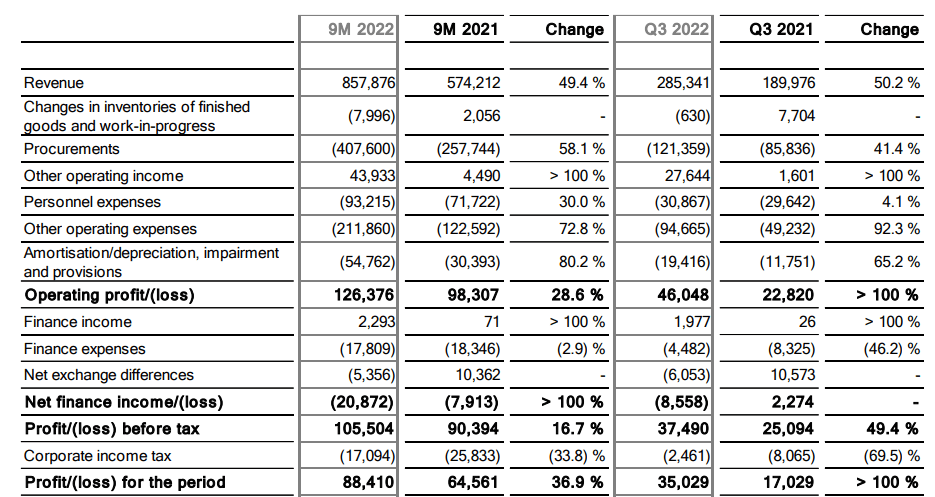

The total revenue in the first nine months of the year was approximately 858M EUR, a 49% increase compared to 9M 2021. But despite the strong revenue increase, the EBITDA increased by just 19.8 to 164M EUR. While that still is a nice increase compared to the first nine months of last year with a 137M EUR EBITDA, the FY EBITDA result is coming in slightly below expectations and this forced Befesa to update its EBITDA guidance to ‘more than 220M EUR’.

Befesa Investor Relations

The company remains very profitable as its bottom line shows a net income of 88.4M EUR for an EPS of approximately 2.2 EUR per share. That’s fine, especially when we look at 2022 as a transitional year.

