style-photography

In observing this year’s year-to-date market rally, a common question among investors is: is it too late to jump in, particularly in the tech sector where so many of last year’s biggest decliners have made major inroads back up? My answer is no, it’s not too late at all to participate in the rebound: it just requires careful stock-picking.

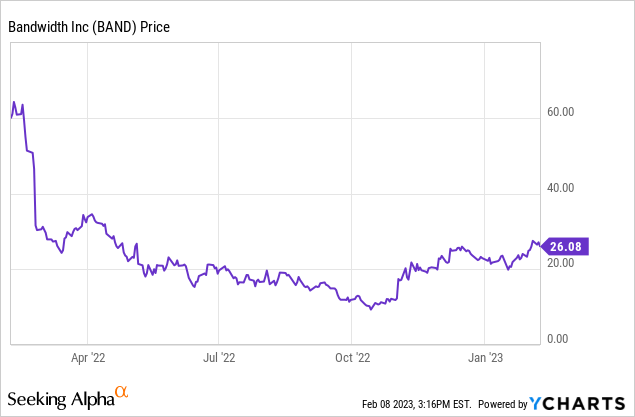

“Growth at a reasonable price” continues to be my favorite way to play the rebound, and Bandwidth (NASDAQ:BAND) is a shining example of this strategy. The communications-platform-as-a-service vendor (CPaaS), a direct rival to Twilio (TWLO), has seen its share price drop ~60% over the past year, though it has enjoyed a double-digit recovery so far this year. There’s plenty of upside left to go here.

The bull case for Bandwidth will be more apparent this year

Bandwidth will next report earnings in the tail end of February, but I think now is an excellent time to pick up BAND stock while A) expectations are still low, holding down Bandwidth’s valuation and B) indicators from the prior quarter, as well as potentially softening headwinds such as FX, should help Bandwidth break past conservative expectations heading into this earnings cycle. I remain bullish on Bandwidth and have held onto the stock, even as I’ve enjoyed a huge rebound recovery from its low points reached last Fall.

Here, in my view, is the long-term bull case for Bandwidth:

- Growth and profitability, not to mention value, in one neat package. Bandwidth is a haven for safety-oriented investors. It balances mid-teens revenue growth alongside a positive adjusted EBITDA margin (which continues to see expansion potential).

- The CPaaS space isn’t as competitive as other areas of enterprise software. You can name dozens of different CRM or HCM companies. This isn’t true of Bandwidth’s space. Bandwidth and Twilio are by far the most recognizable names in the space, followed by smaller startups like Nexmo. Bandwidth’s ability to corner this market is far better than an enterprise software company in a more tightly competitive arena.

- CPaaS naturally lends itself to expansion. Bandwidth’s dollar-based net expansion rates are healthy in the ~110% range. The fact that all of its pricing is usage-based means that as its customers (Internet companies) grow their own usage and website/app visitors, Bandwidth’s revenue will increase without the company having to lift a finger.

- Use cases are varied and growing. The diversity of Bandwidth’s client base is a testament to how broadly applicable its product is. For example, Google (GOOG) (GOOGL) is a Bandwidth client, using Bandwidth voice to give its Internet calling capabilities to businesses and consumers. Arlo (ARLO), the security camera company, uses Bandwidth’s 911 access company to connect its customers with local emergency departments. Zoom (ZM) has its conferencing platform powered by Bandwidth Voice.

- Opportunity for product category expansion. Twilio extended its growth potential by adding new products like call-center operations software. To date, Bandwidth has stuck to its core voice-and-text capabilities, so adding additional features opens up even more growth for Bandwidth down the road.

Valuation update

Of course, Bandwidth is an appealing stock for one main reason: value. At current share prices near $26, Bandwidth trades at a market cap of just $660.2 million. After we net off the $311.6 million of cash and $637.2 million in convertible debt on Bandwidth’s most recent balance sheet (as a footnote here, do recall that Bandwidth is also FCF-positive), the company’s resulting enterprise value is $985.8 million.

