audioundwerbung

Ballard Power (NASDAQ:BLDP) (TSX:BLDP:CA) are facing a lot of challenges as the last earnings report disappoints. Declining revenues makes it hard to see the long-term outlook for the company. With all the issues I have with the company I have a sell rating for them. I really think there are much better opportunities out there for investors to invest in.

Ballard Power Systems, The Product

In short Ballard Power offers customers with fuel-cells. A product where you can ship energy and store it very efficiently. It’s an emission free way of generating energy and something that is pushed heavily as the green energy wave has taken over.

The company primarily focuses on designing and manufacturing these products and then shifting them to their customers. These fuel-cells are then used in a number of different vehicles to power them, all from buses and trucks to rails and marine applications.

As the company states on their website, their mission is to help deliver valuable and innovative solutions to help transition between nonrenewable and renewable energy sources.

The company has divided their business plan into two different segments. The first being about focusing on power product sales. This is meant to provide customers with high value, durable and cost efficient solutions for energy supplies. The fuel-cells are meant to be efficient at providing both energy and also reducing the risks that other energy sources might have. But Ballard Energy is also involved in developing energy solutions to their customers, by helping them with their fuel-cell programs and adoption of them.

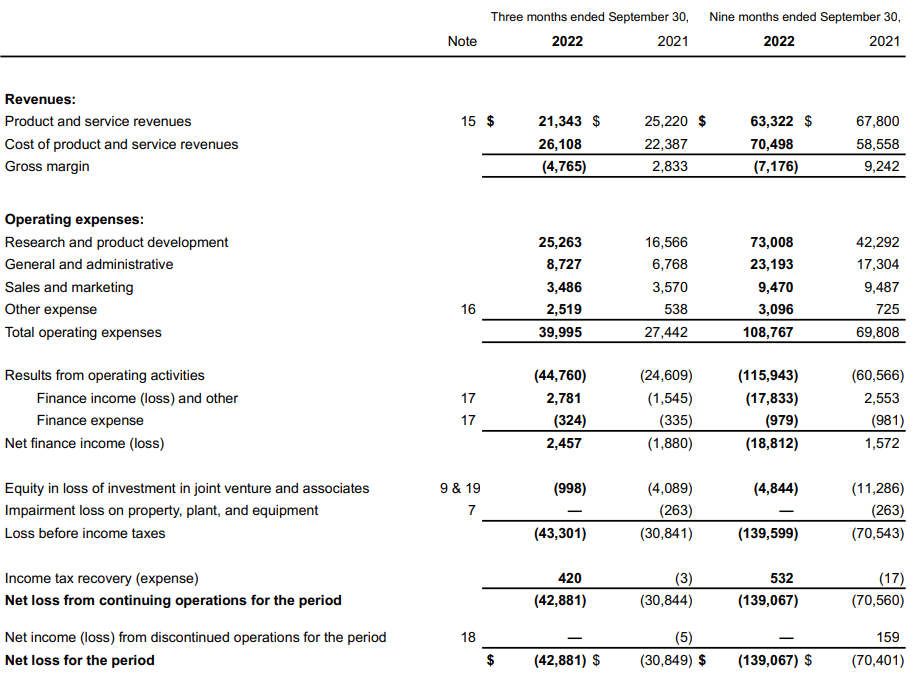

Ballard Power’s Income Statement

Looking at the income statement for Ballard Power Systems for their last Q3 earnings report it’s hard finding any positive developments. Revenues came in at $21.3 million, a decline of 15% YoY, the last thing you want to see as the demand for fuel-cells seems to be increasing otherwise.

Breaking down the revenue segment we can see that a large decrease was seen in “material handling”. Something the company noted was because of lower deliveries to Plug Power (PLUG), decreasing 46% is a lot and something that has me worried about the future of the company.

Ballard Power Income Statement (Q3 Earnings Report)

The quarter ended with the company having a negative gross margin of 22%. The management provided some much needed insight on the cause for that, stating “that a shift to lower overall product margin” and “investment in manufacturing capacity” had the margins down. I think they just haven’t been able to capitalize fully on their products and secure enough customers to grow their business.