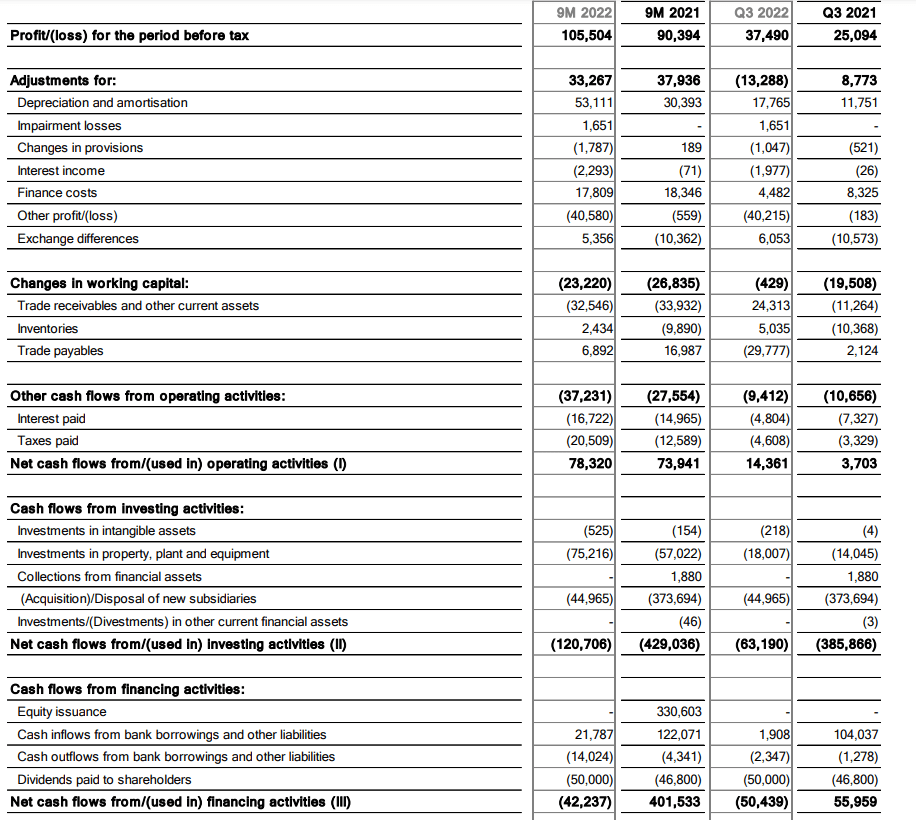

The cash flows were also very strong. The company reported an operating cash flow of 78.3M EUR but this included a 23.2M EUR investment in the working capital and includes a 20.5M EUR tax payment, although only 17.1M EUR would be due based on the 9M 2022 income statement. There should also be a 7M EUR lease payment included in the financing liabilities, so on an adjusted basis, the operating cash flow was approximately 98M EUR.

Befesa Investor Relations

The total capex was 75.2M EUR, but this includes growth capex. The total maintenance capex was just over 50M EUR in 9M 2022 as Befesa was catching up on some maintenance, and the annual sustaining capex should actually be less than 40M EUR. So if I would use the normalized sustaining capex and pro-rata it for three quarters, Befesa’s sustaining free cash flow would be around 56M EUR in the first nine months of the year.

That’s lower than the reported net income, and the difference is easy to explain: the income statement included a 44M EUR ‘other operating income’ and 40.6M EUR of that amount was deducted again in the cash flow statement and was related to the lower than anticipated acquisition cost of the a zinc refining asset.

In any case, we should expect the annualized operating cash flow to be approximately 130M EUR, likely increasing to 150-160M EUR in 2023. The cash flow will be useful to fund the company’s ambitious 5-year growth plan as it wants to invest 400-450M EUR in new capacity and assets.

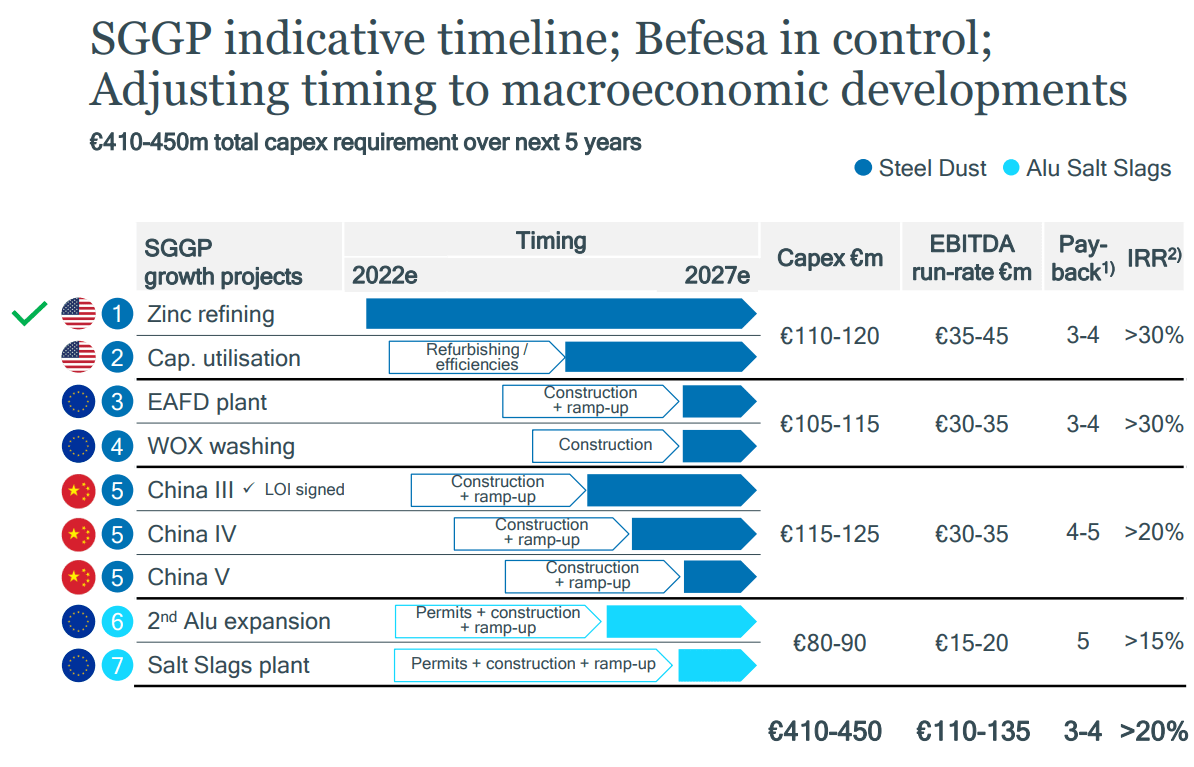

The next image, from the capital markets day presentation was very important for me.