Meanwhile, for the upcoming fiscal year FY23, Wall Street expects Bandwidth to generate $613.3 million in revenue, representing 9% y/y growth (data from Yahoo Finance).

Now, there are a number of reasons why that estimate may be conservative. First, Bandwidth is currently growing revenue in the teens, and guidance for Q4 calls for a growth range of 16-17% y/y growth. Second, FX headwinds should taper down as the dollar has weakened significantly since the start of the year. Third, the company is lapping significant one-time headwinds in FY22, including lingering impacts from a 2021 DDoS attack as well as the defection of two large customers in Q2 of 2022. So to me, a single-digit growth rate in 2023 seems like a “worst case scenario”.

Nevertheless, even by taking guidance at face value, we only get to a valuation of 1.6x EV/FY23 revenue for Bandwidth – despite a rising gross margin profile, positive FCF, and a wide-open market opportunity with expansion potential.

Transitory headwinds should fade; customer growth

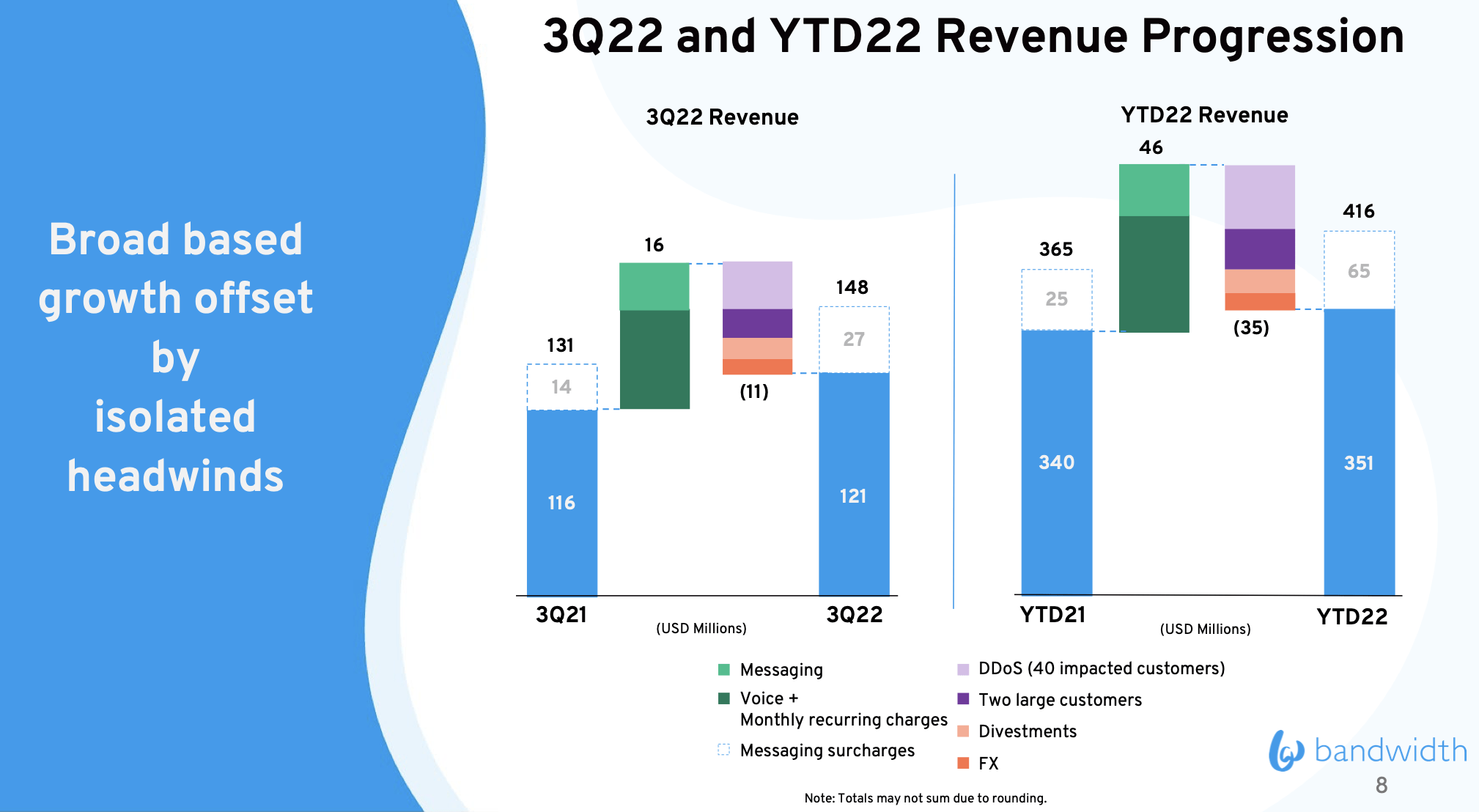

Let’s now zoom into Bandwidth’s transitory headwinds in a bit more detail. In Q3, the company reported $148 million in revenue, representing 13% y/y growth.

Bandwidth Q3 revenue drivers (Bandwidth Q3 earnings deck)

This growth, however, was held down by a number of factors we don’t consider to be part of baseline performance that will hold into 2023. Among them was last quarter’s departure of two large customers as well as divestitures the company made at the start of 2022. (In other words – we think comps will start to get easier in Q1’23 due to these divestitures, and then again in Q2, as we lap the defection of these two large customers). In addition, with the downward trends in the dollar since Bandwidth last reported earnings, FX headwinds should also similarly soften. Taken together, Bandwidth notes that its growth rates were held down by ten points of these transitory headwinds.

It’s worth noting as well that on the Q&A portion of the Q3 earnings call, CEO David Morken noted that A) customers are still expanding their usage (dollar-based net retention was 107% in Q3), and B) the company has not yet seen a slowdown or elongation in deal closing cycles, which is something many software companies have reported.

We’ve noted that contract customer term links have ticked up. Average annual customer spend has ticked up. Our enterprise focus is squarely centered on larger Global 5000 companies, and we’re working with them in all kinds of different verticals in the macro secular trend of digital transformations and in our case, specifically, moving to the cloud with what used to be premise-based equipment and solutions.

And so that trend, I think, is a much more powerful force at the moment and the macro uncertainty. And we’re certainly seeing that in our results whether it’s the contract term length through the average spend. On the sales desk, we’ve got pipeline management expertise that understands how to both nurture and then close long-term enterprise engagements, but I don’t have anything specifically to share about elongating contract close cycles in a way that you’re concerned right now.”

