Spencer Platt/Getty Images News

Tapestry, Inc. (NYSE:TPR) provides luxury accessories and branded lifestyle products in the United States, Japan, Greater China, and internationally. The company has three operating segments, namely: Coach, Kate Spade, and Stuart Weitzman.

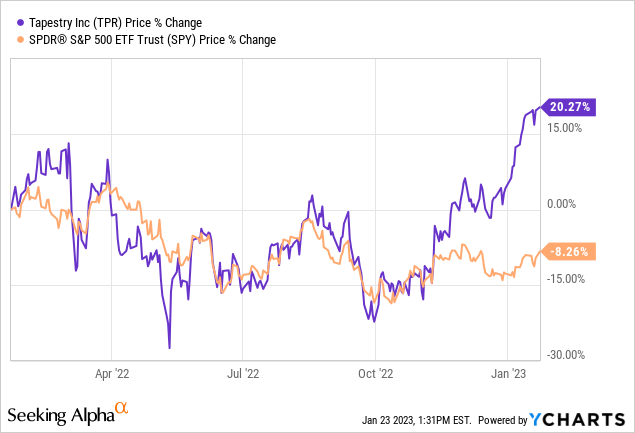

In the past 12 months, the firm has significantly outperformed the broader market, gaining as much as 20%, compared to the 8% decline of the SPY.

In this article, we are going to take a look at several macroeconomic factors, including consumer confidence and the reopening of China, along with some company specific numbers and ratios, which could signal how the company might perform in the coming quarters.

