Christoph Burgstedt

Avidity Biosciences (NASDAQ:RNA) was founded in 2012 and is based in San Diego, California.

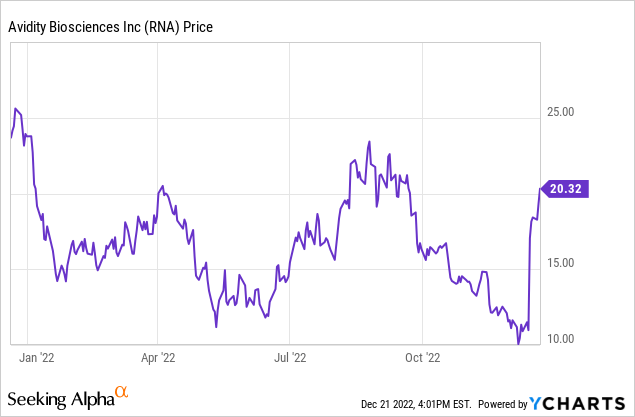

The company’s stock was up 55% last week after releasing preliminary data from a Phase 1/ 2 study of its antibody-oligonucleotide technology candidate in treating myotonic dystrophy type 1. After this news release, I decided to assess the company in detail and present my detailed analysis.

The initial target for the pipeline is muscle diseases like myotonic dystrophy type 1, Duchenne’s muscle dystrophy, etc.

Pipeline:

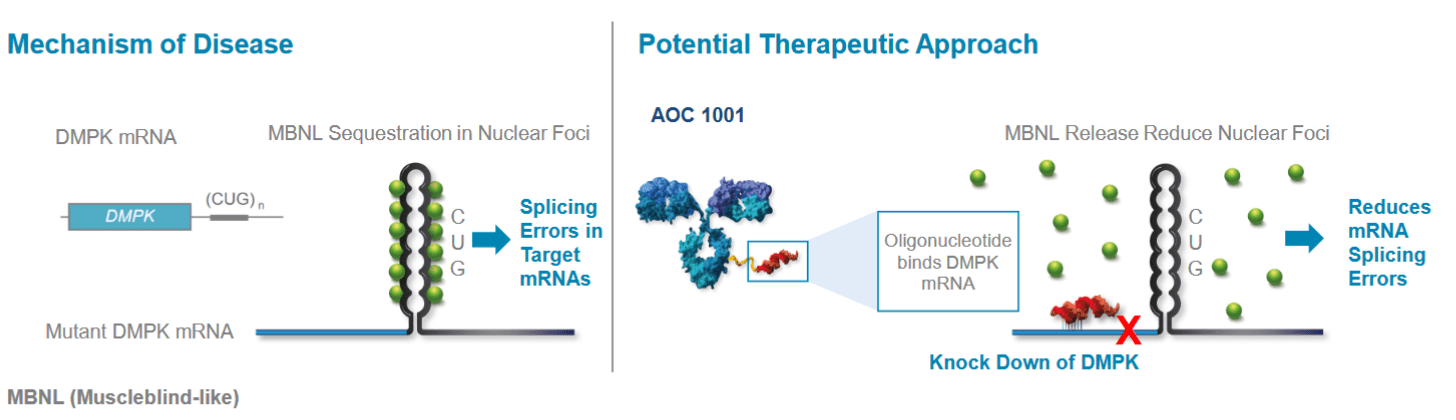

Myotonic Dystrophy type 1:

DM1 is an orphan disease affecting approx. 40K patients in the U.S. It is characterized by muscle weakness, respiratory and cardiac problems, GI complications, and cognitive and behavioral impairment. An abnormality in the DMPK gene causes an increased number of CUG triplet repeats, which can be thousands in DM1 patients compared to approx. 35 in a healthy person.

Investor presentation

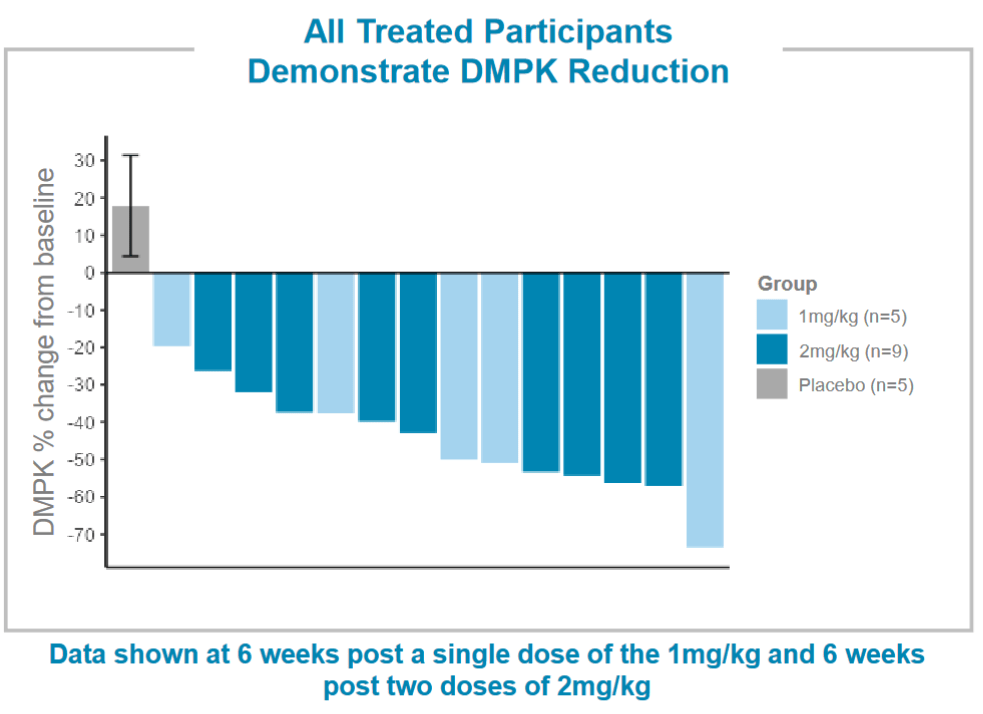

The company released preliminary data from an ongoing Phase 1/2 randomized, placebo-controlled, double-blind clinical trial called MARINA yesterday. A meaningful reduction in DMPK was seen in 100% of treated patients. A mean 45% reduction in DMPK was seen on a single dose of 1 mg/kg or 2 doses of 2 mg/kg. See the waterfall plot below.