Befesa Investor Relations

With a total investment of just 410-450M EUR, Befesa expects it will be able to boost its EBITDA by 110-135M EUR per year, resulting in IRRs exceeding 20%.

The very first element has now been completed with the acquisition of the zinc refining asset in the USA. This means the cumulative 2023-2027 growth capex will likely be just 60-70M EUR per year. This, in combination with the sustaining capex and the planned dividends should be fully covered by the incoming operating cash flows.

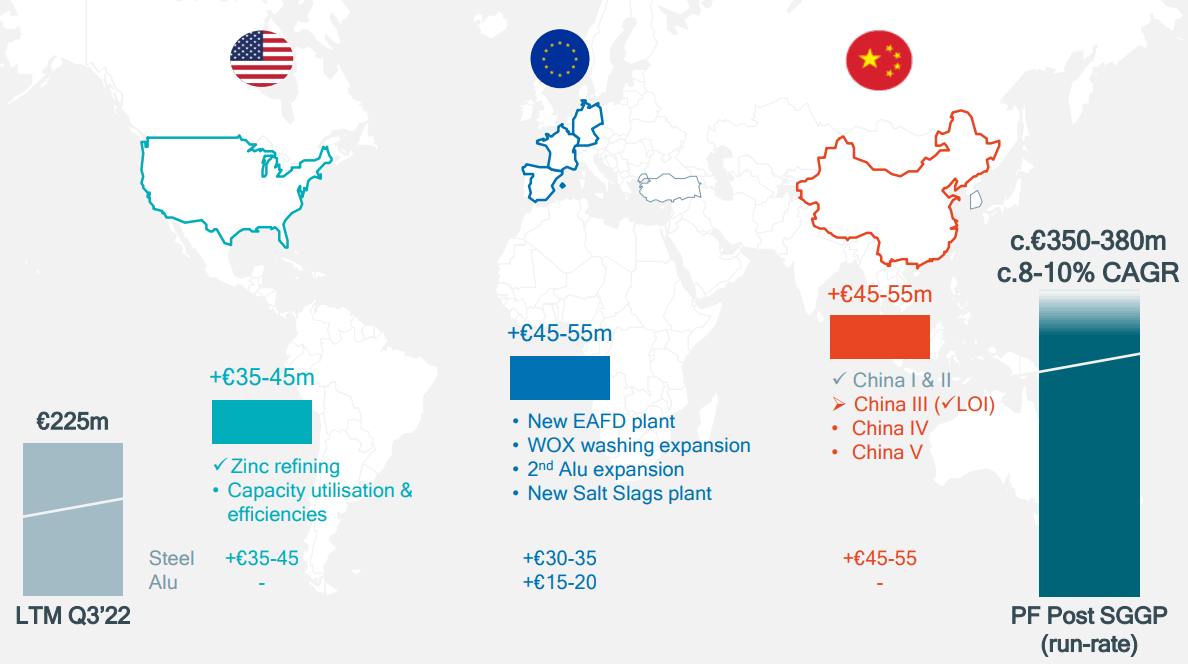

Befesa Investor Relations

And as you can see above, this should result in an EBITDA run rate of 350-380M EUR. After deducting interest expenses (20M EUR, as I anticipate the gross debt to decrease, despite the growth capex), 80M EUR in depreciation and applying a 25% tax rate, the net income run rate by the end of 2027 should be 200M EUR or 5 EUR per share. And assuming the sustaining capex will continue to track at about 70% of the depreciation expenses, the free cash flow per share will be 5.5-5.75 EUR per share. And this should all be achieved without requiring a single Euro of external funding.

