jetcityimage

Bank of America Corporation (NYSE:BAC) has changed its business model since the great financial crisis of 2008. Once at the epicenter of the highly destructive subprime loans, it has now focused at the other end of the spectrum in conservatism. Today, we will go over how the bank has performed over the longer run, and take a look at a couple of great income choices that might make sense for investors.

Fair Value Today

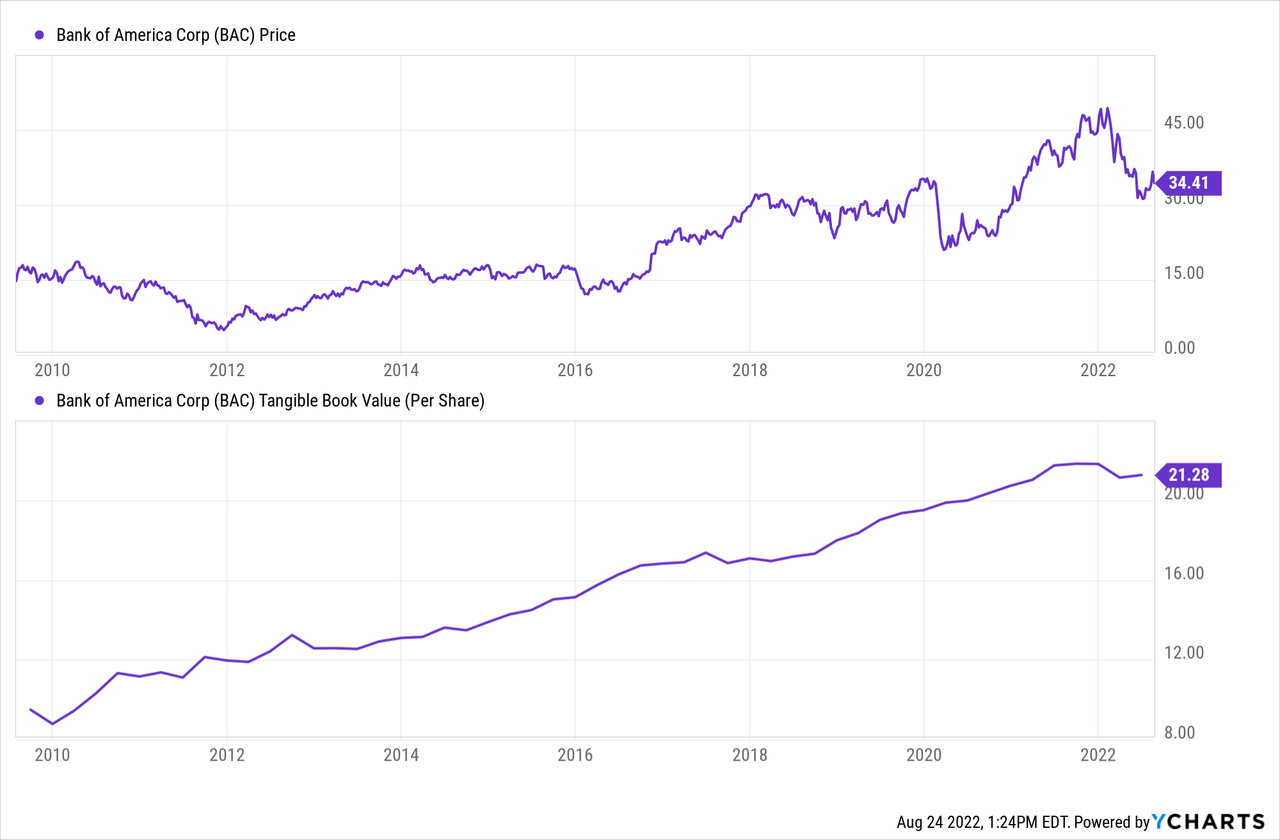

BAC has increased its tangible book value per share by over 120% since 2009. The performance has been steady with a few small drops along the way.