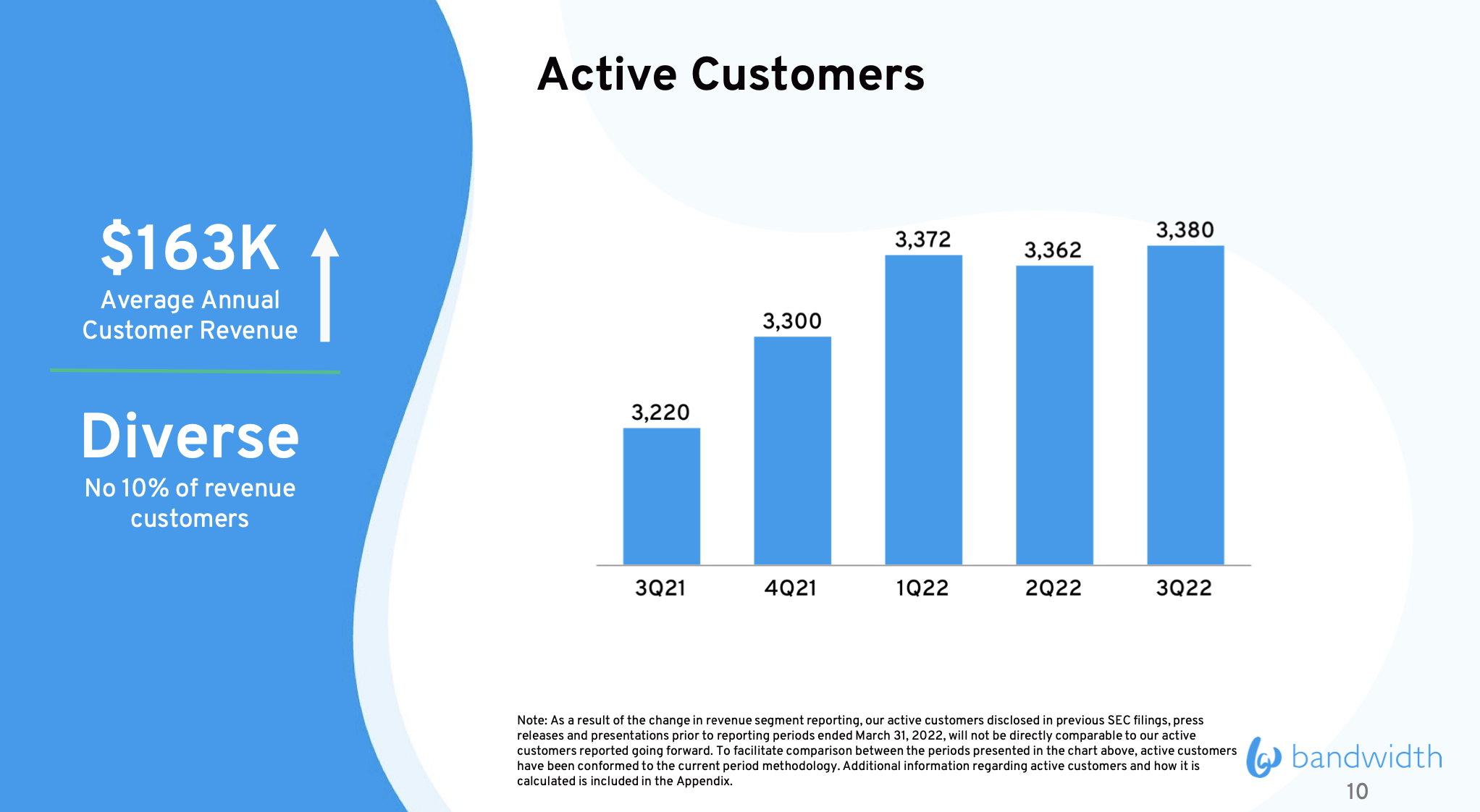

Bandwidth also returned to net-new customer growth in Q3, after seeing churn in a group of smaller customers in Q2 that the company reported as “non-regrettable.”

Bandwidth customer counts (Bandwidth Q3 earnings deck)