Where will the growth come from?

I think the future for recycling looks great, and I think I should cut Befesa some slack as 2022 wasn’t the easiest year to work in. I expect more from 2023 as the end of China’s tough zero covid policy and the easing of the European energy prices should boost Befesa’s performance. With EBITDA tracking at the lower end of the 2022 guidance and the company likely missing its expectations to push the debt ratio below two times the EBITDA, all eyes should be on 2023 and beyond.

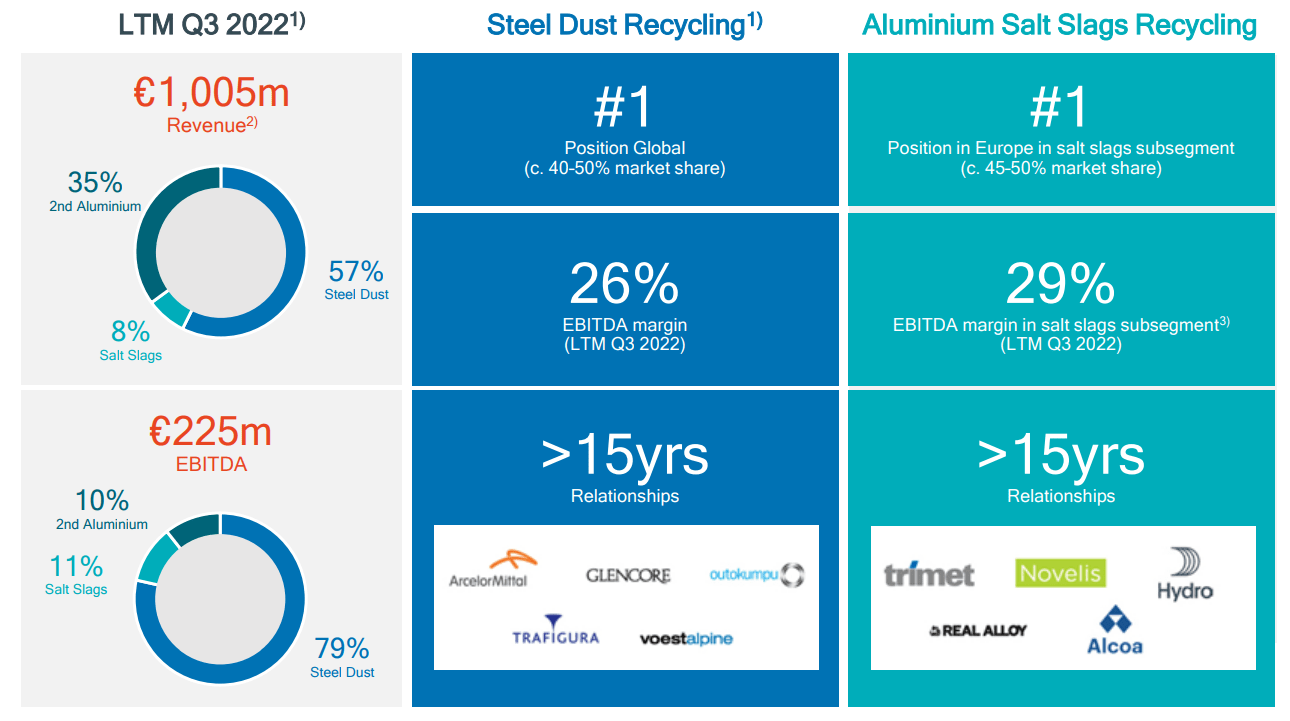

Befesa is the number 1 for steel dust recycling in the world and it’s easy to understand the large steel producers will want to continue to work with a reputable counterparty.