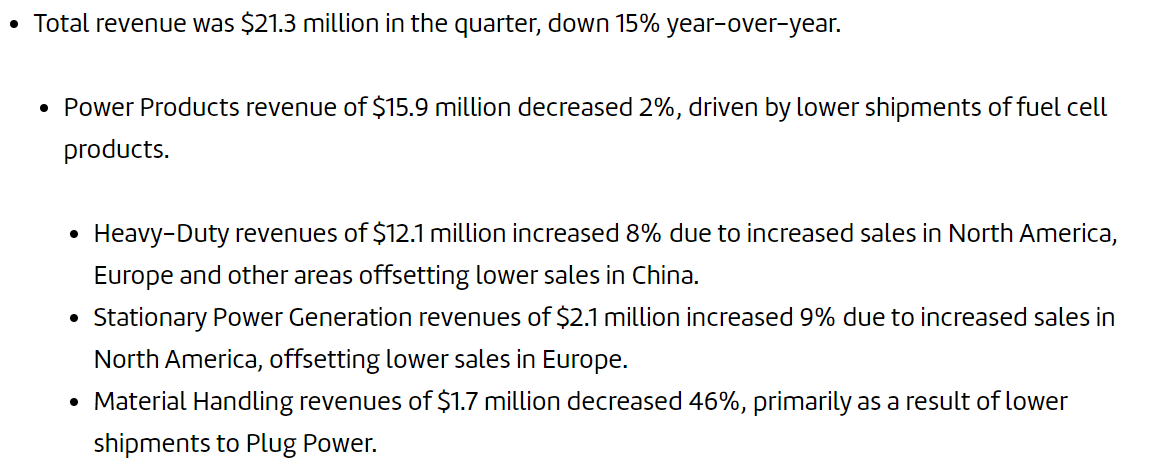

Earnings Report Highlights (Q3 Earnings)

Some positive news was seen however in the earnings report. As the company had an increase in orders. This brought the total order backlog to $107 million. The increase was primarily driven by a much higher European demand. Right now the order backlog is made up of around 55% orders from Europe. In my opinion this brought some much needed positives to the report, but it was still overshadowed by the large loss in revenues the company saw.

With a net loss of $42 million I struggle to see any short term jumps giving Ballard Energy a profitable bottom line. As the EPS came in at ($0.14) the current valuation has investors paying a large premium for the share price.

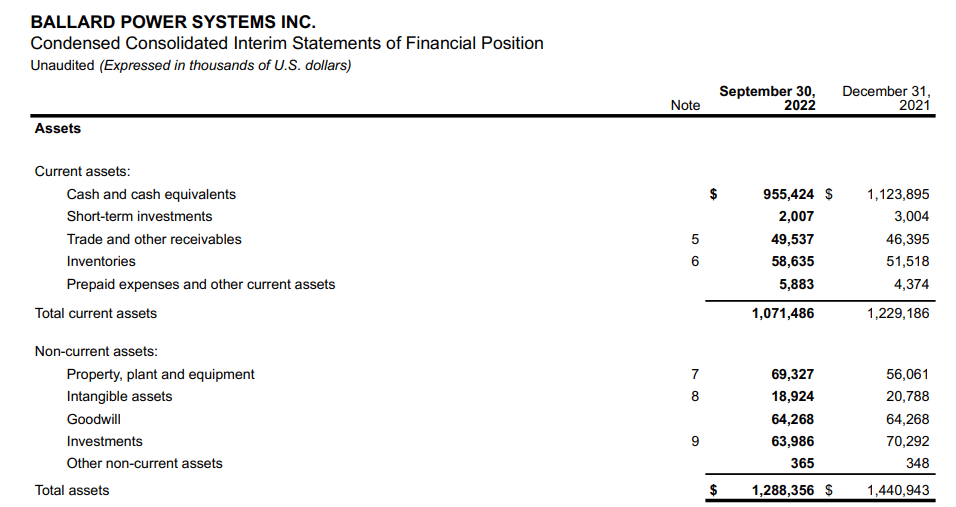

The Balance Sheet

Looking at the balance sheet we are left with some positive news at least. The cash position the company holds has been going down YoY but they are more or less debt free right now which is a major bonus given the situation the company is in with profitability.