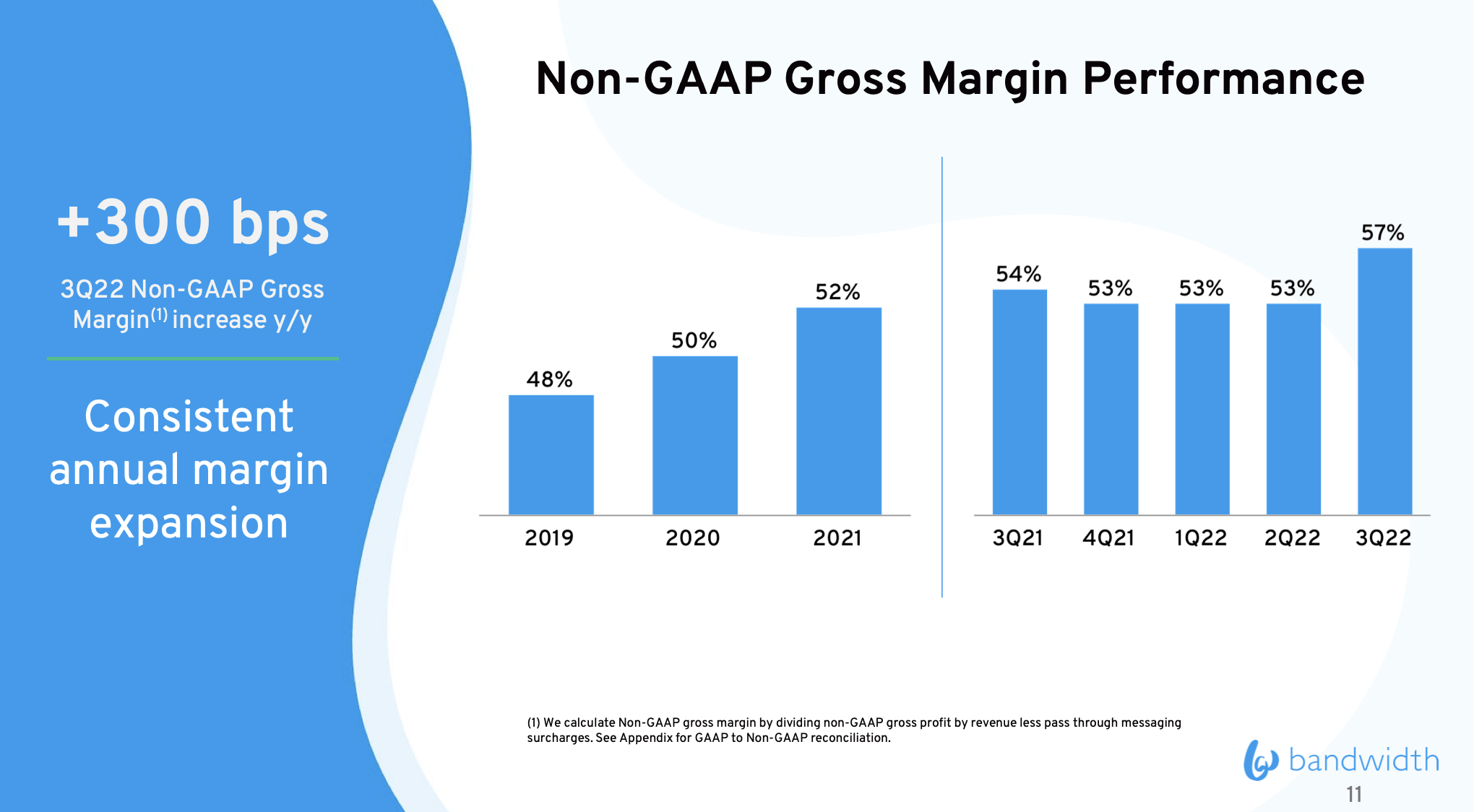

Margins are ticking up

Another thing we should note: Bandwidth has also done a good job at boosting its margin profile. Pro forma gross margins are up 3 points year over year and four points sequentially to 57%, its highest on record:

Bandwidth gross margin trends (Bandwidth Q3 earnings deck)

These margin gains are driven both by favorable product mix toward messaging, as well as economies of scale as the company’s procurement team has succeeded at optimizing spend and securing vendors at a discount.