Consumer confidence

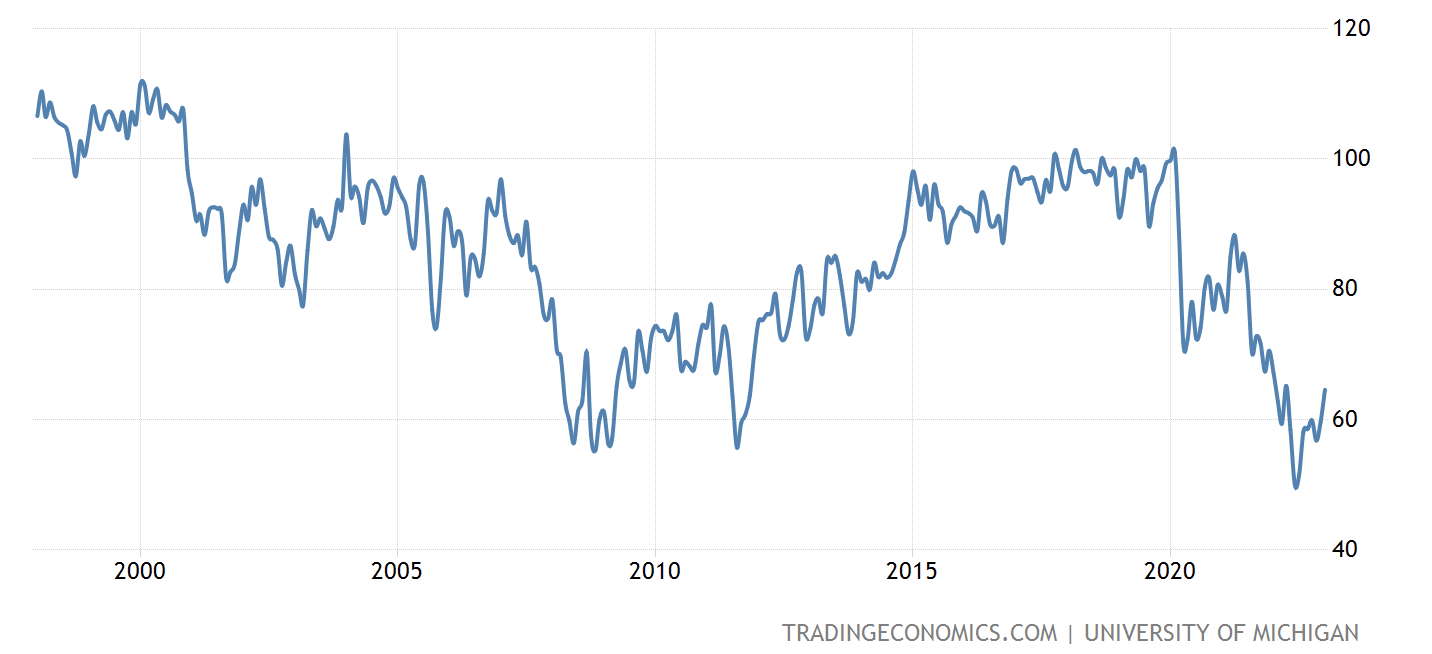

Consumer confidence is often treated as a leading economic indicator, which could signal potential changes in the spending behaviour of the people. Low consumer confidence readings indicate that the consumers’ view and outlook on the economy as a whole is negative. In such an environment, people are likely to save more and spend primarily on essential goods. In 2022, consumer confidence has fallen to historically low levels. In the recent quarters, however, it has sharply rebounded.

U.S. Consumer confidence (Tradingeconnomics.com)

In our view, the rebound is a good signal that the macroeconomic environment is becoming somewhat less uncertain, despite the readings remaining at historically low levels. We do expect the improvement in consumer sentiment to continue in 2022, although the rate of improvement is likely to slow substantially. We believe this could benefit the demand for TPR’s products in the near term.

Analysts at Bernstein are however not entirely convinced that Tapestry could benefit from the improving consumer confidence. They have recently downgraded the stock for the following reason:

For premium brands and retailers, the party is over,” the downgrade note explained. “The demand for affordable luxury and premium brands is likely to soften in 2023, comping against last year’s wave of spending.

Reopening of China

The reopening of China is also likely to positively benefit TPR’s business in the near term. While the North American region is where the largest portion of TPR’s revenue is generated, the Greater China area is also a significant contributor.

Net sales by region (‘TPR’)

As the Chinese government has recently announced the lifting and easing of Covid related restrictions, we believe that these sales figures from the Greater China area are likely to improve substantially in the near term. We expect the lifting of restrictions to lead to a substantial increase in demand for TPR’s products.

Goldman Sachs has also recently published a list of stocks, which could benefit the most from the reopening of China. Tapestry is also on this list.

While both the improving consumer confidence and the reopening of China could positively impact the company’s financial performance and potentially its stock price, there are other factors that we need to consider before making an investment decision.

Inventory

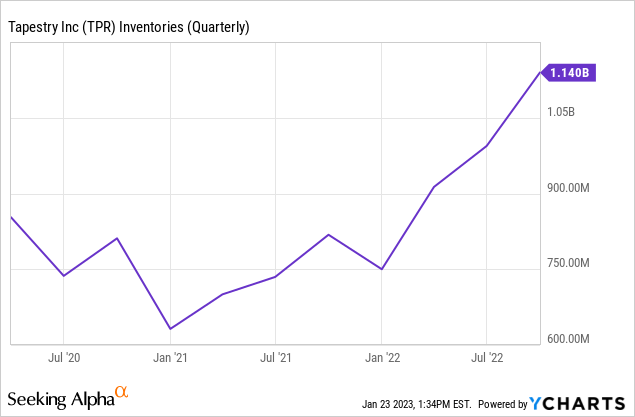

In the recent quarters, the firm’s inventory has been growing rapidly. Many retailers in 2022 have been struggling with inventory management issues. Many had to use steep discounting in order to get rid of their excess or obsolete inventory.

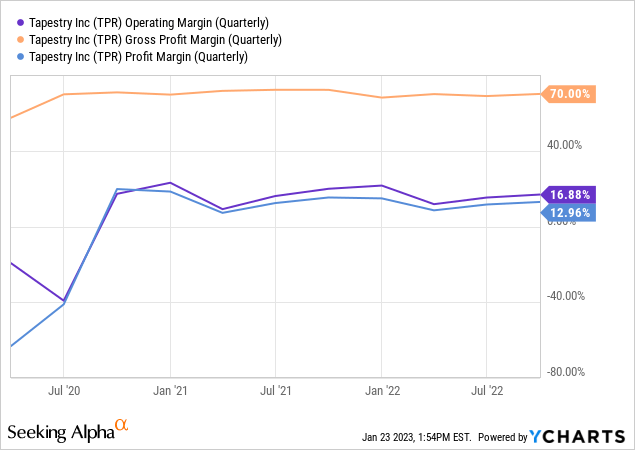

While so far the firm has managed to keep its margins relatively constant despite the challenging macroeconomic environment, we believe that the potential for discounting is relatively high.

We believe that margin contraction in the coming quarters could be a real risk. We would like to see, how TPR will be able to manage its inventory and what impact it would have on the margins, before we would feel confident investing in the company’s stock.

At Barclay’s the firm has been also downgraded and the worsening sales to inventory ratio has been pointed out as one of the reasons:

A worsening sales-to-inventory growth spread for TPR and an edited assortment with product that the firm believes benefited from “return to work/occasion/travel” in the spring season last year is also seen working against earnings results.

At the same time, BofA analyst Lorraine Hutchinson and team are somewhat more optimistic, writing:

[…] more effective discounting and product innovation for Tapestry (TPR), while finding little markdown risk to inventory given that the apparel company has mainly core products and styles that transcend seasons.

Also, important to highlight that Nordstrom (JWN) has recently announced that it is cutting its profit outlook after a highly promotional season. We believe that this could already be an indication of how other retailers may have been performing during the latest quarter.

The holiday season was highly promotional, and sales were softer than pre-pandemic levels. While we continue to see greater resilience in our higher income cohorts, it is clear that consumers are being more selective with their spending given the broader macro environment, […]

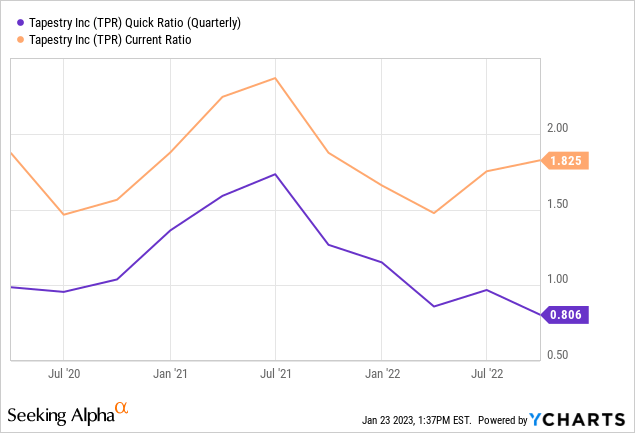

Liquidity

Two ratios, which are often used to analyse a company from a liquidity point of view, are: current ratio and quick ratio. If the current ratio is above 1, it means that the firm has enough current assets to cover the current liabilities. In the case of the quick ratio, inventory is excluded from the current assets.

While the current ratio has stayed far above 1 during the past years, the quick ratio has seen a gradual decline, starting from mid 2021. The latest reading was somewhat above 0.8. While this reading may not be critical at the moment, we would like to see this ratio to improve. Having a quick ratio below 1 could mean that the firm may not have enough financial flexibility in the near term, if the macroeconomic environment does not improve in a way that we would expect.

Key takeaways

The improving consumer confidence may be a good sign for retailers, as it may signal a growth in demand in the near term. On the other hand, analyst at Bernstein are not so convinced about this potential improvement.

The reopening of China is likely to benefit TPR’s financial performance. The firm has also been listed by Goldman as one of the companies, which may benefit the most from the reopening.

The rising inventory levels are raising concerns. We believe it may have a negative impact on the margins, if promotional activity will be necessary to get rid of excess or obsolete inventory.

While the liquidity position does not seem particularly concerning now, we would like to see the quick ratio improving, before we would recommend investing.

We currently rate TPR’s stock as “hold”.

Be the first to comment