Ballard Power Balance Sheet (Q3 Earnings Report)

Amounting to over $950 million in cash, Ballard Energy shouldn’t have to dilute more shares to keep afloat. Given the current operating expense the company has, the cash position would help finance themselves for almost another 6 years. I see that as a good sign as it should be ample time for them to get their stuff in order and have a positive bottom line.

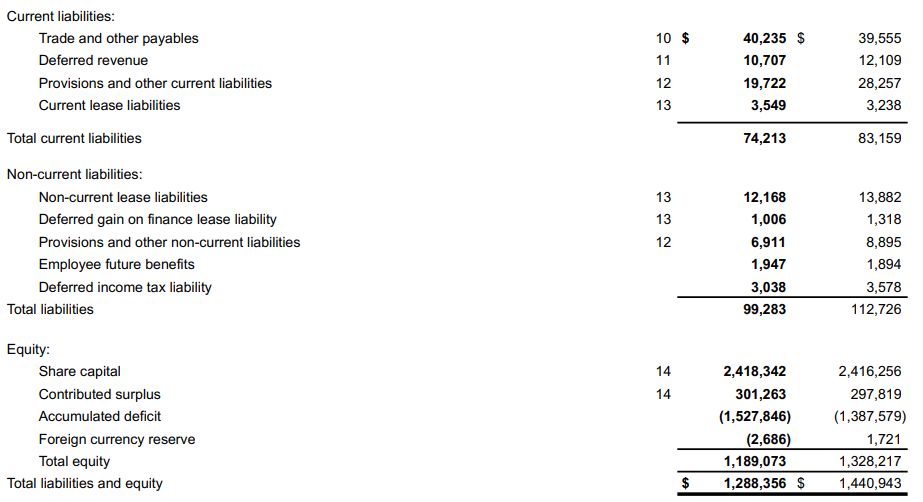

Ballard Power Liabilities (Q3 Earnings Report)

Given this large portion of cash I think the company is in a relatively healthy position to take on some long-term debt in case they want to fund expansion. But I would watch out for the free cash flow they are generating too. If the cash flow digs too deep, I think we could continue to see large share dilution.

Valuing The Company

Valuing the company right now and providing readers with a price target I think would be irresponsible. Until they actually have profitability, not just net margins, but just gross margins I don’t think you would want to have a price set to buy them at.

Since the downside risks of buying a company which isn’t actually generating profits your money are at great risks. The fuel cell market is expected to continue to grow YoY, but Ballard Power does not have the same good margins as some of its competitors like Bloom Energy (BE).

Price Chart (Seeking Alpha)

I think that investors could keep track of a few things if they are interested in getting exposure to the industry. Looking at the way the company is managing with cash and debt is a starting point. Like I stated before, I think they could potentially take on more debt to finance new projects and expansion. This could perhaps help increase revenues.

If the management places a larger focus on having better margins I would see that as a positive sign. But right now they are placing the blame on lack of orders and selling the “less profitable” products. I think they need to pull themselves together and focus on taking more market share and customers. Bloom Energy is also selling fuel-cells and they saw an impressive increase in revenues in their latest report.

Risks With An Investment

Making an investment right now would be incredibly dangerous. As Ballard Energy doesn’t even have positive gross margins, I think it will take time until we see the bottom line improving at all.

Company Info (Ballard Power Website)

I think that given the negative bottom line the potential downside of starting a position here is high. Right now the share price is volatile and decided by potential future net incomes. In my opinion there is nothing that proves the company is able to generate a profit in the future.

Apart from the obvious issues of growth the company has, and the risks that brings to an investment, I also think the market could harm investment. Bloom Energy is the largest fuel-cell company in the US, having over 80% of the market share. This makes them much more able to adapt to higher costs and maneuver around them, compared to Ballard Power.

Conclusion

Ballard Power Systems is a company selling fuel-cells to companies in order for them to generate energy in an emission free way. This is the future according to many, as the push for green energy becomes higher and higher year after year.

But with a lack of even positive gross margins, it’s hard to make a case why you should invest in Ballard Power based on fundamentals and not just pure hope. Unless the company starts focusing on cost effective measures, I think the share price will be suppressed and investors will stay away.

An short, I think that you would be better off selling any shares in the company right now. With such a lack of profitability by the company, any investment right now will face a lot of risks. There are better options out there, with companies already making a profit in this sector.

Be the first to comment