Befesa Investor Relations

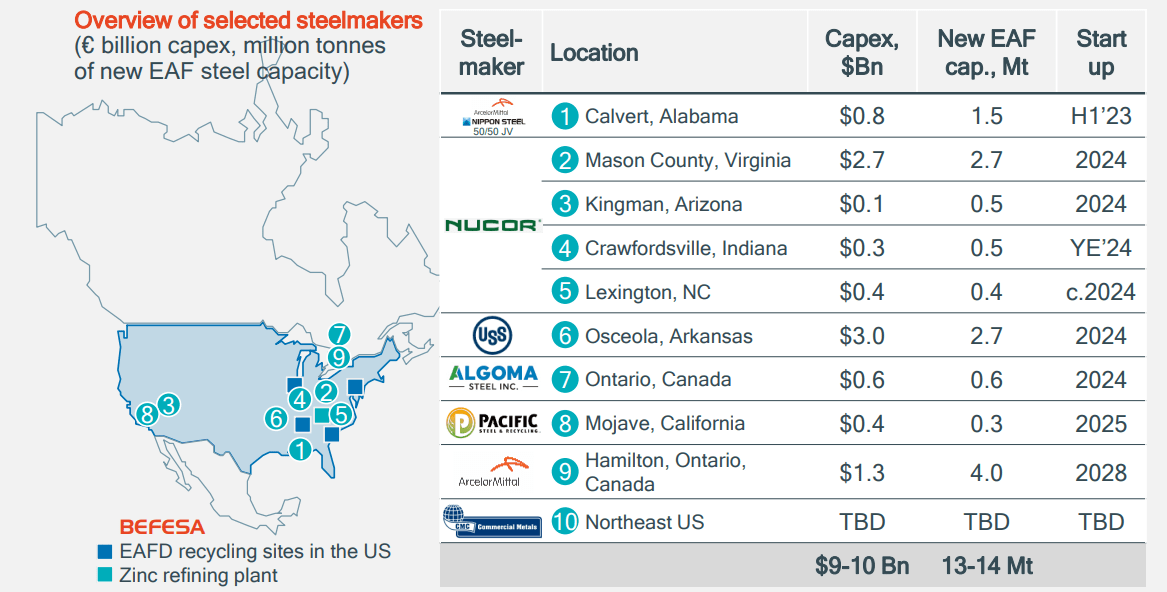

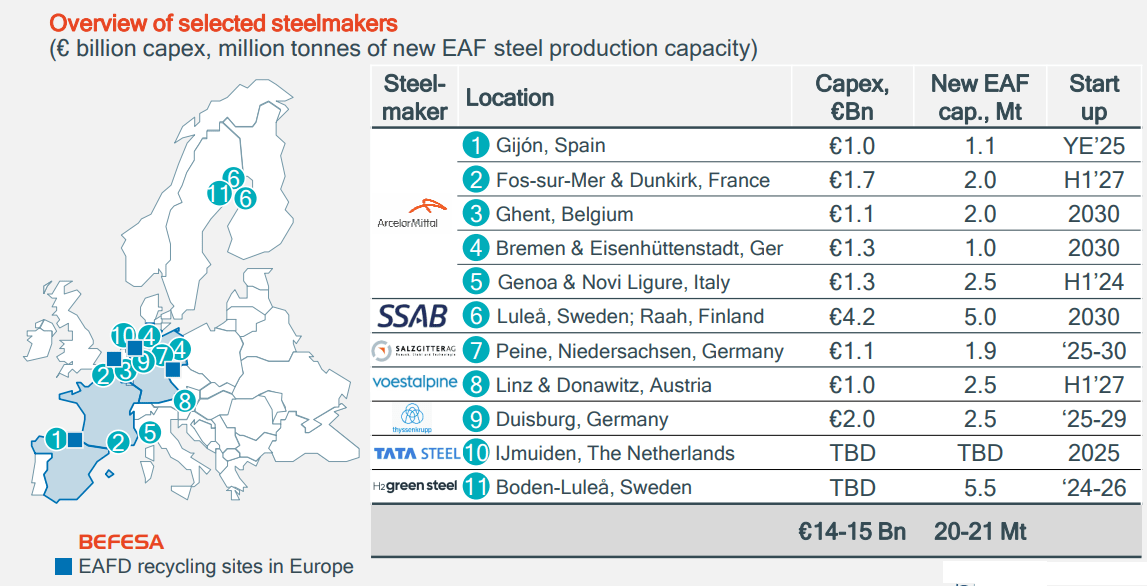

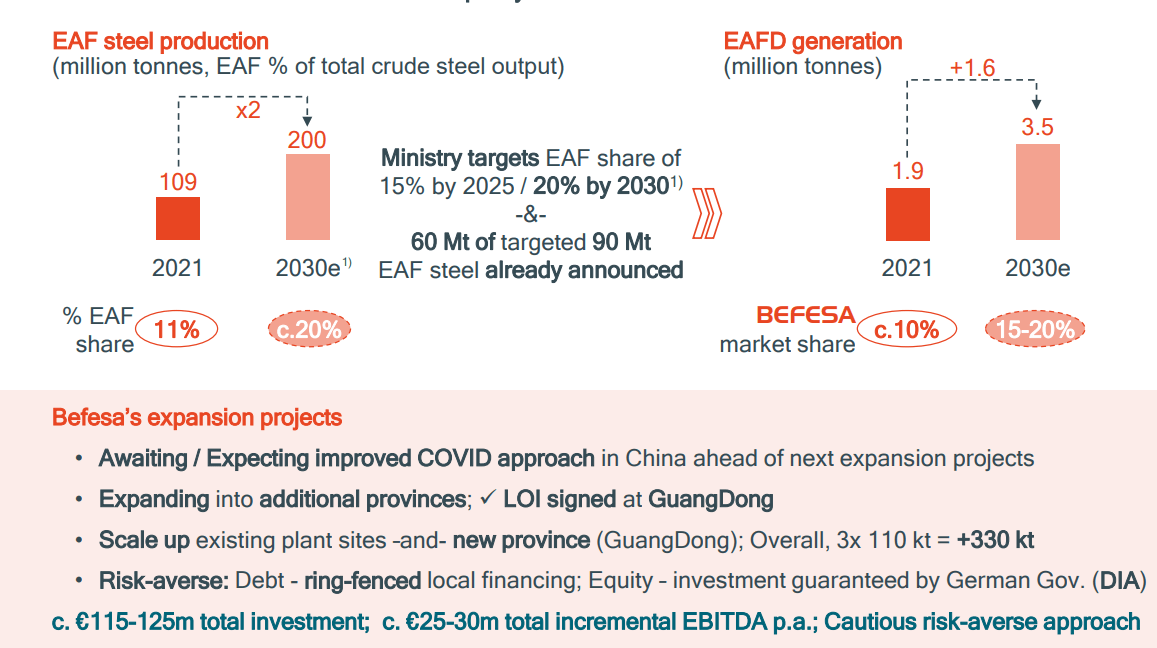

Befesa should grow in line with the acceleration of the conversion to Electric Arc Furnaces in the world, a cleaner way to produce steel. Between now and 2030, a total of 13-14 million tonnes of steel production will be converted to EAF, requiring the need for an additional 300,000 tonnes per year of dust handling capacity.

Befesa Investor Relations

We see a similar conversion plan in Europe, driving the need for an additional 350,000 tonnes in dust handling capacity by the end of this decade.

Befesa Investor Relations

So with its current expansion plan, Befesa is simply planning to retain market share and isn’t even budgeting gaining additional market share.

The real unknown is China where about 60 million tonnes of steel production is expected to be converted to Electric Arc Furnaces. This should create the demand for an additional 1 million tonnes of dust handling capacity. Befesa plans to grow its market share from 10% to 15-20% in China and its current expansion plans will provide 330,000 tonnes of additional handling capacity.

Befesa Investor Relations

Investment thesis

While the EBITDA will likely come in at just over 220M EUR this year, I expect a double-digit EBITDA increase in 2023 as China is reopening and Befesa will commission additional capacity.

I also like the company’s 5-year growth plan which should increase the EBITDA by in excess of 50%. All these expansions can easily be self-funded with the incoming operating cash flow the next few years. I think the company’s expansion plans are credible, realistic and achievable. Applying a multiple of 10 times EBITDA (which I think is fair given Befesa’s leadership in the space and the fact that I can only see the demand for recycling going up), the lower end of the 2027 run rate EBITDA guidance would result in an enterprise value of 3.5B EUR and an equity value of approximately 3B EUR (assuming 500M EUR in net debt by the end of that year). That represents a share price of 75 EUR. Reaching that target price would represent an annual return of 13.6% over four years (assuming the market will price the company based on its expectations for FY 2027 at the start of 2027).

The combination of all elements means I’m planning to have a very close look at Befesa as the company’s EBITDA should gradually increase from here on.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment