rlesyk/iStock Editorial via Getty Images

Don’t worry! This isn’t yet another article attempting to use technical analysis to find a fair value for the Barrick Gold Corporation (NYSE:GOLD) stock price.

In our analysis of Barrick Gold, we discovered a few critical operational headwinds, which could see the stock trail its peers in the coming quarters. Observations suggest that input costs might taper; yet, an overblown gold price argument coupled with questionable project ramp-ups and worrisome opportunity costs might cause Barrick Gold’s stock to capitulate.

We understand that this article will yield divided opinions. However, it contains a few critical talking points.

Without further ado, let’s move into a detailed discussion about Barrick Gold.

Operational Review

Critical Assets Constrained and Underperforming

Barrick provided an update on its reserves on Thursday, stating that there is a “probable increase” in proven reserves to 76 million ounces (up 8 million ounces from January 2021), led by its Pueblo Viejo mine. Please note the word “probable.”

Furthermore, Barrick Gold’s preliminary Q4 report was unsurprising as results revealed gold production has now slipped for three straight years. Barrick is struggling with various issues, such as government constraints, delayed ramp-ups at critical assets, and questionable capital allocation.

Gold Operations

Let’s start with our outlook on the positives and traverse down to the negatives later.

A quarter-over-quarter vantage point suggests that Barrick achieved stronger results from its Carlin mine as planned maintenance cooled down. The more robust results were due to higher grades and enhanced throughput, leading to a 10% quarter-over-quarter production increase. However, note that year-over-year production fell. Nothing is stopping Carlin from producing above the midpoint in 2023; however, the mine’s all-in sustaining costs are typically high, as shown by its 16% year-over-year increase. Nevertheless, this could be offset by lower cost of goods sold, as input costs are seemingly slowing with global inflation moderating.

Furthermore, Cortez might rebound in 2023. The asset experienced a 25% yearly slump in production due to mine sequencing. Higher throughput can unfold this year due to sequencing and higher implied gold prices. Again, lower COGS is a possibility as fuel and labor costs are stagnating.

As for Pueblo Viejo, gold produced slumped by 5% year-over-year while all-in-sustaining costs surged by an astonishing 46% during the same period. Barrick is working on environmental approval for a tailings facility at Pueblo Viejo; additionally, it’s in the midst of an expansion. However, results remain underwhelming, and we do not see a massive rebound in 2023 here, as its all talk and no results at the moment.

A significant concern is Barrick’s Porgera joint venture in Papua New Guinea, which was initially placed on maintenance in 2020. However, the project’s restart is subject to government approval of the ownership structure, which has not yet experienced tangible developments. We see this as sunk capital, opportunity costs, and a bad situation overall.

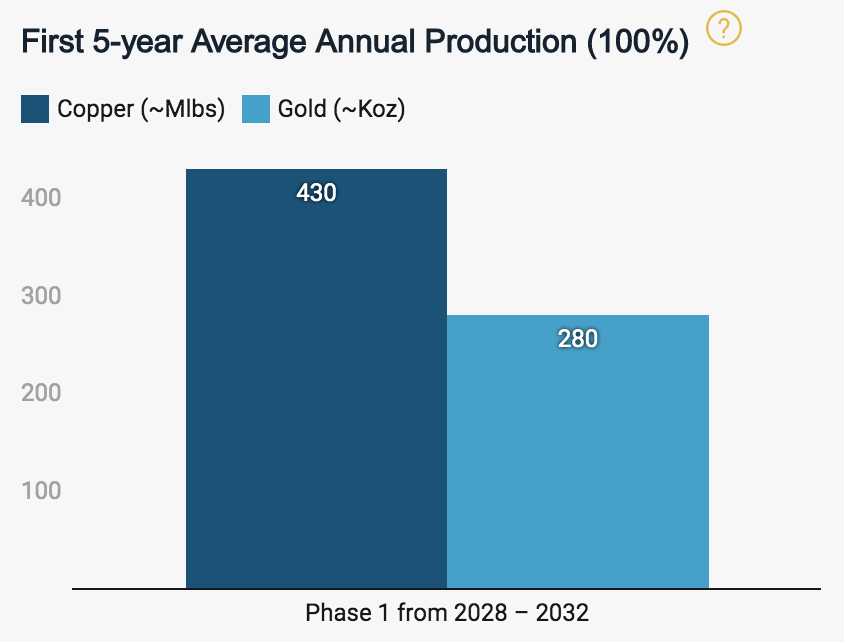

Lastly, Barrick recently committed to the Reko-Diq Copper-Gold project in Pakistan. The mine’s updated geophysical report suggests production will commence in 2028. We don’t believe that investors will yet value minerals in the ground here, and it will probably be seen as investing cash outflows for the time being. Moreover, political instability in Pakistan is at a multi-decade high, and the asset is 50% owned by state-owned enterprises and direct government entities. Thus, we deem the risk-reward of this project unfavorable.

Reko-Diq (Barrick Gold)

Copper Outlook

Let’s briefly look at copper operations.

Barrick’s Lumwana mine has recovered by 44% quarter-over-quarter after grid issues. Lumwana could add significant value in the coming years.

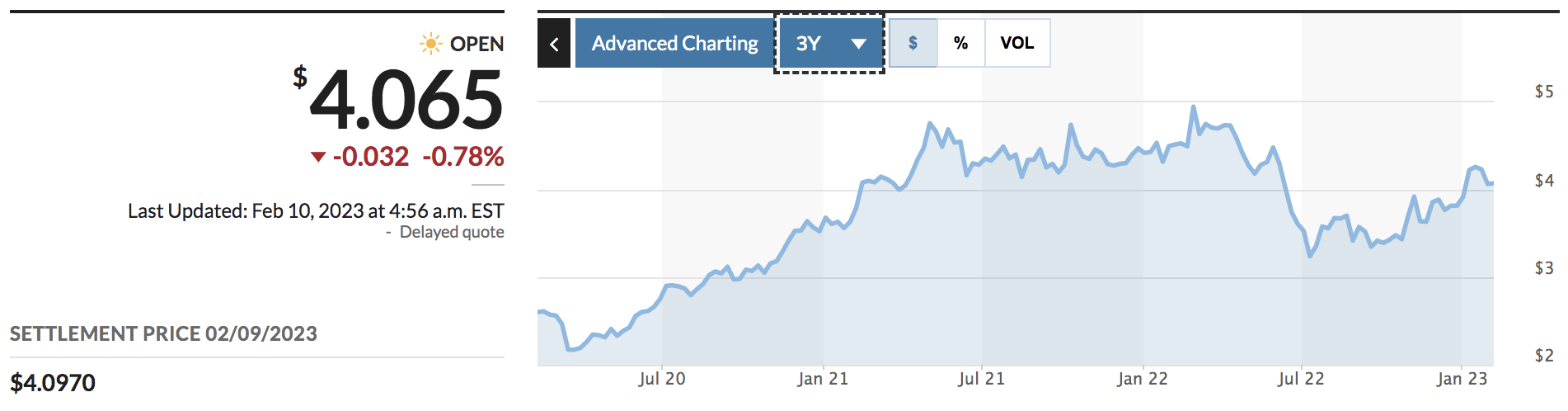

Broadly based, the company’s copper production surged by 23% year-over-year. However, all-in-sustaining costs also rose by a staggering 20%. A situation could unfold where all-in-sustaining costs taper during 2023 due to the aforementioned reasons. And sustained prices might elevate profits.

Copper Spot (Market Watch)

Although Barrick’s copper operations are accumulating and cointegrated with many of its gold endeavors, it makes up less than 10% of its revenue mix. As such, any changes to sales and production will have minimal effect on the company’s broad-based results.

Counterargument

Share Buybacks

Barrick Gold’s share buyback program juxtaposes an uncertain operating outlook. It reiterates that there is often a difference between the variables that affect a stock’s price and its underlying entity.

Barrick Gold is in the midst of a $1 billion buyback program. Executing share buybacks while operations are struggling is a red flag as it often signals that management wants to raise the share price to make it more investable to institutions. We aren’t saying this is the case for Barrick; however, the possibility can’t be ignored.

In conclusion, we could see a decoupling between Barrick’s operating performance and its share price due to its buyback program, which could transpire into stock price momentum.

Outward Support

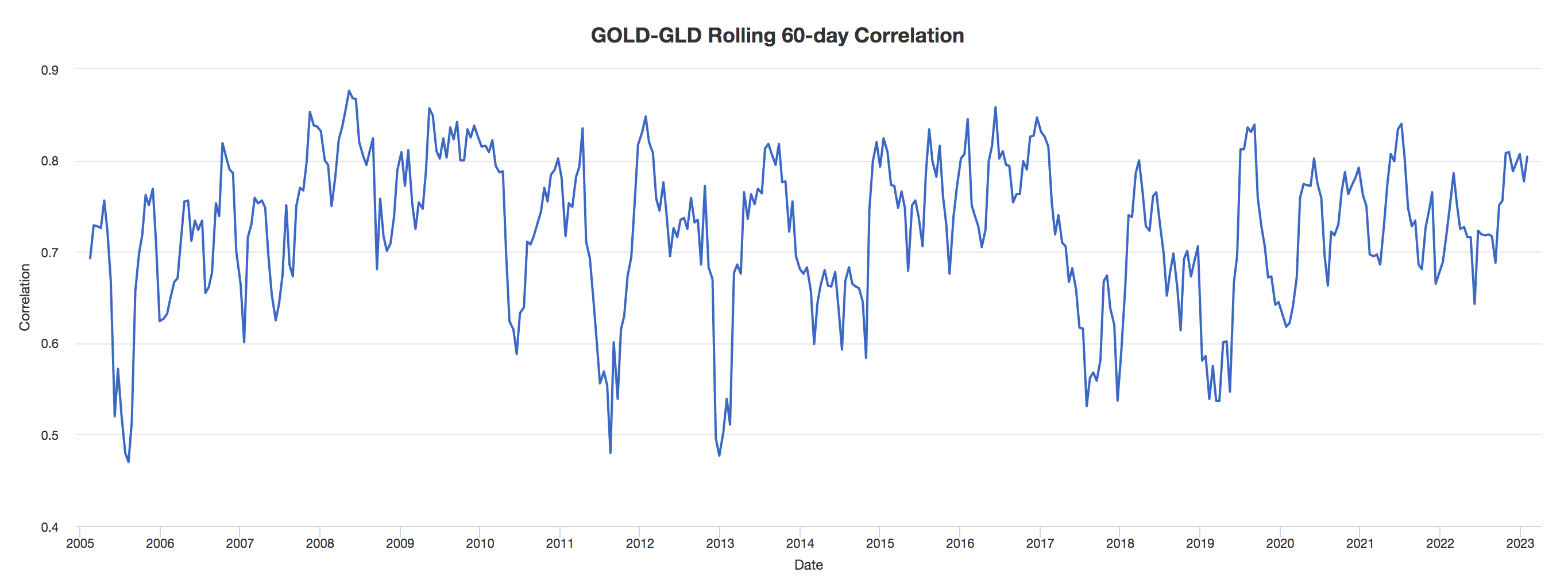

Another counterargument against our bearish thesis is that investors might simply buy Barrick’s stock based on systemic support from gold prices. As argued in one of our previous articles, we aren’t overly convinced about the fundamentals behind 2023’s gold rush. However, it must be considered that perception often dominates reality in the financial markets.

Below is an illustration of the correlation between gold prices and Barrick Gold’s stock price.

Author in Portfolio Visualizer

Dividends, Valuation, and VaR

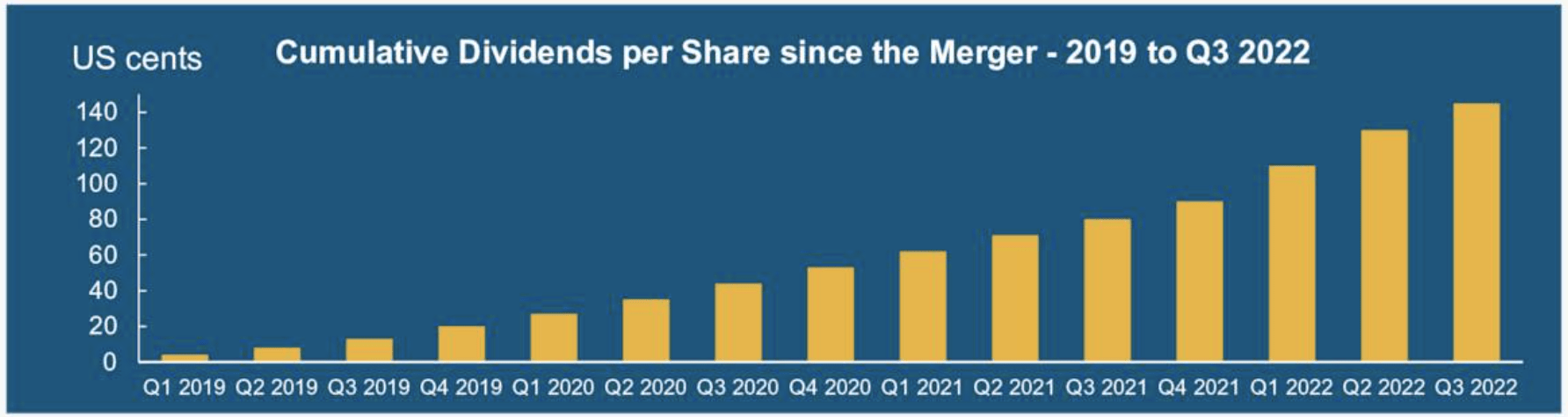

Similar to its share repurchases, Barrick rewards its shareholders with generous dividends. It has a five-year yield on cost of 3.06% and exhibits four consecutive years of dividend growth, which will probably encourage demand for the stock from income-seeking investors.

VBN (Barrick Gold)

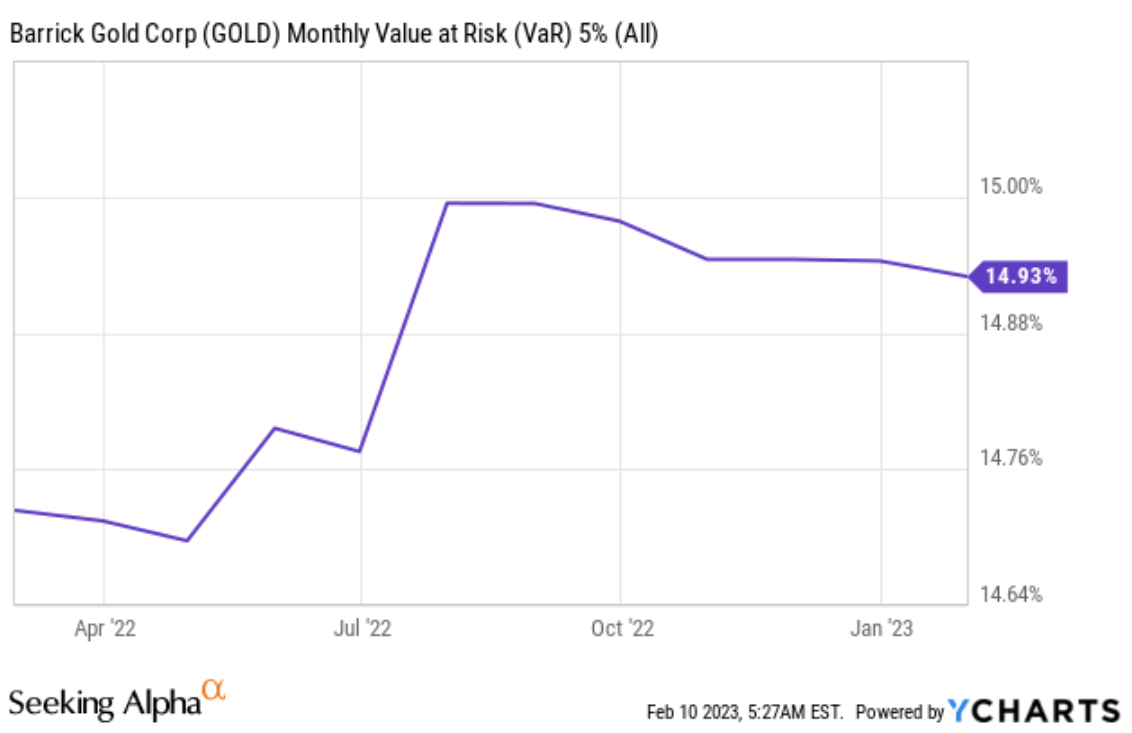

Despite its incredible dividend characteristics, Barrick possesses an unfavorable value-at-risk value. Based on the stock’s current volatility, it will probably lose at least 14.93% of its market value in 5% of its traded months. Moreover, Barrick’s stock is trading at a price-to-book ratio of 1.32x, suggesting that the market has already priced its equity value.

Monthly Value at Risk 5% (Seeking Alpha)

Although Barrick Gold provides a solid dividend, its stock hosts excess price risk, which is why we are not overly keen on the security’s total return prospects.

Final Word

In conclusion, Barrick Gold Corporation’s operations are underwhelming, which could see it lag its peers. Although critical progress has been realized, it is unlikely that noticeable ramp-ups will occur in 2023.

The company’s share buyback program and dividend policy might entice investors to buy the stock. Nevertheless, Barrick Gold Corporation’s questionable fundamentals and an overhyped gold price argument might lead to disappointment. Therefore, we assign a sell rating to Barrick Gold Barrick Gold Corporation’s stock.

Be the first to comment