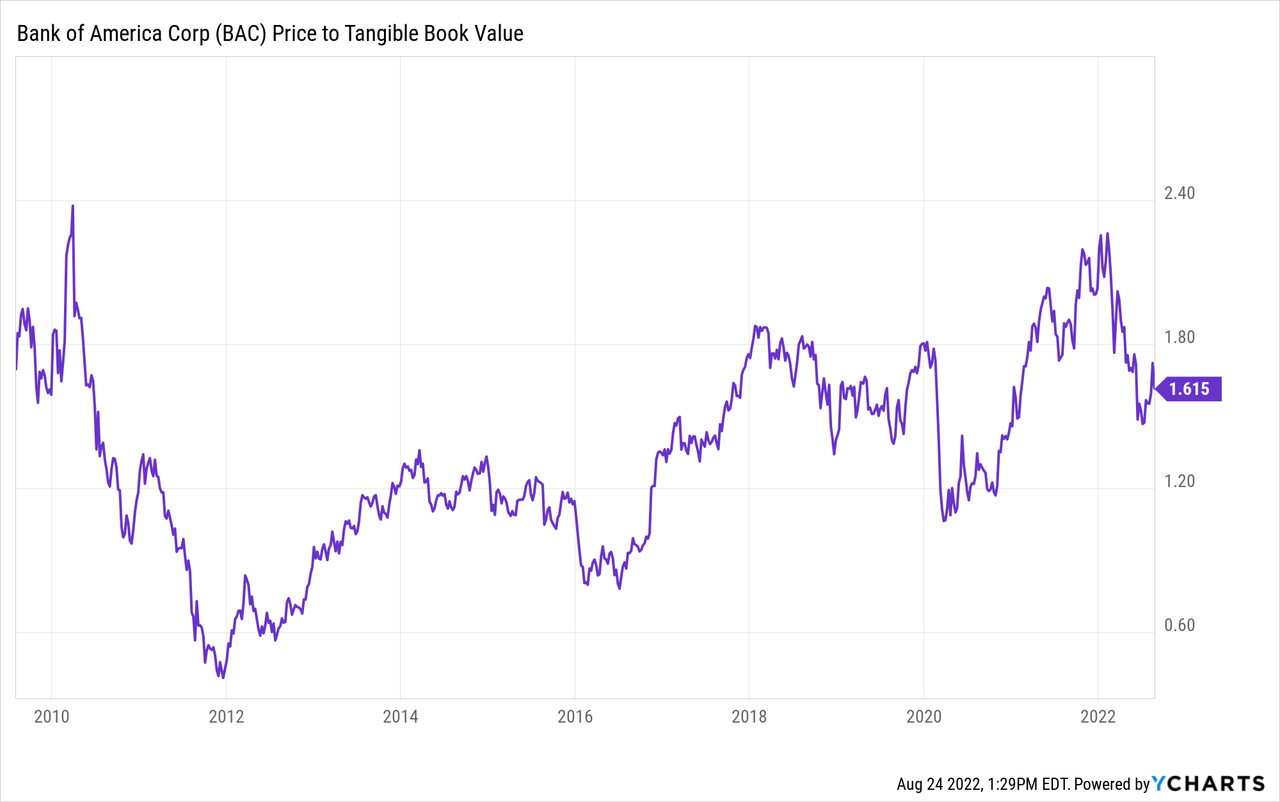

The stock though has had a far more volatile movement as investors went from extreme pessimism in 2012 (0.6X tangible book) to extreme optimism in 2022 (2.3X tangible book).

The recent drop from the highs was predictable as investors became enamored with peak earnings and bid the bank to crazy heights. Q2-2022 brought investors back to earth as earnings fell 9%.

Bank of America Q2-2022 Presentation

Don’t get us wrong, those results were fine, all things considered. We were particularly impressed by the control on non-interest expenses, a category we felt JPMorgan Chase & Co. (JPM) slipped on. Markets were probably focused on the falling income and the slowdown in capital return based on the new higher CET1 requirements. The extremely high valuation was only the fodder for the fat bears.

At present, we think the shares are in the “hold/neutral” range. Valuation has come down but we would see only a sub 1.4X tangible book as a compelling entry point. We are very confident we will get that in a recession with accelerating charge-offs and a very flat to inverted yield curve. So our take here is “buy below $30”.