Investor presentation

The treatment was also well-tolerated and no treatment-related discontinuations or deaths were seen.

Next catalyst: Additional MARINA trial data is expected in 2023 (likely by mid of year).

The stock was up 55% on the news.

Issue of FDA clinical hold: Earlier in Q3, FDA placed a partial clinical hold on new patient enrollment in the MARINA trial due to a serious adverse event in the 4 mg/kg dose arm. However, dosing is continuing in the enrolled patients. All the enrolled patients in the MARINA trial have opted to enroll in the MARINA-open-label extension trial which will test the therapy over a longer-term follow-up of up to 24 months. This places confidence in the safety of the therapy. I expect FDA to provide a favorable decision on the partial clinical hold issue in H1 2023. Also, FDA allowed the dosing in the currently enrolled patients to continue, so it is a piece of favorable news regarding safety.

The therapy has Fast Track designation from the FDA in treating DM1.

Facioscapulohumeral dystrophy, FSHD:

It is an autosomal dominant genetic disease that affects 16K to 38K people in the U.S. It causes weakness in the face, shoulders, arms, and trunk muscles first, which later spreads to the lower body. It is caused by an abnormal expression of DUX4, a gene involved in embryonic development.

The company is using an AOC, AOC 120 to reduce the expression of DUX4 mRNA and DUX4 protein. An IND has been cleared by FDA and a Phase 1 study is planned.

Duchenne’s muscular dystrophy, DMD:

It is a genetic disease that causes muscle weakness in male children and affects 1 in 3500-5000 live male births. The company is targeting exons 44, 45, and 52 which affect approx. 30% of all mutations amenable to exon skipping.

IND clearance has been obtained for the first program targeting exon 44 skipping (7% of all cases) and a clinical study is planned.

Financials and other information:

Cash reserves are expected to be $500M after the recent offering. There is no long-term debt.

CEO Boyce was the President of Akcea Therapeutics and held senior leadership roles at big pharma like Novartis, Alexion Pharmaceuticals, and Ionis Pharmaceuticals.

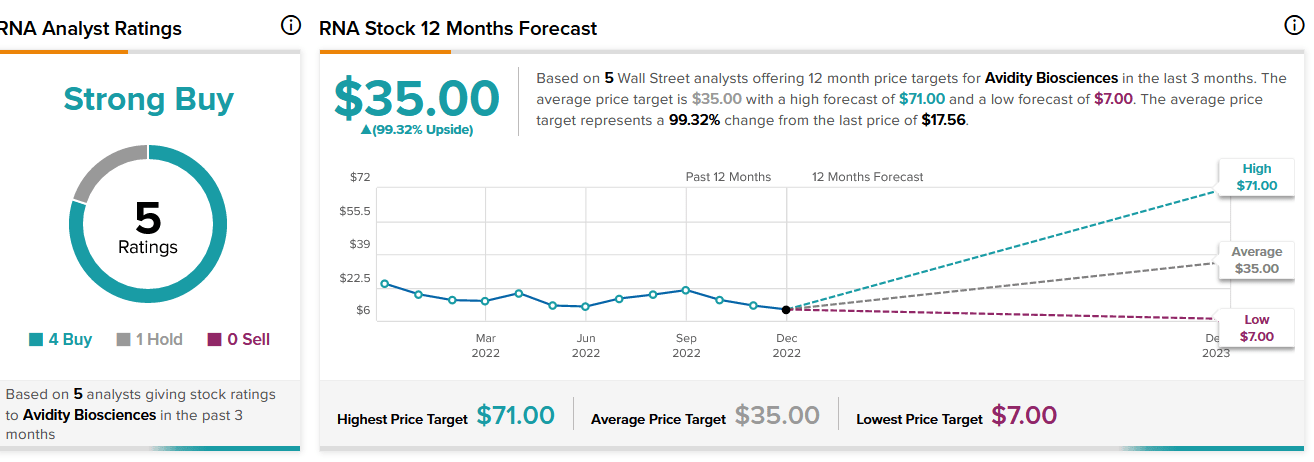

The mean consensus Wall Street analyst price target is $35 (100% upside). After the recent data, the median of 4 new price target issues is also $35. Raymond James issued a Street-high price target of $71 after the data.

Tipranks

Prominent institutional investors holding the stock include RTW Investments (holds a 9.5% stake in the company), and ECor1 Capital (holds a 5.3% stake).

The next price-moving catalyst is the updated Phase 1/2 MARINA trial data in 2023 (likely in mid-2023).

My plan is to start a small position and add more on the dips targeting 2-3% portfolio allocation with a 2-3 year timeframe.

Risks in the investment include underwhelming data or loss of efficacy, side effects, failure to lift FDA clinical hold or new clinical hold, etc. This is a developmental stage biotech company with risks and thus, may not be suitable for all investors. This note represents my own opinion and is not professional advice. Investors should consult their financial advisors and conduct their own research and due diligence before making any investment decisions.

Be the first to comment