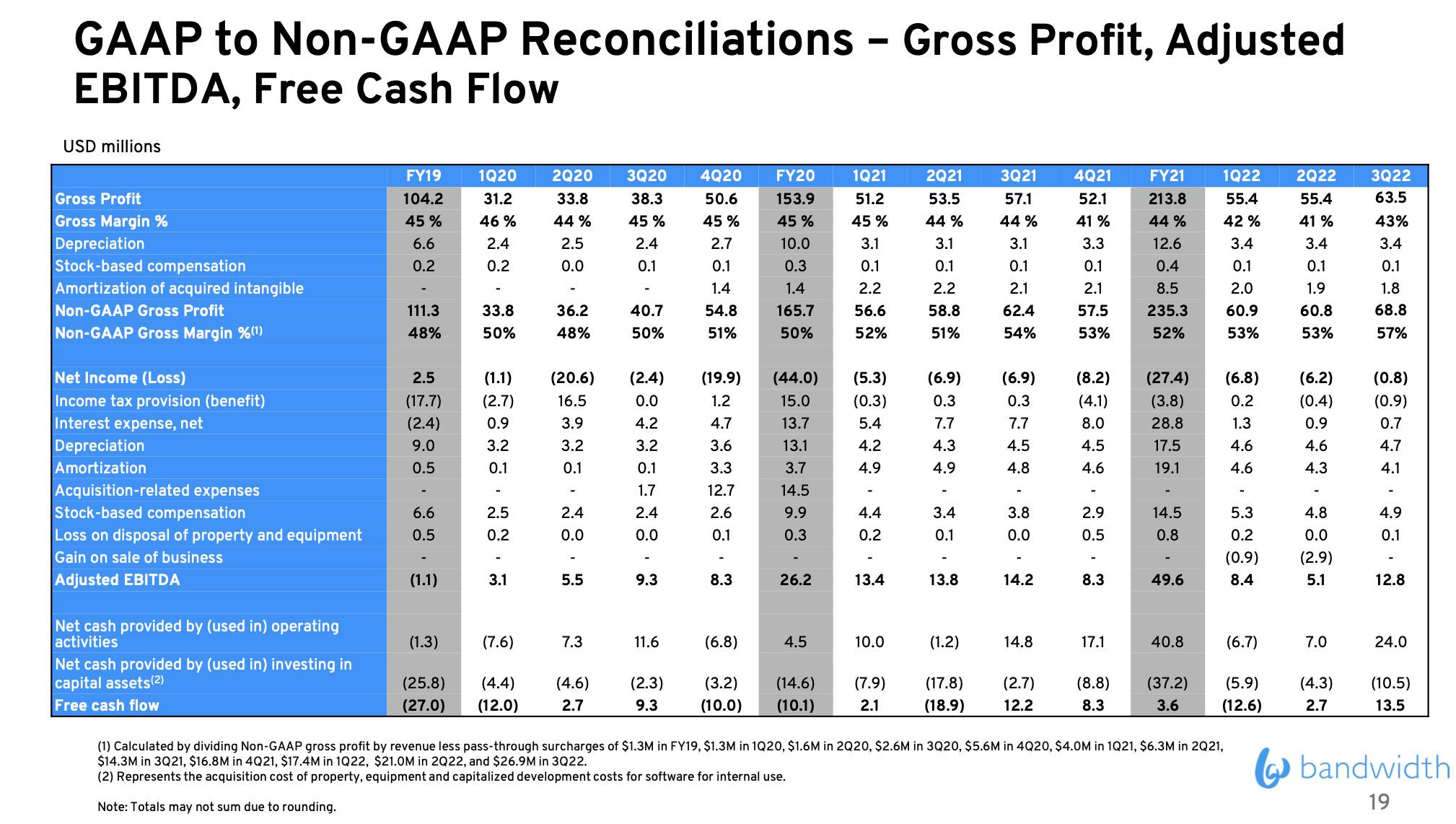

This has helped Bandwidth, in an inflationary opex environment, to maintain positive adjusted EBITDA and free cash flow as shown in the trend charts below:

Bandwidth bottom-line performance (Bandwidth Q3 earnings deck)

Bandwidth’s consistency in generating bottom-line profits, even on a pro forma basis, will help boost sentiment for this stock in a relatively more nervous market environment where investors have zoomed in to tech stocks’ bottom lines.

Key takeaways

Oftentimes, the best rebound plays are out-of-the-spotlight stocks that are trading at immensely attractive valuations, and Bandwidth fits the bill perfectly here. In my view, expectations have reset to extraordinarily conservative lows for this company, and as Bandwidth starts to lap a challenging 2022, growth rates will recover and drive a boost in sentiment for this name. Stay long here.

Be the first to comment