Choices

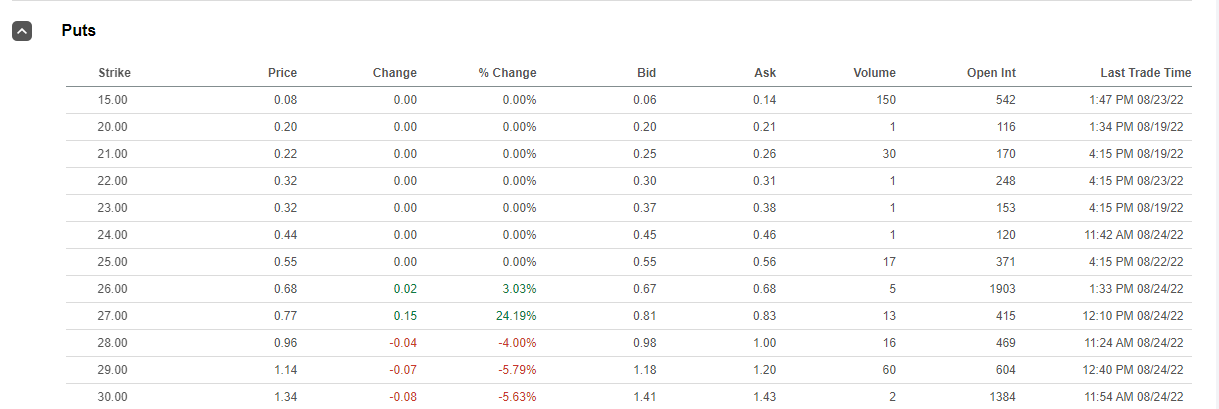

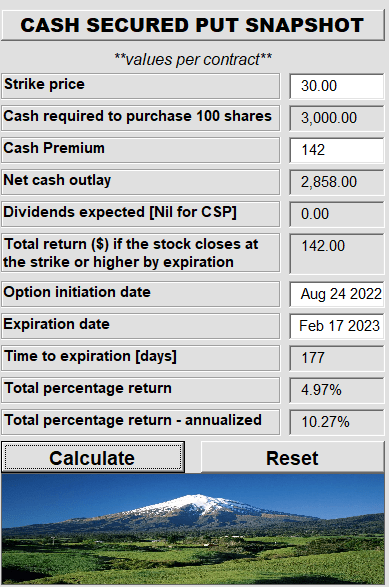

Investors could no doubt wait for that setup and that would be a great point to buy. Of course there is no certainty in anything (despite our stated confidence), and you could never get that sub $30 price. One way to approach that would be to sell Cash Secured Puts for $30.00. Below we have shown the February 2023 Put options.

Seeking Alpha

The $30 strikes have a great risk-reward setup with a 10.27% yield, even if prices drop about 15% till then.

Author’s App

That is, as long as BAC stays over $30 at expiration, you would make 10.27% on risked capital.

The Other Alternative

Of course, not all income investors are comfortable navigating the options landscape, even if provides the best risk-adjusted yields. For those that are not comfortable, we do have another idea. Hear us out.

BAC provides a very tiny 2.44% yield. The advantage of that rather minuscule payout is that BAC has an amazing dividend coverage and can buyback shares as conditions dictate with remaining cash. But for those looking for more yield, outside of options, Bank of America Corporation 7.25% Convertible Preferred L (NYSE:BAC.PL) a really busted preferred, provides an interesting alternative.

Bank of America

Preferred Stock :: Bank of America Corporation

A few relevant points on this preferred share class that we think investors should grasp are presented below.

BAC.PL was Issued in 2008 and the par value was $1,000. The shares rank in line with other preferred issues and like almost all of them, (there is one exception) the dividends are non-cumulative. BAC.PL and all other preferred shares need to be paid if BAC wants to pay a single cent to common shareholders.

It is one of the rare preferred shares out there that cannot be redeemed by BAC i.e. it is non-callable. BAC.PL is also convertible at the option of the holder into 20 shares of common stock. This was based on a $50 common stock price ($1,000 preferred share price) at the inception of this preferred series. At current market price, the preferred stock conversion does not make sense (preferred $1,221 versus $35 for common). The $35 common shares would only equate to $700 in total.

The original conditions also allowed BAC to force a conversion, on or after January 30, 2013. Here the requirements were that if the common shares exceeds $65 (130% of $50) for 20 trading days during any period of 30 consecutive trading days, the bank has the option to convert all or some of this issue into common shares.

The one reason we are bringing this one up now, is that the price is far more reasonable. Looking at the one year timeframe, we can see that there was a bohemian push on this all the way to $1,500 a share.

Seeking Alpha

Investors bidding that would get a 4.83% yield on their price. They would also risk a forced conversion down the line, where they would be paid back perhaps as less as $1,300 in BAC shares. Assuming the same happened within a 4 year time frame, those “investors” would make about 1.5% a year as their $290 in dividends would be offset with a $200 loss on conversion.

Today, however, things look quite peachy in comparison. BAC.PL now gets 5.99% on a stripped yield basis. BAC is nowhere near $65, but even assuming it gets there, a forced conversion would create a capital gain of about $80.00. In other words you have sailed right past the return-free-risk zone which yield chasers had gotten into.

There are other events like an acquisition, reorganization or fundamental change in the investment that can prompt a conversion to common (receiving make-whole shares), which can be read in further detail in the prospectus. Our assessment on those is that they are extremely unlikely, but investors may want to read through those by themselves.

Verdict

BAC wins full marks for their longer term performance and we believe even in the upcoming turbulent times, it will show its mettle. The common shares are poor yield plays though and hence we have outlined two interesting choices for those looking for income. We have our financial sector quota full for now, but we are keeping an eye on both these choices for our subscribers.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment