sl-f/iStock via Getty Images

Article Thesis

AvalonBay Communities (NYSE:AVB) is a real estate investment trust focused on apartments in major metropolitan areas. The company’s shares have come under pressure over the last year, which has made the valuation decline to an attractive level, and which has made the dividend yield rise well above the historic norm. Since operational results are strong, AVB looks attractive right here.

Company Overview

AvalonBay Communities, Inc. is a REIT that owns around 90,000 apartments in around 300 communities that are located in major metropolitan areas across 11 states and in DC.

There are cyclical sectors in the real estate space, such as hotels, malls, and other strength-of-the-economy-dependent market segments. But demand for housing isn’t dependent on the strength of the economy, as people need a place to live in all economic environments. That is why AvalonBay has been remarkably resilient in the past, and I believe the same will hold true in the future. Between 2012 and 2019, AvalonBay grew its FFO per share during every year. In 2020, due to some rent concessions, FFO per share was down 7%, but even that was a pretty solid result — while the world stood still, AVB still generated 93% of the profit it generated during the previous year.

The dividend remained well-covered as well during the pandemic and other crises in the past, as the dividend coverage ratio stood at 1.4 in 2020, thus the company did not have to cut its payout. AvalonBay has a dividend track record of 28 years, although it did not increase the payout during each of those years. Still, the past track record warrants a great Dividend Consistency score:

Seeking Alpha’s Quant algorithm

AVB: Attractive Right Here

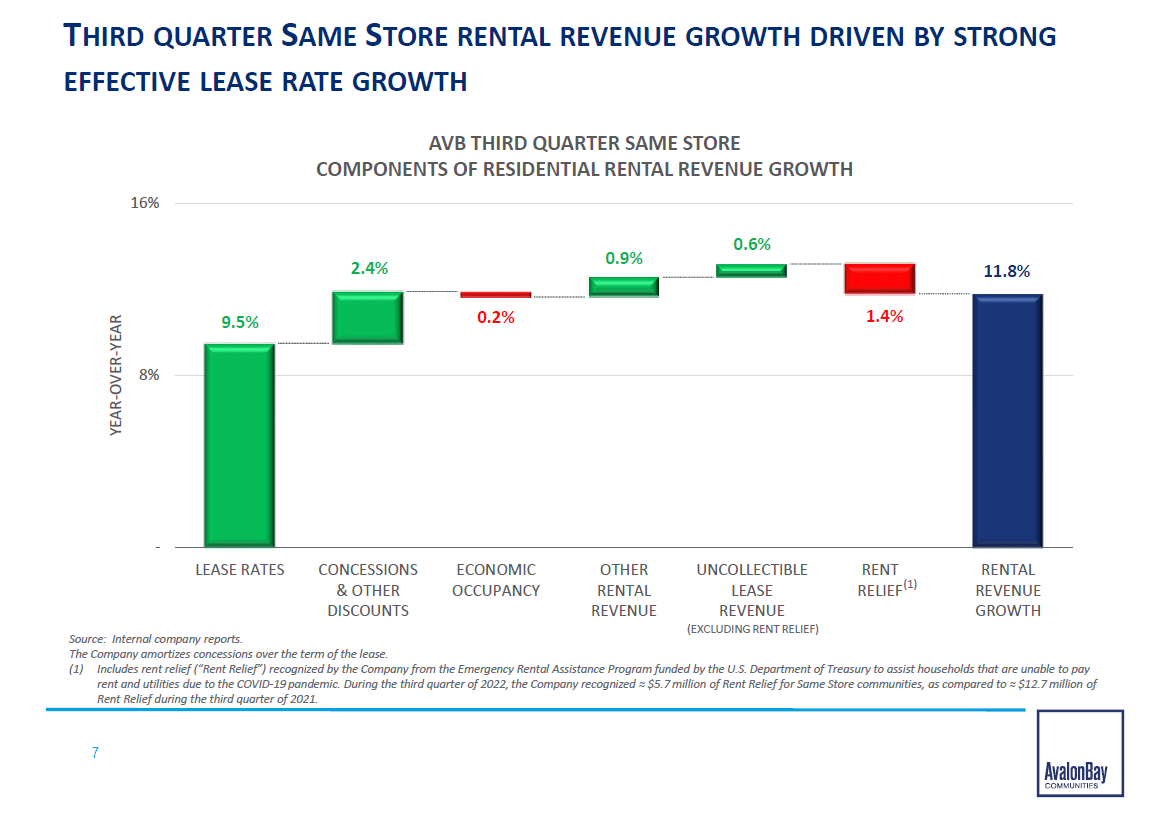

Everyone knows that rents have gone up quite a lot in the last two years, and that also holds true for the assets that AvalonBay owns. That’s why its comparable rent growth has been highly compelling, including during the most recent quarter:

AVB presentation

AvalonBay has generated rental revenue growth of 12% in the most recent quarter, primarily driven by a 10% lease rate increase, while some minor items such as concessions also had a positive impact. Same-property revenue growth is more valuable for AvalonBay compared to revenue growth that is derived via the acquisition or construction of new communities. When new assets are acquired, they come with additional costs for managing these properties and for financing them, as they are partially financed with debt that causes interest costs for the REIT. But when AvalonBay grows its revenue via same-property growth, i.e. by increasing its lease rates, then these additional revenues don’t go hand in hand with additional costs, which makes same-property-driven rent growth extremely accretive for the company.

Not surprisingly, the company has seen its profits grow significantly in the recent past on the back of compelling lease rate growth — AvalonBay’s core funds from operations per share grew from $2.06 in the third quarter of 2021 to $2.50 in the third quarter of 2022 (the most recent quarter), which made for an annual FFO growth rate of 21.4%. Of course, AvalonBay will not continue to grow like this forever, but this shows how much AvalonBay benefits from the current environment of quickly-growing apartment lease rates. Even when growth stalls out and reverts back to a more normal level eventually, the gains in lease rates we have seen over the last two years or so will persist, I believe, thus future lease rate development will start from a permanently higher level.

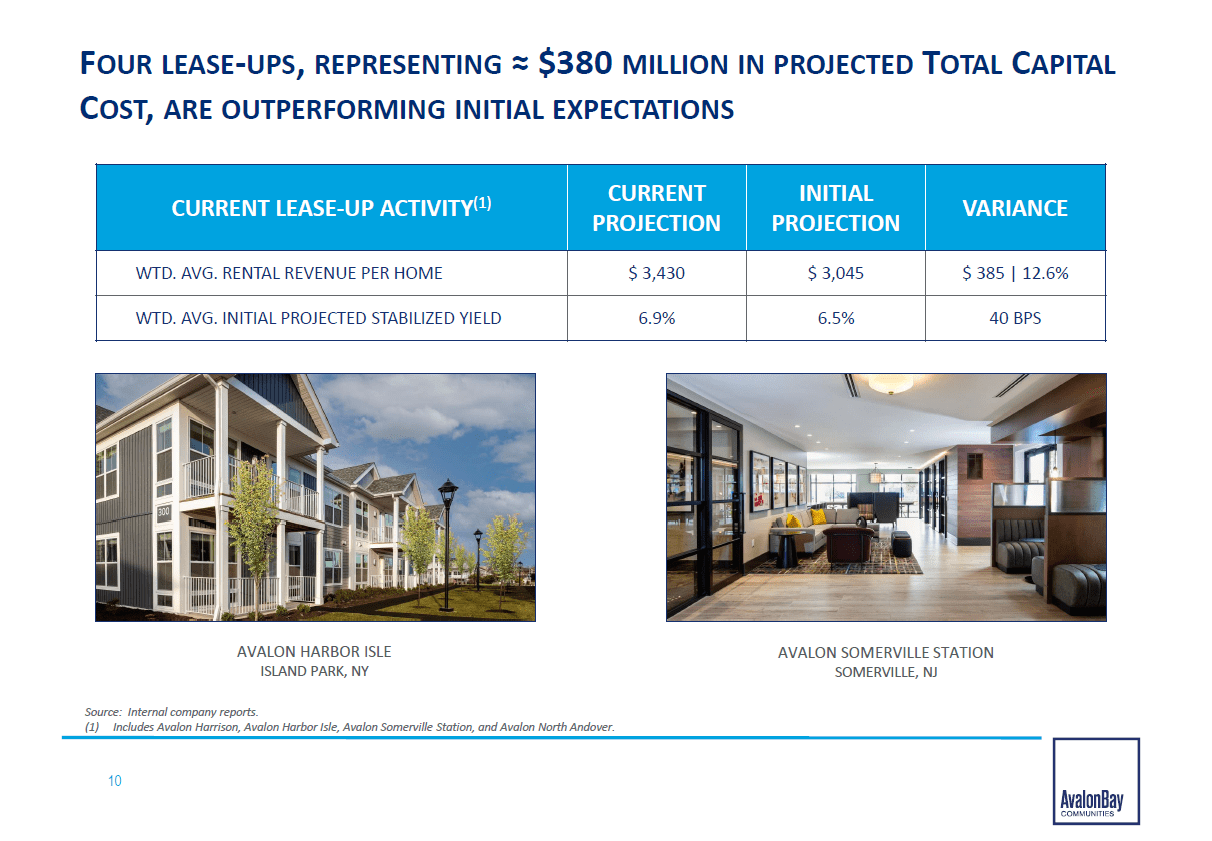

While rising lease rates on existing properties are highly important, AvalonBay is also developing new assets on top of that. The revenues derived via those aren’t as high margin as the additional revenue AVB generates from raising lease rates, but over time, new property development still adds meaningfully to AVB’s FFO per share and thus also its share price/value. Current developments that will add to AvalonBay’s results going forward include the following:

AVB presentation

Avalon Harbor Isle in NY State and Avalon Somerville Station in New Jersey are two of the newest additions to AvalonBay’s portfolio — both are outperforming the original estimates when it comes to their yields, or return on the price AVB paid to develop them. A current weighted yield of 6.9%, or almost 7%, sounds very solid in absolute terms. When we consider that AVB uses leverage to partially finance these assets, the return on the equity portion becomes more attractive, however. Based on AVB’s interest expense of $60 million during the most recent quarter, or $240 million per year, we can estimate its current cost of debt at just 3.2% based on a net debt position of $7.6 billion. If new properties are financed with 50% equity and 50% debt, the leverage effect makes AVB’s return on equity climb to 10.6% at a going-in yield of 6.9%, comparable to what AVB has showcased for the two developments shown above. In short, generating returns on equity in the 10% range or slightly higher is a very much achievable goal for AvalonBay, which is quite attractive, I believe, as long as investors buy AVB at a valuation that is not too high.

AvalonBay is recycling capital at times, meaning it sells properties that are fully-valued, or where AVB deems the market price attractive (for the seller). That money can then be used for developing new properties where the yield on the price AVB pays is higher:

AVB presentation

During the most recent quarter, AvalonBay sold $855 million worth of properties, at a cap rate of 3.9%. When AvalonBay sells properties at a 3.9% cap rate and invests the proceeds in new developments with yields in the 6% to 7% range, that’s highly accretive. If, for example, the proceeds from the sales during the most recent quarter were invested at an average return rate of 6.5%, AvalonBay would grow its annual income from this $855 million investment from $33 million to $56 million — an increase of 70%.

Of course, there’s some execution risk when AVB develops new projects, and there is also a time lag, as new property developments do not generate cash flows at the time when the project is started. Still, this capital recycling strategy will lift AvalonBay’s returns significantly over time, which is one of the reasons for AVB’s strong long-term track record — the company has generated an annualized shareholder return of 13.4% since its IPO in the 1990s, easily trouncing the returns of the broad market.

AvalonBay’s development pipeline will result in sizeable revenue growth over the coming years, as current developments will add around $130 million per year to the company’s net operating income, according to current projections by management. That’s equal to around 10% of AvalonBay’s funds from operations today, thus the company already has built-in growth of 10% in its pipeline from current developments. Same-property growth thanks to further lease rate increases should add some growth as well, thus it is expected that AVB will continue to deliver compelling FFO growth in 2023 and beyond:

Seeking Alpha

Analysts are predicting that FFO per share will rise by 7% this year and by 6% next year, following a very sizeable 18% jump in FFO per share in 2022. While 6%-7% annual profit growth wouldn’t be too attractive for a highly-valued tech player, that’s pretty compelling for a REIT, as REITs are generally seen as income vehicles primarily.

AvalonBay currently offers a dividend yield of 3.7%. In combination with a 6%-7% annual profit growth rate, that would allow for a similar dividend growth rate at unchanged payout ratios, AvalonBay could deliver total returns in the 10% range, before potential multiple expansion tailwinds:

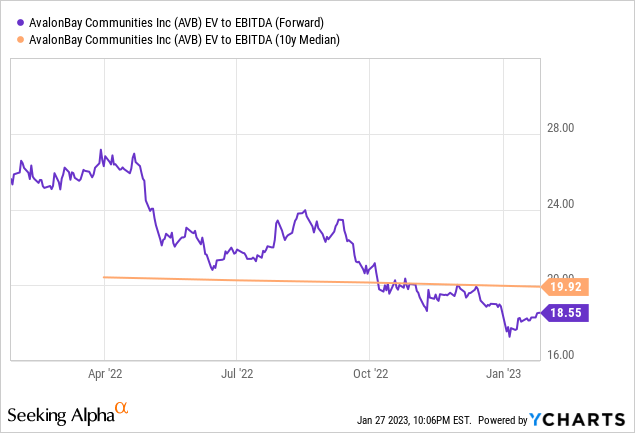

Right now, AVB trades at a 18.5x EBITDA multiple. Due to the properties that are currently in development, with “built-in” future EBITDA that is not yet visible, one could argue that this understates AVB’s attractiveness. But despite that, AVB trades at a discount compared to the longer-term average valuation. Relative to where AVB traded one year ago, the stock is outright cheap, although I do not expect that AVB will rise back to a mid-20s EBITDA multiple in the near term. But even multiple expansion towards the ~20 range it has historically been valued at would allow for some total return tailwinds already.

Takeaway

REITs have been sold down due to rising interest rates. But AVB seems like it has been hit too hard — its balance sheet is strong, the REIT has locked in low rates for many years (weighted average time to maturity of more than 8 years), and underlying results are highly compelling. The pipeline will add meaningfully to FFO going forward, and management expects solid lease rate growth in 2023.

Shares are trading at a below-average valuation, and between expected profit growth, the dividend yield of 3.7%, and some multiple expansion tailwinds, total returns could be compelling going forward.

Be the first to comment